Of course you can withdraw money from your IRA at any time. It’s your money, after all. The real question isn’t if you can take it out, but how you can do it without getting hit with a nasty 10% early withdrawal penalty and a bigger-than-expected tax bill.

The answer almost always boils down to one simple thing: your age.

Your Guide to IRA Withdrawal Rules

It helps to think of your Individual Retirement Arrangement (IRA) as a kind of financial greenhouse. The government gives you some great tax benefits to encourage you to let your savings grow in there, protected and untouched, until you’re ready for retirement.

But if you open the greenhouse door and take things out too early, there are consequences.

The IRS has a magic number: age 59½. Once you hit that milestone, the door swings open, and you can generally access your funds without that dreaded 10% penalty. Before that age, any money you take out is usually considered an "early" distribution, which means you could face the penalty on top of the regular income taxes you’ll owe.

Understanding the Basics

Before diving into the complex exceptions and strategies, it’s critical to get a handle on a few core principles. These are the building blocks that will help you understand every other rule we’ll cover.

The outcome of any withdrawal really depends on three key factors:

- Your Age: It’s the big one. Are you over or under that 59½ threshold?

- Your IRA Type: The rules for a Traditional IRA and a Roth IRA are worlds apart, especially when it comes to taxes.

- The Reason for Withdrawal: Life happens. The IRS recognizes this and allows for penalty-free access in certain situations, like buying your first home or covering major medical bills.

For a quick reference, here’s a simple breakdown of how these rules play out in common scenarios.

IRA Withdrawal Rules at a Glance

| Withdrawal Scenario | Traditional IRA Consequences | Roth IRA Consequences |

|---|---|---|

| Withdrawal after age 59½ | Taxed as ordinary income. No 10% penalty. | Contributions: Tax-free and penalty-free. Earnings: Tax-free if the account is at least 5 years old. |

| Withdrawal before age 59½ (No Exception) | Taxed as ordinary income. 10% early withdrawal penalty applies. | Contributions: Tax-free and penalty-free, anytime. Earnings: Taxed as ordinary income, and a 10% penalty applies. |

| Withdrawal before age 59½ (With Exception) | Taxed as ordinary income. The 10% penalty is waived. | Contributions: Tax-free and penalty-free. Earnings: Taxed as ordinary income, but the 10% penalty is waived. |

This table gives you the 30,000-foot view, but as you can see, the details matter—a lot.

At Spivak Financial Group, we spend our days helping people navigate these variables to make the smartest financial moves possible. The goal is always the same: access your money when you need it while keeping as much of your hard-earned savings as you can.

This guide will walk you through everything you need to know. We’ll unpack the penalties, clarify the exceptions, and give you the confidence to make the right call for your situation, whether you’re planning for retirement years down the road or need to access your funds sooner than expected.

Understanding the Core IRA Withdrawal Rules

Every Individual Retirement Arrangement (IRA) is built on a handful of foundational principles meant to encourage us to save for the long haul. Think of these as the ground rules for that financial "greenhouse" we mentioned earlier. Getting a firm grip on these concepts is your first step before you even think about touching that money without making a costly mistake.

The single most important rule to burn into your memory is the age 59½ threshold. This specific age is the magic number that acts as a dividing line. Any money you pull out after hitting this age is considered a "qualified distribution," which is just the IRS's way of saying you've played by the rules.

But take money out before that age, and it's generally considered an "early distribution." That's when things can get expensive.

The 10% Early Withdrawal Penalty

The government gives us great tax breaks to help our IRA money grow, but there's a catch if you raid the cookie jar too soon. If you take funds out before age 59½, you'll most likely get hit with a 10% additional tax on the taxable part of that withdrawal. Let's be clear: this isn't your regular income tax. It's a separate penalty slapped on by the IRS to discourage people from cashing out early.

Let's say you're 45 and need to pull $20,000 from your Traditional IRA. Here’s what that looks like:

- Early Withdrawal Amount: $20,000

- 10% Penalty: $2,000 (This goes straight to the IRS)

That $2,000 penalty is on top of the ordinary income taxes you'll also owe on the $20,000. Depending on your tax bracket, the total haircut on that withdrawal could easily eat up 30-40% of the money you take out. This penalty is exactly why you have to be so careful.

The whole point of the 10% penalty is simple: to keep your retirement money saved for, well, retirement. But the tax code isn't completely heartless. It recognizes that life happens, which is why there are several important exceptions that let you dodge this penalty. We'll get to those in a bit.

Two Flavors of IRAs Mean Two Sets of Tax Rules

Figuring out if you can pull money from your IRA is also about understanding how it will be taxed. The tax hit you take depends entirely on whether your money is in a Traditional IRA or a Roth IRA. These two accounts are essentially mirror opposites when it comes to taxes.

Traditional IRA Withdrawals

With a Traditional IRA, you usually put in pre-tax money. That means you probably got a nice tax deduction for your contributions along the way. Since you haven't paid Uncle Sam on that money yet, he's waiting to collect when you finally take it out.

- Tax Treatment: Any and all withdrawals from a Traditional IRA are taxed as ordinary income. The amount you take out is just added to your other income for the year and taxed at whatever your marginal tax rate is.

Roth IRA Withdrawals

A Roth IRA is the exact opposite. You contribute with after-tax money, so you don't get that immediate tax break. The big payoff comes later: your money grows tax-free, and your withdrawals in retirement are also completely tax-free.

- Tax Treatment: As long as you're over 59½ and your account has been open for at least five years, qualified withdrawals of both your contributions and your earnings are 100% tax-free.

- A Special Rule for Contributions: Here's a powerful feature of the Roth: you can withdraw your direct contributions at any time, at any age, for any reason, completely tax-free and penalty-free. The IRS just sees it as you taking your own money back.

This difference is everything. A $20,000 withdrawal from a Traditional IRA could leave you with less than $14,000 after taxes and penalties. But withdrawing $20,000 of your contributions from a Roth IRA puts the full $20,000 right back in your pocket. Knowing which account you have is step one in building a smart withdrawal plan.

How to Legally Avoid the 10% Early Withdrawal Penalty

While the age 59½ rule is the main gatekeeper for your IRA funds, life is rarely that simple. Unexpected events can create an urgent need for cash, and thankfully, the IRS understands this. They’ve established several specific exceptions that act as legal "keys" to unlock your IRA before age 59½ without triggering that painful 10% early withdrawal penalty.

It's crucial to remember one thing, though: even when the 10% penalty is waived, you will still owe ordinary income tax on any pre-tax money you pull from a Traditional IRA. Think of it this way: the IRS may forgive the penalty, but it never forgets the tax.

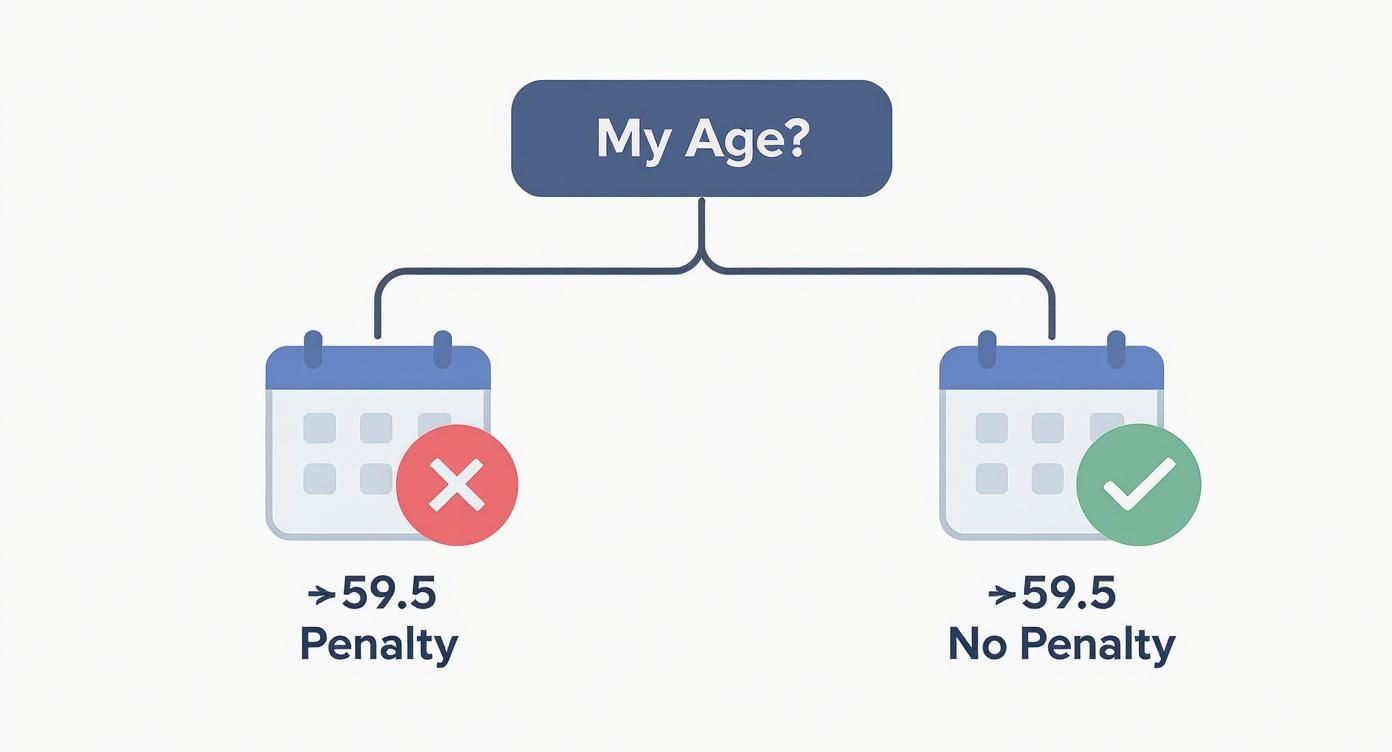

This infographic gives you a quick visual on how the primary withdrawal rule works based on your age.

As you can see, your age is the first and most critical factor. But as you'll learn, certain life events can create important workarounds to this general rule.

Common Exceptions for Penalty-Free Withdrawals

The IRS has carved out several situations where you can take an early distribution without the extra tax hit. These are some of the most common pathways people use to access their funds when life throws a curveball.

- First-Time Home Purchase: You can withdraw up to a $10,000 lifetime maximum from your IRA penalty-free to buy, build, or rebuild a first home for yourself, your spouse, your kids, or even your grandkids.

- Higher Education Expenses: Need to pay for college? You can take penalty-free distributions to cover qualified higher education costs for yourself, your spouse, children, or grandchildren at an eligible school.

- Significant Medical Expenses: If you have unreimbursed medical bills that exceed 7.5% of your adjusted gross income (AGI), you can withdraw funds penalty-free to pay for that excess amount.

- Health Insurance Premiums: If you lose your job and receive unemployment compensation for 12 straight weeks, you can take penalty-free withdrawals to pay for your health insurance premiums.

- Total and Permanent Disability: If you become totally and permanently disabled, the IRS allows you to access your IRA funds without the 10% penalty.

These exceptions provide much-needed flexibility, but they each come with their own specific rules and documentation requirements. It’s absolutely vital to make sure your situation aligns perfectly with the IRS guidelines to avoid any unwelcome surprises come tax time.

New Relief Under the SECURE 2.0 Act

Recent legislation has acknowledged the growing financial pressures many families are facing. According to The Vanguard Group, early withdrawals from retirement accounts recently hit an all-time high of 3.6%, jumping from 2.8% the previous year. This clearly shows a trend of people needing to tap their retirement savings for immediate needs.

In response, the SECURE 2.0 Act introduced some new, targeted relief options. For instance, you can now withdraw up to $1,000 once a year for personal or family emergencies without incurring the 10% penalty. For victims of domestic abuse, the penalty-free withdrawal limit is even higher, allowing up to the lesser of $10,000 or 50% of the account balance.

The 72(t) or SEPP: A Powerful Strategy for Early Retirees

For anyone planning to retire early, there is a far more powerful and structured exception: Substantially Equal Periodic Payments (SEPP), also known as a 72(t) distribution plan. This isn't a one-time withdrawal for a specific expense; it's a calculated income stream designed to provide consistent, penalty-free cash flow for years.

A 72(t) plan allows you to receive a series of payments from your IRA for at least five years or until you turn 59½, whichever period is longer. If structured correctly, every single dollar of these distributions is exempt from the 10% penalty.

Think of it as setting up your own personal pension directly from your IRA funds. The IRS allows this, but only if you follow a very strict set of rules. You must use one of three approved calculation methods (amortization, annuitization, or life expectancy) to determine your annual payment amount.

Once a 72(t) plan is in motion, you absolutely cannot modify it. You can't take more, you can't take less, and you can't stop the payments until the term is complete. A single mistake—like taking an extra dollar or missing a payment—can "bust" the plan. That would retroactively apply the 10% penalty to all distributions you've ever taken, plus interest.

The complexity and unforgiving nature of these rules are why precision is everything. Partnering with a specialist isn't just a good idea; it's essential for success. At Spivak Financial Group, our entire focus is on designing and implementing compliant 72(t) plans that empower our clients to access their funds early without devastating penalties. If you're exploring this powerful strategy, you can learn more about when you can take money out of an IRA without penalty through our detailed resources. It can be a life-changing tool, but it must be handled with expert care.

Traditional vs. Roth IRA Withdrawals Explained

When you ask, "can I withdraw money from my IRA," the answer is almost always yes. But the real question isn't "can I," it's "what happens when I do?" The impact of a withdrawal changes dramatically based on whether you have a Traditional or Roth IRA.

Think of them as two different paths up the same retirement mountain. One gives you a tax break for the initial climb, while the other makes reaching the summit—and enjoying the view—completely tax-free. Your experience pulling funds from these accounts will be worlds apart, especially when it comes to taxes. Getting this right is fundamental.

The Traditional IRA Path: Pay Taxes Later

The big draw of a Traditional IRA is the upfront tax benefit. For most people, contributions are made with pre-tax dollars, which means you get to deduct that amount from your income in the year you contribute. It’s a nice, immediate way to lower your tax bill today.

But the IRS always gets its share in the end. When you eventually pull money out of a Traditional IRA, every dollar of that distribution is taxed as ordinary income. The amount you withdraw is simply added to your other income for the year and taxed at whatever your marginal rate is at that time.

This applies to everything—your original contributions and all the growth they've generated over the years. No exceptions.

The Roth IRA Path: Pay Taxes Now

A Roth IRA flips the script entirely. You contribute with after-tax dollars, so you don't get that immediate tax deduction. You're paying your taxes upfront before the money even hits the account.

The payoff for this strategy is huge, and it comes at withdrawal.

Because you've already paid taxes on your contributions, you can withdraw that principal amount at any time, at any age, for any reason, completely tax-free and penalty-free. It’s your money, plain and simple. This incredible flexibility is the Roth IRA's superpower.

Now, for the earnings your money has generated, the rules are a bit stricter. To get those out tax-free and penalty-free, you generally need to check two boxes: you must be at least 59½, and your Roth IRA has to have been open for at least five years.

Understanding the Roth IRA 5-Year Rule

This "5-year rule" can seem confusing, but it’s actually pretty straightforward. The clock starts ticking on January 1st of the very first year you contribute to any Roth IRA. Once you've passed that five-year mark and you're over 59½, all your earnings are officially unlocked for tax-free withdrawal.

The choice between these two accounts has massive long-term consequences. For a much deeper look at the strategy behind this decision, our guide on choosing a Roth IRA or not can walk you through the specifics to help you make the right call for your future.

Here's a simple table to quickly see the differences side-by-side.

Comparing Traditional and Roth IRA Withdrawal Rules

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution Taxes | Made with pre-tax dollars (usually deductible) | Made with after-tax dollars (not deductible) |

| Withdrawal of Contributions (Any Age) | Taxed as ordinary income; subject to 10% penalty if under 59½ | Always tax-free and penalty-free |

| Withdrawal of Earnings (After 59½) | Taxed as ordinary income | Tax-free (if 5-year rule is met) |

| Withdrawal of Earnings (Before 59½) | Taxed as ordinary income; subject to 10% penalty | Taxed as ordinary income; subject to 10% penalty (unless an exception applies) |

This comparison makes it clear how your account choice sets the stage for what happens when you need to access your money.

A Real-World Withdrawal Comparison

Let's put this into practice with a real-world scenario. Imagine you're 48 years old, in the 22% federal tax bracket, and you need to pull $20,000 for an emergency that doesn't qualify for a penalty exception.

Withdrawing $20,000 from a Traditional IRA:

- 10% Early Withdrawal Penalty: $20,000 x 10% = $2,000

- Federal Income Tax: $20,000 x 22% = $4,400

- Total Cost: $2,000 + $4,400 = $6,400

- Money in Your Pocket: $20,000 – $6,400 = $13,600

Withdrawing $20,000 of Contributions from a Roth IRA:

- 10% Early Withdrawal Penalty: $0 (Contributions are always penalty-free)

- Federal Income Tax: $0 (Contributions are always tax-free)

- Total Cost: $0

- Money in Your Pocket: $20,000

The difference is staggering. In this situation, the Roth IRA puts an extra $6,400 in your pocket. Your initial choice of account isn't just a minor detail—it's absolutely central to your withdrawal strategy and how much of your own money you actually get to keep.

The Practical Steps to Making an IRA Withdrawal

Knowing the rules is one thing, but how do you actually get the money out of your IRA? It's a fair question. Once you’ve decided to take a distribution, the logistics are thankfully pretty straightforward.

This section is your step-by-step guide to navigating the process. We'll demystify it so you can access your funds with confidence and without any nasty surprises.

The whole process kicks off with your IRA custodian. This is just the financial institution—like a brokerage, bank, or mutual fund company—that holds your retirement account.

Step 1 Contact Your IRA Custodian

Your first move is to get in touch with your custodian. You can usually do this through their online portal, over the phone, or by walking into a local branch.

When you connect, you’ll need to verify you are who you say you are and tell them you want to make a distribution from your IRA.

To make things go smoothly, have this information handy:

- Your full name and account number.

- The exact dollar amount you want to withdraw.

- The reason for the withdrawal (this is for their records, and it's especially important if you're claiming a penalty exception).

From there, your custodian will get you the necessary paperwork, which is typically called a Distribution Request Form. These days, it can almost always be completed digitally.

Step 2 Complete the Distribution Request Form

Think of the distribution form as the official instruction slip for your custodian. It's absolutely critical to fill it out accurately to avoid any headaches or delays.

You'll be asked to confirm your personal details, the withdrawal amount, and how you want to receive the money—usually an electronic transfer to your bank account or a physical check. Pay close attention to every field. A simple mistake, like a typo in your bank account number, can cause a real setback. Double-check everything before you hit submit.

Step 3 Make a Smart Tax Withholding Decision

This is a crucial step, and honestly, it’s one that people often overlook. When you pull pre-tax money from a Traditional IRA, it’s a taxable event. Your custodian is required to give you the option to withhold federal (and sometimes state) income taxes right then and there.

Most custodians have a default withholding rate, often 10% or 20%, for federal taxes. But here's the key: you have the right to change this amount or even elect no withholding at all.

Making the right choice here is essential for managing your tax bill down the road.

- Withholding at the Source: This works just like having taxes taken out of a regular paycheck. It’s a simple way to pre-pay your tax bill on the distribution, which seriously reduces the risk of owing a big chunk of money to the IRS later.

- Electing No Withholding: If you go this route, you’ll get the full gross amount of your withdrawal. But—and this is a big but—you are now fully responsible for paying the taxes on that income. This often means you'll need to make a separate estimated tax payment to the IRS to avoid underpayment penalties.

Failing to plan for taxes is one of the biggest mistakes you can make when taking money from an IRA. An unexpected tax bill can be a real shock to the system. So, take a minute to consider your overall financial picture, and don't hesitate to consult a tax advisor if you're unsure. Taking these practical steps ensures your withdrawal goes exactly as planned.

Smart Alternatives to Tapping Your IRA Early

Let's be blunt: taking an early withdrawal from your IRA should be your absolute last resort. Think of it as a financial nuclear option. Yes, you get cash in hand, but you're vaporizing your retirement future by killing off years of potential compound growth. Before you pull that trigger, you have to explore every other avenue.

Walking through these alternatives isn’t just about finding cash; it's about understanding the true, long-term cost of an IRA withdrawal. When you compare interest rates, repayment plans, and the overall hit to your net worth, you get a much clearer picture of which choice actually serves both the you of today and the you of tomorrow.

Evaluating Other Financial Tools

When a financial emergency pops up—and it always does—several other options are likely on the table that are far better than raiding your retirement savings. Each has its own quirks, but they all share one critical advantage: they leave your nest egg alone to keep growing.

Consider these possibilities:

- Personal Loans: An unsecured personal loan from a bank or credit union can be a quick way to get funds. Your credit score will dictate the interest rate, but that rate is often much lower than the double-whammy of taxes and penalties you’d face with an IRA distribution.

- Home Equity Line of Credit (HELOC): If you're a homeowner with some equity built up, a HELOC can be a fantastic, low-interest source of cash. It works like a credit card secured by your home—a revolving line of credit you can tap as needed, which offers a ton of flexibility.

- 401(k) Loans: If your workplace 401(k) plan allows for loans, this is often one of the best moves you can make. You’re literally borrowing from yourself. The interest you pay? It goes right back into your own account, not into a lender’s pocket. We have a detailed comparison of the pros and cons in our guide on borrowing from a 401(k) versus a 72(t) SEPP.

The Ultimate Financial Safety Net

The best way to protect your IRA? Build a dedicated emergency fund. This is your first, best, and most powerful line of defense against life’s curveballs, whether it’s a sudden job loss or a surprise medical bill. Having three to six months of living expenses parked in a high-yield savings account means you never have to ask, "can I withdraw money from my IRA?" in a state of panic.

Unfortunately, most people don't have a formal plan for handling financial shocks. You can see this in how retirement balances vary by generation. Baby Boomers, for example, have an average IRA balance of $257,002, while Millennials are sitting at just $25,109 on average.

This lack of planning continues into retirement. A recent survey found that a staggering 49% of retirees have no formal withdrawal strategy at all—they just take what they need, when they need it. This reactive approach is exactly why it’s so critical to explore every alternative before touching those retirement funds.

Before you make any move, talk to a financial professional who can look at your entire financial picture. At Spivak Financial Group, we can help you size up all your options to find a solution that tackles your immediate needs without sacrificing your retirement. Call us at (844) 776-3728 to explore your alternatives.

A Few Common Questions About IRA Withdrawals

It's easy to get tangled up in the web of IRA rules, but a few key answers can clear things up fast. Let's tackle some of the most common questions people ask when they're thinking about touching their IRA funds.

Getting your money out is usually a pretty smooth process. Once you put in a distribution request with your account custodian, an electronic funds transfer (EFT) will typically land in your bank account within 3 to 7 business days. If you're going old-school with a paper check, plan on it taking 7 to 10 business days—or maybe a bit longer—to arrive in the mail.

Handling Withdrawals and Repayments

What happens if you take money out but then change your mind? The IRS has a provision for this called a 60-day rollover. You have precisely 60 days from the moment you receive the funds to get them back into an IRA.

This is a hard and fast deadline. If you miss that 60-day window, the withdrawal is considered permanent, and you'll be on the hook for any taxes and penalties that apply. It's also important to know you can only do this kind of "indirect" rollover once every 12 months, and that limit applies across all of your IRAs combined.

Required Minimum Distributions

A lot of people ask, "Do I ever have to take money out?" For a Traditional IRA, the answer is a definite yes. The government gives you a tax break on the way in, but they want their cut eventually. Once you hit age 73, the IRS requires you to start taking Required Minimum Distributions (RMDs) every year.

This rule is how the government ensures it finally collects taxes on all that tax-deferred growth. On the flip side, Roth IRA owners have a huge advantage here—they are completely exempt from RMDs for their entire lifetime, which gives them incredible flexibility.

What about inheriting an IRA? That opens up a whole different can of worms. Spouses usually get the most favorable options and can often just treat the account as their own. For most other beneficiaries, however, the clock starts ticking: you typically have to drain the entire inherited account within 10 years. The rules here are complex, so getting professional advice is crucial to avoid a costly tax blunder.

Navigating these rules, especially for sophisticated early retirement strategies like a 72(t) SEPP, demands a high level of precision and expertise. At Spivak Financial Group, our specialty is creating compliant, penalty-free income streams from retirement accounts. Ready to unlock your financial future? Visit us at https://72tprofessor.com.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

https://72tprofessor.com