Yes, you can absolutely make a 401(k) withdrawal at age 55 without that dreaded 10% penalty, all thanks to a special IRS provision. It’s widely known as the “Rule of 55,” and it’s a game-changer if you leave your job during or after the calendar year you turn 55.

How to Access Funds Penalty-Free

The standard age for penalty-free access to your retirement funds is 59½. Pull money out before then, and you’re typically hit with a painful 10% early withdrawal penalty on top of your regular income taxes. Ouch.

But the Rule of 55 creates a valuable workaround for those who part ways with their employer a little earlier than planned.

Think of it as an early access key to your retirement savings. The catch? This key is very specific. It only works on the 401(k) plan from the company you just left. It won’t unlock funds from previous jobs’ 401(k)s or any IRAs you might have.

To give you a clearer picture, let’s break down the core components of the Rule of 55 in a simple table.

Rule of 55 At a Glance

| Key Component | Explanation |

|---|---|

| Minimum Age | You must be at least 55 years old. |

| Separation Event | You must leave your job (quit, get laid off, or fired) in the calendar year you turn 55 or later. |

| Plan Specificity | The rule only applies to the 401(k) or 403(b) from the employer you just left. |

| Penalty Avoidance | Successfully avoids the 10% early withdrawal penalty. |

| Tax Impact | Withdrawals are still taxed as ordinary income. The penalty is waived, not the tax. |

This table neatly sums up the essentials, but the real magic is in understanding how these pieces fit together in the real world.

Key Aspects of the Rule

The IRS didn’t create this rule by accident; it’s designed to give early retirees a bit more financial breathing room. At its heart, the Rule of 55 lets you take money from your most recent employer’s 401(k) or 403(b) plan without the 10% penalty if you separate from service in the year you turn 55 or older.

Let’s be crystal clear on a few non-negotiables:

- Separation from Service: This is the trigger. You must leave your job—whether you resign, get laid off, or are let go—in or after the calendar year you reach age 55.

- Plan Specificity: Again, this is crucial. The rule only applies to the plan of the employer you just separated from. Money in old 401(k)s or IRAs is still locked up until 59½.

- Tax Implications: You dodge the 10% penalty, but you can’t escape Uncle Sam. Every dollar you withdraw is considered ordinary income and will be taxed in your bracket for that year.

A Practical Example

Let’s meet Sarah, an accountant. She gets laid off from her job in March. Her 55th birthday isn’t until August of that same year.

Because her “separation from service” happened in the calendar year she turned 55, she’s eligible to start taking penalty-free distributions from that specific company’s 401(k) right away.

She could take a lump sum to bridge an income gap or set up periodic payments. Either way, each withdrawal gets added to her taxable income for the year. This flexibility is exactly why understanding how to take money from your 401(k) under these special rules is so vital for smart financial planning.

How to Qualify for the Rule of 55

Knowing the Rule of 55 exists is one thing, but actually qualifying for it is another game entirely. The IRS has some very strict, non-negotiable criteria. Getting it wrong can easily trigger that painful 10% early withdrawal penalty you’re working so hard to sidestep.

So, let’s get into the weeds. To use this powerful provision, you have to nail the timing and know exactly which accounts are in play.

The Separation from Service Requirement

This is the absolute linchpin of the whole rule. Everything hinges on when you leave your employer. To qualify, you must leave your job—whether you quit, get laid off, or retire—during or after the calendar year you turn 55.

The timing here is critical, so let’s be crystal clear. Say your 55th birthday is in November. If you leave your job in February of that same year (when you’re still 54), you qualify. But if you leave in December at age 54, you’ve missed the window. Even if you wait until the next year to touch the money, it’s too late.

Key Takeaway: The calendar year you leave your job is what counts, not your exact age on that day or the year you decide to take the money. You must separate from service in the year you turn 55 or any year after.

It’s also worth noting that the reason you leave doesn’t matter one bit. Whether it was your choice to retire or the company’s decision to downsize, as long as the timing lines up with the rule, you’re good to go.

Which Retirement Accounts Qualify?

This is a major tripwire where a lot of people make a costly mistake. The Rule of 55 is incredibly specific about which piggy bank you can open.

- Your Current Employer’s 401(k) or 403(b): The rule only applies to the retirement plan of the employer you just separated from. This is the one and only account you can access penalty-free under this provision.

- IRAs and Old 401(k)s: The rule does not apply to any of your Individual Retirement Accounts (IRAs). It also doesn’t work for 401(k)s you have sitting with previous employers.

This leads to a crucial warning: If you roll your qualifying 401(k) over into an IRA, you immediately lose your Rule of 55 eligibility for those funds. If you need the cash, take your distributions before you even think about doing a rollover.

Special Circumstances and Common Questions

While the main rules are pretty black and white, there are a few unique situations and common questions that pop up all the time.

One of the biggest exceptions is for qualified public safety employees. This group includes certain federal, state, and local government workers like police officers, firefighters, and EMTs. For these folks, the magic number isn’t 55—it’s 50. They can start taking penalty-free withdrawals once they leave their job in the year they turn 50 or later.

Here are a few other questions we hear a lot:

- Does getting a new job mess things up?

Nope. You can leave your job at 56, start taking distributions from that company’s 401(k), and immediately start a new job somewhere else. Your new employment doesn’t affect your access to your old 401(k) under this rule. - Do I have to take the money out right away?

Not at all. As long as you met the separation rule, you can leave the money in that 401(k) and decide to take withdrawals later on—maybe at age 57 or 58. The key is just keeping the funds in that specific employer’s plan until you’re ready.

Nailing these qualifications is the first real step to using the 401k withdrawal at age 55 rule to your advantage. With the right timing and a clear plan, you can build a financial bridge to whatever’s next without giving a chunk of your money back in penalties.

The Financial Impact of an Early 401k Withdrawal

While the Rule of 55 offers a fantastic way to dodge the dreaded 10% early withdrawal penalty, it’s not a get-out-of-jail-free card. Think of it like a coupon that waives the cover charge at a club—you still have to pay for your drinks once you’re inside. Every single dollar you pull from your 401(k) is taxed as ordinary income, and that can have some serious financial ripple effects.

This isn’t just a minor footnote; it can completely change your tax situation for the year. A large withdrawal can easily bump you into a higher federal and state tax bracket. That means a much bigger slice of your money ends up going to Uncle Sam than you probably planned for.

How Taxes Can Take a Bite Out of Your Withdrawal

Let’s look at a real-world example to see how this plays out. Imagine a married couple, both 56 years old, with a combined taxable income of $90,000 for the year. This puts them comfortably in the 22% federal tax bracket.

Now, let’s say one spouse leaves their job and decides to take a $100,000 lump-sum distribution from their 401(k), using the Rule of 55. This isn’t just a simple transfer of funds; it’s a major taxable event.

- Original Taxable Income: $90,000

- 401(k) Withdrawal: +$100,000

- New Taxable Income: $190,000

That one withdrawal catapults their income into the next tax bracket. While some of their income is still taxed at the lower rates, a big chunk of that $100,000 withdrawal is now taxed at 24% instead of 22%. This is a common trap that catches many early retirees by surprise, leaving them with a much smaller net amount than they expected. Properly navigating these tax rules is a huge part of avoiding expensive 401(k) early withdrawal penalties and surprise tax bills.

The Hidden Cost of Lost Compounding

Beyond the immediate tax hit, there’s a quieter, more sinister cost: the loss of future growth. When you pull money out of your 401(k) at 55, you aren’t just taking the principal. You’re robbing that money of its ability to work for you and grow for another decade or more.

Think of every dollar in your 401(k) as a tiny employee. By taking it out early, you’re forcing that employee into retirement when they could have been generating more wealth for you. This lost potential, fueled by the magic of compound interest, can be staggering.

A $50,000 withdrawal at age 55 might seem manageable, but it could mean giving up more than $98,000 in potential growth by the time you turn 65, assuming a modest 7% average annual return. The true cost isn’t just what you take out today—it’s the future wealth you’ll never get to see.

And this isn’t an uncommon scenario. According to a recent Vanguard Group report, early withdrawals from retirement accounts just hit an all-time high of 3.6%, up from 2.8% the year before. While the Rule of 55 provides a penalty-free door, walking through it doesn’t erase the long-term impact of tapping into funds that haven’t fully matured. You can explore more safe withdrawal strategies from SmartAsset to understand the bigger picture.

Weighing Your Needs and Your Future

Ultimately, deciding whether to make a 401k withdrawal at age 55 comes down to a balancing act. You have to weigh your immediate financial needs against the long-term security you’re potentially sacrificing.

For some, it’s an essential bridge to cover expenses until a pension or Social Security kicks in. For others, the tax consequences and lost compounding might make other options—like a home equity line of credit or tapping into a different savings account—the smarter move. The key is to make the decision with your eyes wide open, fully understanding both the upfront tax bill and the long-term opportunity cost.

Comparing the Rule of 55 to Other Early Access Options

The Rule of 55 is a fantastic tool for getting to your retirement funds early, but it’s not the only key in the lockbox. When you’re planning for early retirement, another common strategy you’ll run into is the 72(t) distribution, also known as a Substantially Equal Periodic Payment (SEPP) plan.

Getting a handle on the core differences between these two is absolutely critical. Choosing the right one depends entirely on your financial needs and what you want your early retirement to look like.

Think of the Rule of 55 as a flexible line of credit. It lets you take withdrawals when you need them—maybe a big lump sum one year to buy a boat, smaller amounts the next to cover property taxes, and then nothing at all the year after. You’re in the driver’s seat when it comes to the timing and size of your distributions, which is a huge advantage for life’s unpredictable expenses.

A 72(t) SEPP, on the other hand, is much more like a fixed-income annuity. It’s built to give you a steady, predictable stream of cash over a long time. Once you kick off a 72(t) plan, you are locked into a very rigid schedule of identical payments, calculated by the IRS, that you must take every single year.

The Rule of 55 vs. 72(t) SEPP Plans

The decision between these two often boils down to a simple question: Do you need a flexible source of cash or a predictable income stream? The Rule of 55 gives you freedom, while a 72(t) plan provides structure. Both can help you dodge that nasty 10% early withdrawal penalty, but they play by completely different rules and serve very different purposes.

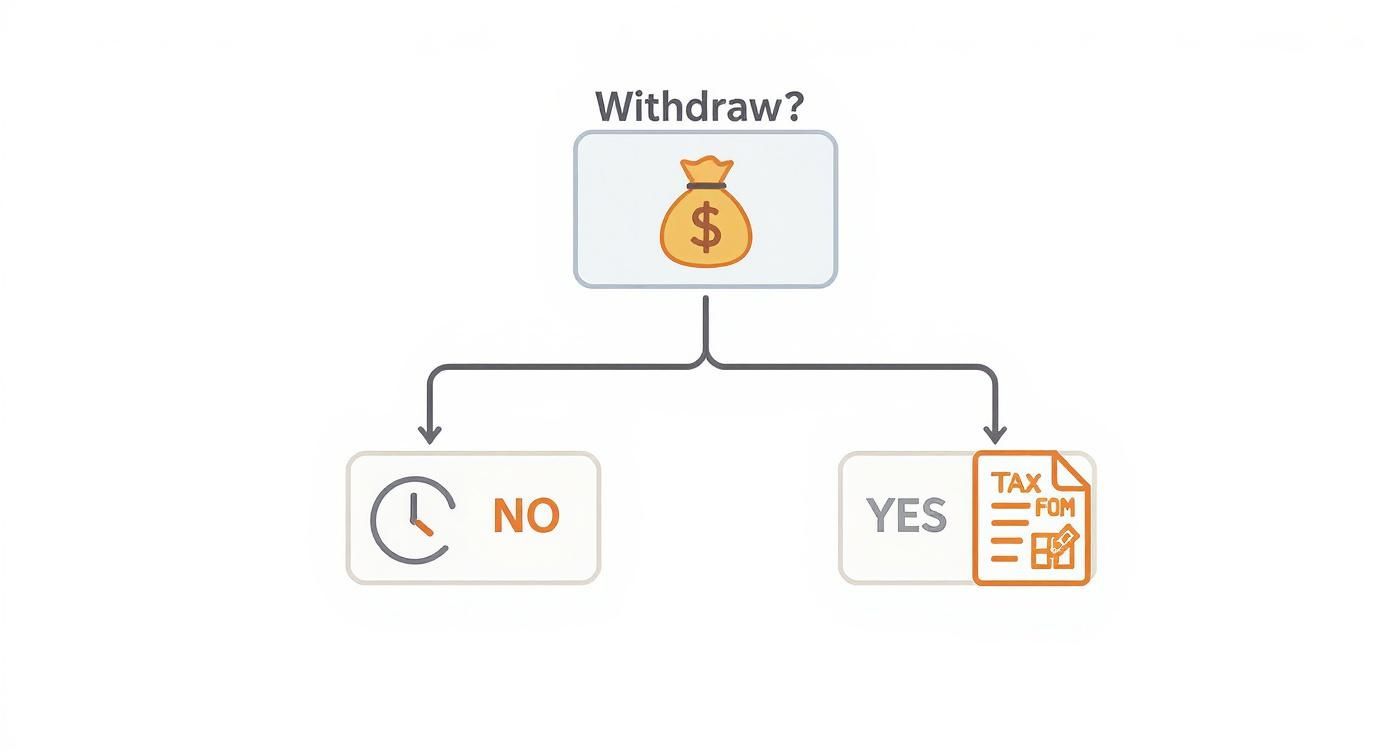

To help you picture these differences, the decision tree below simplifies the first choice you have to make when thinking about a 401k withdrawal age 55 or another early access method.

This graphic lays out the first step: either commit to a withdrawal and get ready for the tax bill, or let your investments keep growing. Your choice here really sets the stage for which strategy—the flexible Rule of 55 or the structured 72(t) SEPP—might be the right fit for you.

Key Distinctions You Must Understand

The differences go way beyond just payment flexibility. Each rule has its own specific requirements for account types, rules about making changes, and big penalties for messing up. A mistake with either one can be incredibly expensive, wiping out the very penalty-free benefit you were hoping for.

Let’s put them side-by-side to see how their core features stack up.

Rule of 55 vs. 72(t) SEPP Plans

| Feature | Rule of 55 | 72(t) SEPP |

|---|---|---|

| Eligible Accounts | Only the 401(k) or 403(b) of your most recent employer. IRAs are not eligible. | Applies to IRAs, 401(k)s, and other qualified retirement accounts. |

| Withdrawal Flexibility | Highly flexible. You can take lump sums, periodic payments, or no payments at all. | Extremely rigid. You must take a specific, fixed payment amount each year. |

| Age Requirement | Must separate from service in the year you turn 55 or later (or 50 for public safety workers). | Can be started at any age before 59½. |

| Plan Duration | No set duration. You can take withdrawals as needed until the money runs out or you reach 59½. | Must continue for five full years or until you reach age 59½, whichever is longer. |

| Consequences | A wrong move (like an early IRA rollover) disqualifies you. All withdrawals are taxed as income. | Any modification to the payment schedule results in retroactive 10% penalties on all past distributions, plus interest. |

The main trade-off is pretty clear: The Rule of 55 gives you incredible freedom but is stuck to a single 401(k) account. In contrast, a 72(t) SEPP can be used with almost any retirement account but demands that you stick to its strict payment schedule for years without fail.

If your early retirement plan needs a consistent, paycheck-like income to cover monthly bills, a 72(t) plan might be just what you need. But if you think you’ll have large, irregular expenses or want the option to stop withdrawals if you go back to work, the flexibility of the Rule of 55 is a much better bet.

If you’re leaning toward the structured income route, you can learn more about the complexities of Substantially Equal Periodic Payment rules to see if this strategy really fits your needs. In the end, the best choice depends entirely on your personal financial roadmap.

Building Your Early Retirement Bridge Strategy

Making the leap into early retirement using the Rule of 55 isn’t about just unlocking a pot of money. It’s about building a solid financial “bridge”—one that can carry you from your last paycheck all the way to age 59½ and beyond. This requires more than just access; it demands a real strategy to make sure your withdrawals cover today’s needs without jeopardizing your long-term security.

The first plank in this bridge is knowing exactly how much you’ll need. A 401(k) withdrawal at age 55 has to be a calculated decision, not a guess. You need to map out every expense, essential and otherwise, to figure out the precise amount you need to pull from your account each year.

Calculating Your Income Needs

Before you touch a single dollar, it’s time to get brutally honest with your numbers and create a detailed early retirement budget. This isn’t just about scraping by; it’s about funding the life you’ve worked so hard to build.

Your budget needs to account for the basics, of course, but also for the new costs that come with your new freedom.

- Core Living Expenses: Think mortgage or rent, utilities, groceries, and transportation. These are your non-negotiables.

- Healthcare Costs: This is the big one. You’ll need to realistically estimate premiums for COBRA or a plan from the Affordable Care Act (ACA) marketplace. Don’t underestimate this line item.

- Discretionary Spending: What does retirement look like for you? Factor in travel, hobbies, dining out, and anything else you plan to enjoy.

- Taxes: Don’t forget the IRS. Every withdrawal is treated as ordinary income, so you have to set aside funds for federal and state taxes.

Once you have that annual number nailed down, you can structure your withdrawals to match it. This deliberate approach is crucial. It keeps you from withdrawing too much, which could easily push you into a higher tax bracket and drain your savings far too quickly.

Advanced Strategies for Your Bridge

With your income needs sorted, you can start thinking more strategically. The money you access through the Rule of 55 isn’t just for paying bills; it can be a powerful lever to maximize your other retirement assets.

One of the smartest plays is using your 401(k) funds to delay taking Social Security. It’s simple but incredibly effective. For every year you wait past your full retirement age (up to age 70), your monthly benefit jumps by about 8%.

By using your 401(k) as a bridge to cover expenses from, say, age 62 to 70, you could potentially boost your lifetime Social Security income by over 75%. That one decision can lock in a much larger, inflation-protected income stream for the rest of your life.

This move requires careful management, though. You have to ensure you have enough to live on without running your 401(k) dry. According to recent NerdWallet data, the average 401(k) balance for people aged 55 to 64 is around $271,320, with the median being $95,642. These numbers give you a ballpark of what many early retirees are working with. You can learn more about retirement balance trends from NerdWallet to see where you stand.

Securing Your Healthcare Coverage

The final pillar of your retirement bridge—and arguably the most critical—is healthcare. When you leave your job, your employer-sponsored health insurance usually goes with it, and Medicare doesn’t kick in until age 65. A single unexpected medical issue could completely derail your financial plans if you’re not covered.

You have a few solid options to bridge this gap:

- COBRA: This lets you keep your old employer’s health plan, typically for up to 18 months. The coverage is familiar, but it’s often the most expensive choice since you’re footing the entire bill plus an administrative fee.

- ACA Marketplace: The Affordable Care Act marketplace offers various health plans. The key here is that based on your income—which you now control through your withdrawals—you might qualify for subsidies that make the premiums much more manageable.

- Spouse’s Plan: If your spouse is still working, getting added to their employer’s plan is often the easiest and most cost-effective path forward.

Healthcare isn’t an afterthought; it’s a cornerstone of a successful early retirement. By carefully calculating your needs, using your 401(k) to boost other benefits, and locking in solid health coverage, you can build a bridge that’s strong enough to carry you to a secure and enjoyable retirement.

Common Mistakes to Avoid with the Rule of 55

The Rule of 55 is a fantastic tool for getting a head start on retirement, but its apparent simplicity can be a bit of a trap. A few common, yet very expensive, mistakes can quickly turn this penalty-free opportunity into a major financial headache.

Knowing what these pitfalls are is the key to using the 401(k) withdrawal age 55 rule correctly and keeping your retirement plans on solid ground.

The single biggest error is also the one you can’t undo. A lot of people think the first logical step is to roll their 401(k) into an IRA for better investment options or easier management before they start taking money out.

This is a critical mistake. The moment you move your 401(k) funds into an IRA, you permanently lose the ability to use the Rule of 55 for that money. The rule applies only to the 401(k) plan from the employer you just left.

Crucial Warning: Do not roll over your 401(k) funds to an IRA until after you have taken all the distributions you need under the Rule of 55. An IRA rollover will immediately disqualify those funds from this special provision, subjecting any subsequent withdrawals before age 59½ to the 10% penalty.

Failing to Confirm Your Plan Allows It

Another surprisingly common misstep is just assuming the Rule of 55 is a universal benefit. While the IRS gives this exception the green light, your employer doesn’t have to offer it in their 401(k) plan. It’s not a legal requirement, and plenty of plans simply don’t allow for these kinds of partial distributions.

Before you hand in your notice or make any big career decisions based on tapping into these funds, you have to take one vital step. Get in touch with your plan administrator or HR department and ask them directly: “Does our 401(k) plan permit penalty-free withdrawals if I leave the company in or after the year I turn 55?”

Getting that confirmation in writing is always the smartest move. If they say “no,” then the Rule of 55 is off the table for that specific plan, and you’ll need to look at other strategies.

Underestimating Your Tax Bill

Getting around the 10% penalty feels like a big win, but that’s only half the battle. A very common mistake is forgetting about the income tax hit that comes with a large withdrawal. People get so focused on avoiding the penalty that they forget every single dollar they take out is taxed as ordinary income.

Let’s say you decide to pull out $80,000 to pay off your mortgage. That entire amount gets tacked onto your other income for the year, which can easily bump you into a much higher tax bracket than you’re used to.

Here are a few tax-related blunders we see all the time:

- Forgetting about state taxes: Most states also tax retirement income, adding another layer to your total tax bill.

- Not planning for withholding: Your plan will most likely automatically withhold 20% for federal taxes on a distribution. But if your actual tax rate is higher, that won’t be enough to cover your liability, leaving you with a nasty surprise come tax time.

- Ignoring the ripple effects: A big withdrawal can also mess with other parts of your financial life, like making more of your Social Security benefits taxable or making you ineligible for certain tax credits.

By sidestepping these common errors, you can make sure your 401(k) withdrawal at age 55 works as a helpful financial bridge, not an unexpected trap. Always double-check your plan’s rules, take your money out before doing any rollover, and have a solid plan for the taxes.

Getting Into the Weeds: Your Rule of 55 Questions Answered

When you start digging into the details of a 401(k) withdrawal at age 55, a lot of specific, practical questions bubble up. Let’s tackle some of the most common ones we hear from clients.

Can I Use the Rule of 55 and Then Get Another Job?

Absolutely. This is a big one, and the answer is a clear yes. The entire rule hinges on your separation from service with the company that holds the 401(k) you want to tap into.

What you do after you leave that job is your business. Taking on a new role with a different company doesn’t change a thing. You can start taking penalty-free distributions from your old employer’s 401(k) while happily collecting a paycheck somewhere else. It’s one of the key flexibilities built right into the rule.

Do I Have to Take the Money Immediately at Age 55?

Not at all. There’s no shot clock on this. As long as you left your job during or after the calendar year you hit age 55, you’ve basically unlocked the option to take penalty-free withdrawals.

You can let the money sit in that 401(k) for a year or two (or more) before you decide to start distributions. The critical thing to remember is that you must take the money directly from that specific 401(k) before you roll it into an IRA. A rollover slams the door on your Rule of 55 access for good.

Important Reminder: The Rule of 55 is a 401(k) and 403(b) provision only. Once those funds move into an IRA, they have to play by IRA rules, which don’t have this age 55 exception.

Does the Rule of 55 Apply to My IRA?

No, and this is probably the most crucial distinction to understand. It’s a mistake that can be costly. The Rule of 55 is exclusive to employer-sponsored plans like 401(k)s and 403(b)s, and only the one connected to the job you just left.

It does not apply to any of your Individual Retirement Accounts (IRAs), including SEP IRAs or SIMPLE IRAs. Any money sitting in an IRA is typically locked up until age 59½ if you want to avoid that 10% early withdrawal penalty, unless another specific exception applies.

Figuring out these complex retirement rules is a heavy lift, but you don’t have to tackle it alone. At Spivak Financial Group, our specialty is creating smart, penalty-free income streams for people planning an early retirement.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

See what’s possible for you at https://72tprofessor.com.