When you're facing a major financial crisis, the money sitting in your 401(k) can look like a port in a storm. The IRS provides an option called a 401(k) hardship withdrawal, which lets you tap into those retirement funds for what they define as an immediate and heavy financial need. But this isn't free money—it's a serious decision with permanent consequences for your future.

What Is a 401k Hardship Withdrawal

Think of a hardship withdrawal as the emergency brake on your retirement savings train. It’s designed for a true, unavoidable crisis, but pulling that lever brings everything to a screeching halt and comes with some serious, irreversible costs.

The most important thing to understand is that a hardship withdrawal is not a loan. You can't pay it back. The money you take out is gone forever, and so is all the compound growth it would have generated over the years.

The Rise in Financial Pressures

It's clear that more Americans are feeling the squeeze and are being forced to pull that emergency brake. We've seen a troubling surge in people resorting to hardship withdrawals. Some reports show the percentage of participants taking them jumped from just 1.7% in 2020 to 4.8% in 2024. Another major firm noted that nearly 6% of employees raided their accounts for hardship reasons in 2024, a huge leap from around 2.7% in 2018.

This trend highlights the immense financial pressure households are under, forcing them into a tough spot between paying for today's emergency and saving for tomorrow's security.

A hardship withdrawal should always be your last resort, not your first option. It permanently shrinks your retirement account and almost always triggers immediate taxes and penalties, which can significantly reduce the amount you actually receive.

Key Characteristics of a Hardship Withdrawal

Before we dive into the specific 401k hardship withdrawal rules, let’s get clear on what makes this type of distribution different from other ways you might take money from a 401(k).

Here are the defining features you absolutely must know:

- It Is Not a Loan: This bears repeating. You cannot repay the funds. Once you take the money out, that portion of your retirement savings is permanently gone.

- Immediate Tax Consequences: The amount you withdraw is generally treated as taxable income for the year. This could easily bump you into a higher tax bracket, costing you even more.

- Potential for Penalties: If you're under age 59½, you'll likely get hit with a 10% early withdrawal penalty from the IRS. This is on top of the regular income taxes you'll owe.

- Strict Eligibility Rules: You can't just decide you need the money. You have to prove an "immediate and heavy financial need" according to strict IRS definitions, and your specific 401(k) plan has to allow for these withdrawals in the first place.

Getting a firm grasp on these realities is the first step. By understanding the full picture—the rules, the costs, and the better alternatives—you can make a smarter decision that balances today's crisis with your long-term financial health.

Qualifying for a Hardship Withdrawal Under IRS Rules

Navigating the world of 401(k) hardship withdrawal rules really boils down to one critical question: does your situation count as a real emergency in the eyes of the IRS? The government sets a pretty high bar here, outlining specific "safe harbor" events that they automatically consider an "immediate and heavy financial need."

Think of it like getting through a series of locked gates. The very first one—and the most important—is controlled by the IRS. If your reason for needing the money isn't on their approved list, your request is dead in the water, no matter how dire your situation feels personally.

The IRS Safe Harbor Events

To keep things straightforward, the IRS created a clear list of circumstances that automatically qualify. Most 401(k) plans just adopt this list as-is to make administration easier and stay in compliance. If your need falls into one of these buckets, you’ve cleared the first major hurdle.

These qualifying events include:

- Significant Medical Expenses: Costs for medical care that haven't been reimbursed for you, your spouse, your dependents, or your plan beneficiary.

- Home Purchase Costs: Money needed for a down payment or other costs to buy your main home (this does not include mortgage payments).

- Higher Education Expenses: Paying for tuition, fees, and room and board for the next 12 months of postsecondary education for you, your spouse, your kids, or your dependents.

- Preventing Eviction or Foreclosure: The exact amount needed to stop you from being kicked out of your primary home or to prevent foreclosure on your mortgage.

- Funeral Expenses: Covering the costs associated with a funeral for yourself, your spouse, children, dependents, or beneficiary.

- Home Repair Costs: Certain expenses needed to fix significant damage to your principal residence.

It's crucial to understand that your plan administrator will demand proof. This isn't based on the honor system; you’ll have to produce medical bills, tuition statements, official eviction notices, or repair estimates to back up your claim.

Your Plan's Rules Matter Just as Much

Even if you check all the IRS boxes, there's another gatekeeper you have to deal with: your own 401(k) plan. It’s a common misconception that every 401(k) has to offer hardship withdrawals. That's simply not true. An employer is not legally required to include this feature in their retirement plan at all.

So, your first move should always be to check your plan's official documents or just call your plan administrator to see if hardship distributions are even an option. If they aren't, you'll have to find another way, regardless of your financial need.

You must satisfy two distinct sets of rules to get approved: the IRS's definition of a hardship and your specific 401(k) plan's rules for allowing and processing the withdrawal. One without the other is not enough.

The "Last Resort" Requirement

Finally, a hardship withdrawal has to be exactly what it sounds like: a last resort. The rules are clear that the amount you request can't be more than what's needed to solve the problem. This means you must have already tapped into any other financial resources you could reasonably access.

Before signing off, your plan administrator will require you to certify that you have no other money available. This includes:

- Insurance payouts or other reimbursements.

- Your own liquid assets (like what's in your savings or checking accounts).

- Taking a 401(k) loan, if your plan offers one and you're eligible.

Data shows that stopping a foreclosure or eviction is the top reason people take these withdrawals, making up 35% of requests. Other big ones include medical bills that exceed 7.5% of your adjusted gross income and funeral expenses up to $5,000. These strict limits really drive home the point that a hardship withdrawal is only for the most severe financial crises. You can find more data on these trends from the Plan Sponsor Council of America. This whole multi-layered process exists to protect your retirement savings, making sure they’re only used when absolutely necessary.

The True Cost of a Hardship Withdrawal

Tapping into your 401(k) during a crisis can feel like a necessary lifeline. But it’s a lifeline with a heavy anchor attached. The true cost of a hardship withdrawal goes far beyond the dollar amount you need right now. It's a multi-layered financial hit that costs you immediately in taxes and penalties, and then keeps on costing you for decades through lost growth.

Before you make this irreversible decision, you need to understand every dollar that will vanish in the process. This isn't just about solving today's problem; it's about the permanent hole you’re about to punch in your financial future.

The Immediate Hit From Taxes

The very first cost you'll run into is income tax. The moment you take that withdrawal, the IRS treats the money as ordinary income for the year, just like your paycheck. That means it’s subject to both federal and, in most places, state income taxes.

Let's say you're in the 22% federal tax bracket and your state has a 5% income tax. Right off the top, a combined 27% of your withdrawal is gone before you can even use it. This is a nasty surprise for many, as they budget for the gross amount, not the much smaller net sum that actually hits their bank account.

This can create a dangerous cycle. If you need a specific amount for your emergency, you might have to withdraw an even larger sum just to cover the taxes. This, in turn, increases your tax bill and digs an even deeper hole in your retirement savings.

The Painful 10% Early Withdrawal Penalty

On top of the income taxes, there's another immediate sting for most people. If you are under age 59½, the IRS will typically tack on an additional 10% early withdrawal penalty. This is a straightforward tax designed purely to discourage people from raiding their retirement accounts before they actually retire.

When you combine this penalty with income taxes, it’s a devastating one-two punch. That 27% tax rate from our example suddenly jumps to 37%. The amount of cash you actually get to keep shrinks dramatically, making a hardship withdrawal a horribly inefficient way to access your own money.

To get a clearer picture of how quickly the costs add up, let's break down a hypothetical $20,000 withdrawal.

Illustrative Cost of a $20,000 Hardship Withdrawal

| Item | Amount | Description |

|---|---|---|

| Gross Withdrawal Amount | $20,000 | The total amount requested from your 401(k) plan. |

| Federal Income Tax (22%) | -$4,400 | Taxes owed based on your federal income tax bracket. |

| State Income Tax (5%) | -$1,000 | Taxes owed based on your state's income tax rate (varies). |

| Early Withdrawal Penalty (10%) | -$2,000 | The additional penalty for taking money out before age 59½. |

| Total Immediate Cost | -$7,400 | The total amount lost to taxes and penalties right away. |

| Net Cash Received | $12,600 | The actual cash you have left to address your hardship. |

As you can see, needing $20,000 doesn't mean taking out $20,000. You lose a huge chunk right away, which often isn't enough to solve the problem that caused the hardship in the first place.

A hardship withdrawal is not a dollar-for-dollar solution. For every dollar you need, you might have to pull out $1.40 or more from your 401(k) just to cover the taxes and penalties, permanently removing that entire amount from your future.

The Invisible Killer: Lost Compound Growth

The most significant cost isn't the immediate taxes or penalty—it's the money your savings would have earned for the rest of your life. This is the silent, devastating impact of lost compound growth. When you pull money out of your 401(k), you aren’t just losing the principal; you are forfeiting all its future earnings.

Consider this real-world example:

- You take a $20,000 hardship withdrawal at age 35.

- After taxes and penalties (assuming our 37% combined hit), you only receive $12,600 to solve your problem.

- But the real damage is what happens to that $20,000 you took out. If it had been left in your account earning an average of 7% per year, it would have grown to approximately $152,245 by the time you turned 65.

By taking that withdrawal, you didn't just spend $20,000. You effectively erased over $150,000 from your retirement nest egg. This phenomenon, known as retirement "leakage," has a profound impact.

Research from the Employee Benefit Research Institute shows that participants who take just one hardship withdrawal often face a 36% higher retirement deficit. This is especially damaging for workers with smaller balances, who are twice as likely to raid their accounts if they lack emergency savings.

This permanent loss is exactly why exploring every possible alternative is so critical. The immediate relief is tempting, but the long-term price you pay can compromise your financial security for decades.

Navigating the Hardship Withdrawal Application Process

So you've weighed the steep costs and decided a hardship withdrawal is the only path forward. What now? The next step is tackling the application itself. It can feel like a mountain of paperwork, especially when you're already stressed, but knowing what's ahead can make the whole process much more manageable.

Think of it this way: the entire application hinges on proving your financial need is both legitimate and urgent. Your 401(k) plan administrator is the gatekeeper, and their job is to make sure every dollar that goes out meets the strict rules set by both the IRS and your specific plan.

Kicking Off the Request and Gathering Your Proof

Your first move is always to get in touch with your 401(k) plan administrator or your company's HR department. They’ll give you the official forms and, more importantly, a detailed checklist of the documents you need to submit. This is where you have to be meticulous—incomplete or fuzzy paperwork is the quickest way to get a denial.

You can't just say you're in financial trouble; you have to prove it with official documents.

- Medical Bills: You'll need actual invoices from the hospital or doctor's office, plus an explanation of benefits (EOB) from your insurer that shows what they refused to cover.

- Preventing Eviction/Foreclosure: This requires a formal, written eviction notice from a landlord or an official foreclosure notice from your mortgage lender. A simple late notice won't cut it.

- Tuition Payments: You’ll need to provide an itemized bill from the college or university that details the tuition and fees for the next 12 months.

- Buying a Home: A signed purchase agreement or other closing documents are what they'll be looking for here.

This documentation is your hard evidence of an "immediate and heavy financial need." Plan administrators are legally required to verify these claims, so being thorough is your best strategy.

What About the Self-Certification Option?

Recent changes from the SECURE 2.0 Act have created a shortcut for some people. Depending on your plan, you might be able to self-certify that you meet the requirements without having to submit all the backup documents right away.

With this option, you simply provide a written or electronic statement confirming you have a qualifying need, that the amount you're requesting is no more than necessary, and that you've exhausted other resources. But here’s the catch: you still have to be ready to produce all the documentation if the IRS or your plan administrator asks for it later.

This can definitely speed things up, but it doesn't mean you can skip gathering your proof. For a closer look at what your own plan might demand, it's a good idea to research the specific 401(k) terms of withdrawal, as the rules can vary quite a bit from one provider to another.

Managing Timelines and Expectations

Once you've submitted your application and all the required paperwork, the review process usually takes several business days. After it's approved, you can expect the funds to hit your bank account in another 3 to 10 business days.

All told, it's wise to plan for a total timeline of one to three weeks from start to finish. Don't make any promises or financial commitments based on getting the money overnight. This process takes patience, and any missing piece of information can cause major delays right when you can least afford them.

Smarter Alternatives to Accessing Your Retirement Funds

Before pulling the trigger on a hardship withdrawal, it’s absolutely critical to pause and look at all your options. Committing to a hardship withdrawal without checking out the alternatives is a bit like taking out a payday loan without first asking a friend for help. Fortunately, you have smarter, less damaging ways to get the cash you need without torching your long-term financial health.

These alternatives are designed to keep your retirement savings intact and help you sidestep that brutal combination of taxes, penalties, and lost future growth. Understanding them puts you back in the driver's seat, letting you control your financial future instead of letting a crisis call the shots.

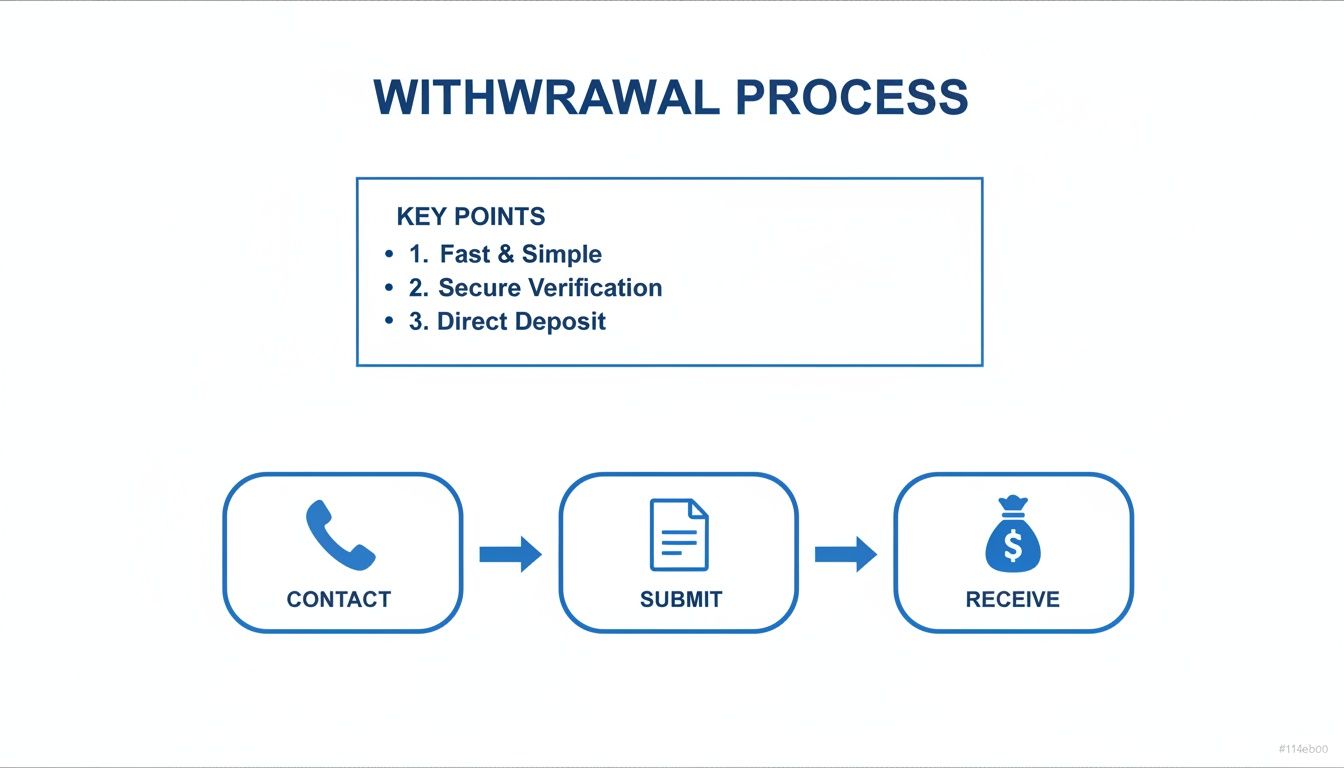

The process for a hardship withdrawal might seem simple, but its simplicity hides the real cost down the road.

As you can see, the path looks straightforward: contact your administrator, hand over the paperwork, and get your money. What this graphic doesn't show you are the severe financial consequences that follow.

The 401k Loan: A Better First Step

For many people facing a cash crunch, a 401(k) loan is a much better first choice. Think of it this way: a withdrawal is a permanent goodbye to your money, but a loan is just a temporary arrangement where you're borrowing from yourself.

The biggest win here is that you repay the loan—plus interest—right back into your own account. Sure, you might miss out on some market growth while the money is out, but you are systematically rebuilding what you took. And that interest? It goes back into your own 401(k), not to some bank or lender.

A 401(k) loan also helps you dodge the immediate, painful hit of a hardship withdrawal. There are no income taxes and no 10% early withdrawal penalty as long as you stick to the repayment plan. The one major catch is if you leave your job; the loan often becomes due almost immediately, which can create a whole new financial headache.

72(t) SEPP: A Strategic Solution for Ongoing Income

A loan is great for a one-off emergency, but what if you need a steady, reliable stream of income? This is where a 72(t) Substantially Equal Periodic Payments (SEPP) plan becomes an incredibly powerful, though lesser-known, tool. It’s a specific provision in the tax code that allows you to take distributions from your retirement account before age 59½ without getting hit with penalties.

You can think of a 72(t) SEPP as a private pension you create for yourself. It’s perfect for situations that require consistent cash flow, like bridging an income gap if you lose your job, funding an early retirement, or covering long-term medical expenses.

Under a 72(t) plan, the IRS calculates a specific annual amount you can withdraw for at least five years or until you turn 59½, whichever is longer. As long as you follow that schedule to the letter, you completely avoid the 10% early withdrawal penalty. You’ll still owe regular income tax on the money, but skipping the penalty is a massive financial victory.

A 72(t) SEPP can transform your retirement account from a locked box into a flexible income source. It gives you a structured way to access your funds without the destructive force of a hardship withdrawal, making it an ideal strategy for planned financial needs.

Setting one up requires precision and very careful planning, because if you mess up the payment schedule, the penalties can come roaring back retroactively. The process often involves moving funds from a 401(k) to an IRA to get the flexibility needed. For anyone still working, understanding the rules for a 401(k) rollover to an IRA while still employed is the essential first step. This is exactly what we specialize in at Spivak Financial Group—guiding clients through this complex process to unlock their funds without penalties.

Comparing Your Options Side-by-Side

Choosing the right path really boils down to your specific situation—the size and urgency of your financial need, your timeline, and what you want for your future. Seeing the options laid out next to each other can make the best choice jump right out.

401k Hardship Withdrawal vs. 401k Loan vs. 72(t) SEPP

| Feature | Hardship Withdrawal | 401k Loan | 72(t) SEPP |

|---|---|---|---|

| Repayment | Not allowed; money is permanently gone. | Required; you pay yourself back with interest. | Not a loan; no repayment is necessary. |

| 10% Penalty | Yes, if under 59½. | No, unless you default on the loan. | No, the plan is designed to avoid it. |

| Income Tax | Yes, on the entire withdrawal amount. | No, not considered taxable income. | Yes, on each distribution payment. |

| Impact on Savings | Severe; permanent loss of principal and growth. | Minimal; principal is restored through payments. | Controlled; you take structured distributions. |

| Best For | A true last-resort, one-time emergency. | A one-time need when you can afford repayments. | Creating a consistent, penalty-free income stream. |

At the end of the day, a hardship withdrawal should only be seen as a financial tool of last resort. By first exploring strategic alternatives like a 401(k) loan or a 72(t) SEPP, you can solve your immediate problem while protecting the retirement you’ve worked so hard to build.

Your Hardship Withdrawal Questions, Answered

Even when you grasp the basics of 401(k) hardship withdrawal rules, it's the specific, real-world questions that matter most. The regulations can feel like a tangled mess, and getting a clear answer is critical when you’re facing a tough financial corner. Let's tackle the most common questions we hear to clear up any lingering doubts.

Can I Take a Hardship Withdrawal for Credit Card Debt?

No, you absolutely cannot. This is one of the most common misconceptions out there.

The IRS is incredibly strict about what it considers an "immediate and heavy financial need," and consumer debt doesn't even come close. The list is reserved for dire situations like preventing foreclosure, paying for significant medical bills, or covering funeral expenses—not managing high-interest credit cards. Your plan administrator will deny the request flat out, as it’s nowhere near the IRS safe harbor guidelines.

Do I Have to Pay Back a 401(k) Hardship Withdrawal?

No, and that’s the biggest problem. A hardship withdrawal is not a loan, so there's nothing to repay. The money is simply gone for good.

This is what makes it so different from a 401(k) loan and also what makes it so financially damaging.

You don't just lose the money you take out. You permanently lose all the future compound growth that money would have generated over decades. This devastating long-term loss comes on top of the immediate hit from income taxes and the 10% early withdrawal penalty.

How Long Does It Take to Get the Money?

Don't expect the cash to show up overnight. While the timeline can vary between plan administrators, a reasonable estimate is anywhere from one to three weeks.

The process isn't instant. Here’s a rough breakdown of what happens:

- You Submit the Application: This part is on you. You'll need to gather every required document—the foreclosure notice, the medical invoice—and formally submit your request.

- The Administrator Reviews It: Your plan administrator will then comb through your application and proof, which usually takes a few business days.

- The Funds Are Sent: Once approved, it takes another 3 to 10 business days for the money to be electronically transferred into your bank account.

You have to factor this waiting period into your plans to avoid making a stressful situation even worse.

Can My Employer Deny My Hardship Withdrawal Request?

Yes, absolutely. Approval is never a sure thing, and a denial can happen for several valid reasons.

For starters, employers aren’t required by law to offer hardship withdrawals in their 401(k) plans. If the feature isn't in your plan documents, you simply can't take one.

Even if your plan does allow them, you can still be denied if you:

- Don't Meet the IRS Criteria: The reason you need the money isn't on the short list of approved events.

- Fail to Provide Adequate Proof: You can't just say you have a hardship; you have to prove it with specific, official documents. No paperwork, no approval.

- Haven't Tried Other Options First: Many plans require you to take a 401(k) loan (if available) before you can even apply for a hardship withdrawal. Skipping this step is a common reason for denial.

Knowing these potential roadblocks can help you build a stronger application and set realistic expectations.

Facing a financial hardship is stressful enough without navigating complex rules alone. While a hardship withdrawal is an option, it's often the most destructive to your long-term financial security. At Spivak Financial Group, we specialize in smarter strategies like the 72(t) SEPP that can provide the income you need without the devastating penalties and lost growth. To explore a better path forward, contact us or visit us online.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

https://72tprofessor.com