Early retirement planning is all about building enough wealth to stop working for a paycheck well before the traditional retirement age of 65. It’s a game plan, plain and simple. You focus on saving aggressively, investing smart, and setting up an income stream that can support your lifestyle for what could be a very long time. This isn't something you can wing; it requires a detailed financial blueprint, often mapped out decades in advance.

What Early Retirement Planning Really Means

Let's get one thing straight: retiring early isn't just about hitting a finish line. It's about buying your freedom. It’s about swapping mandatory workdays for more time with family, chasing a passion project, or finally traveling the world. The real goal here isn’t just to quit your job—it's to achieve financial independence, that sweet spot where your assets generate enough income to cover all your bills, forever.

Think of it this way. Traditional retirement is like a slow, steady walk up a long hill. Early retirement, on the other hand, is like building a chairlift. It takes a lot more engineering, a detailed blueprint, and a ton of heavy lifting at the start, but it gets you to the top much, much faster.

To make this happen, you need a solid foundation. Below are the four essential pillars that every successful early retirement plan is built on.

The Four Pillars of Early Retirement Planning

This table breaks down the fundamental components you'll need to focus on to build a realistic and successful early retirement plan.

| Pillar | Objective | Key Actions |

|---|---|---|

| Aggressive Savings | Maximize the gap between your income and expenses to fuel your investments. | Create a detailed budget, track every dollar, and automate savings to pay yourself first. Aim for a savings rate of 25% or higher. |

| Intelligent Investing | Grow your capital faster than inflation to build a substantial nest egg. | Invest consistently in a diversified portfolio of low-cost index funds or ETFs. Understand your risk tolerance and stay the course. |

| Tax Optimization | Keep more of your money by minimizing your tax burden now and in retirement. | Maximize contributions to tax-advantaged accounts like 401(k)s and IRAs. Explore strategies like tax-loss harvesting. |

| Sustainable Withdrawals | Create a reliable income stream from your assets that won't run out. | Understand the 4% rule and plan for tax-efficient withdrawal strategies, especially if you retire before age 59.5. |

Each pillar supports the others. A high savings rate gives you more to invest, smart investing grows your capital, tax optimization protects that growth, and a solid withdrawal plan ensures it lasts.

The Shift from Dream to Tangible Goal

For a lot of people, early retirement sounds like a lottery winner's fantasy. But when you reframe it from a vague wish to a concrete financial strategy, it suddenly becomes a real, achievable goal. This requires a huge mental shift in how you see money. Every dollar you save and invest is no longer just a dollar; it's a building block for your future freedom.

Unfortunately, the path to retiring early seems to be getting tougher. Over the last two decades, the number of people who actually plan to retire before 65 has been dropping. A recent Global Retirement Reality Report pointed to an eight percent decline in people aiming for pre-65 retirement, mostly due to worries about inflation and not having enough saved.

This new reality just hammers home why a solid, deliberate plan is more crucial than ever. It's not about getting lucky; it's about making smart, consistent choices.

The core of early retirement planning is simple: engineer a future where your time is truly your own. It's the ultimate trade-off—sacrificing some discretionary spending today for decades of personal freedom tomorrow.

The Real Motivations Behind Retiring Early

So what drives someone to take on such a huge goal? The reasons are always personal and go way deeper than just wanting to leave a job. Figuring out your "why" is the fuel that will keep you going when things get tough.

- More Time for Family: Many early retirees want to be fully present for their kids, help out with aging parents, or just enjoy quality time with a partner without the daily grind getting in the way.

- Pursuing Passions: Ever wanted to start a nonprofit, write a novel, or master woodworking? Early retirement gives you the time and energy to finally dive into the things your career pushed to the back burner.

- Freedom to Travel: For some, the ultimate goal is to see the world without being constrained by a few weeks of vacation time a year. They want to soak in new cultures and build a lifetime of memories.

- Improving Health and Well-being: Ditching a high-stress job can do wonders for your mental and physical health. The aim is to live a longer, healthier, and more fulfilling life.

At the end of the day, planning for an early retirement is about building a bridge to the future you actually want, one smart financial move at a time. It’s about taking control and creating the life you want to live, sooner rather than later.

Calculating Your Financial Independence Number

When you start planning for early retirement, the single most important metric you'll encounter is your Financial Independence (FI) Number. This isn't just some arbitrary savings goal. It’s the specific amount of money you need to have invested so you can live the rest of your life without ever having to work for money again.

Think of it like this: your FI number is the destination you plug into your financial GPS. Without it, you’re just driving aimlessly, hoping you eventually end up somewhere nice. But with a clear target, every financial decision has a purpose—to get you there faster. It turns the fuzzy dream of "retiring early" into a concrete, mathematical objective.

The 25x Expense Rule Explained

So, how do you find this magic number? The most common way is the 25x Expense Rule. It's a brilliantly simple rule of thumb that serves as an excellent starting point for anyone serious about leaving the workforce behind.

The formula is as straightforward as it gets: Your FI Number = Your Annual Expenses x 25.

Let’s say you figure out you can live comfortably on $60,000 a year in retirement. Your FI number would be $1,500,000 (that's $60,000 x 25). If your lifestyle demands $80,000 annually, your target jumps to $2,000,000.

This simple math reveals a powerful truth: the less you spend, the faster you get there. Every single dollar you can trim from your annual budget lowers your target FI number by $25.

How The 4% Rule Fits In

The 25x rule isn't just pulled out of thin air; it’s actually the flip side of another key concept called the 4% Rule. This is a well-known guideline suggesting that you can safely withdraw 4% of your portfolio's value in your first year of retirement, then adjust that amount for inflation each year after, without a high risk of running out of money over a 30-year span.

See how they connect? If your portfolio is $1.5 million, a 4% withdrawal gives you $60,000 for your first year of living expenses. That’s the exact annual expense figure we started with. The two rules work hand-in-hand to give you a target to aim for and a sustainable withdrawal plan once you’ve crossed the finish line.

Your FI Number is not static. It's a living number that will evolve as your life changes. Reviewing it annually helps ensure your early retirement plan stays on track with your real-world needs and goals.

Projecting Your Future Expenses Accurately

The entire calculation hinges on one critical variable: your annual expenses. A wild guess just won't cut it. You need to be both realistic and incredibly thorough. While your current spending is a good baseline, you have to think about how your life will look in retirement.

Start by tracking your spending for at least three to six months. You need a crystal-clear picture of where every dollar is going now. From there, project what your future will look like by considering a few key areas:

- Housing: Will the mortgage be paid off? Are you planning to downsize, or maybe even buy that dream cabin by the lake? Housing is most people's biggest expense, so these decisions are massive.

- Healthcare: This is often the biggest unknown, especially for early retirees. Before you're eligible for Medicare at age 65, you'll be on the hook for private health insurance premiums, deductibles, and other out-of-pocket costs. Don't underestimate this.

- Travel and Hobbies: Let's be honest, early retirement is about having the freedom to do what you love. Be realistic about how much you want to spend on travel, hobbies, and other passions you'll finally have time for.

- Taxes: Your investment withdrawals won't be tax-free. You have to account for federal and state income taxes to avoid a nasty surprise that could throw your entire budget off course.

By digging in and creating a detailed post-retirement budget, you can transform your annual expense estimate from a rough guess into a well-researched figure. That precision is what makes your FI number a target you can truly build a plan around.

Building Your Wealth Generation Engine

To hit your Financial Independence number, you need a seriously powerful financial engine. This engine has two parts that have to work together perfectly: an aggressive savings rate and an intelligent investment strategy.

Think of it like building a race car. Your savings is the high-octane fuel you pour into the tank. Your investments are the engine that turns that fuel into blistering speed. One without the other gets you nowhere fast. A pile of savings sitting in a bank account gets eaten alive by inflation, and a brilliant investment strategy with no cash to invest is just a daydream. Nailing early retirement means mastering both.

The Power of a High Savings Rate

Your savings rate—the percentage of your income you actually keep—is the single biggest lever you can pull to shrink your retirement timeline. You can’t control what the stock market does next year, but you absolutely can control how much you save.

A high savings rate does two things at once. First, it obviously grows your nest egg faster. Second, it trains you to live on less, which means your target retirement number—your "FI Number"—gets smaller. It's a powerful one-two punch.

Consider this: someone saving just 5% of their income might have to grind it out for over 60 years to retire. But crank that up to a 50% savings rate, and they could hit financial independence in as little as 17 years. That's not a small tweak; it's a life-changing difference that shows why the gap between what you earn and what you spend is everything.

The secret to a high savings rate isn't about deprivation; it's about intentionality. It means aligning your spending with your deepest values—and for those pursuing early retirement, freedom is the ultimate value.

Optimizing Your Lifestyle for Maximum Savings

Getting to those high savings rates means going way beyond a simple budget. It's about fundamentally changing how you look at your money, shifting from just tracking expenses to actively engineering them.

- Attack the "Big Three": For most people, housing, transportation, and food are the budget killers. Making changes here isn't just about saving a few bucks; it delivers huge, compounding wins over time. Think about downsizing your home, moving closer to work to ditch a car, or becoming a one-car family.

- Design a Cheaper Lifestyle: Don't just cut things you love—find smarter, cheaper ways to do them. If you love going out to eat, learn to master your favorite restaurant meals at home for a fraction of the cost. If travel is your thing, dive into the world of travel hacking with points and miles.

- Automate Your Savings: Make saving your default setting. The day your paycheck hits, have automatic transfers whisk money away to your investment accounts. This "pay yourself first" strategy is non-negotiable. It ensures your goals are funded before you even have a chance to spend that money.

Structuring Your Investment Accounts

Once you’ve created a nice, wide gap between your income and spending, it's time to put that money to work. How you do it matters. The order you fund your accounts in is incredibly important because of the different tax rules for each.

A smart, methodical approach here is like getting a tailwind from the government. You take advantage of every tax break they offer, which can add up to a massive boost in your long-term returns.

The Waterfall Approach to Investing

Think about filling your investment accounts like a series of cascading waterfalls. You fill the top bucket completely, and only then does the money spill over into the next one down. This ensures you’re squeezing every last drop of tax advantage out of the system.

- 401(k) Up to the Match: This is your first stop, no exceptions. Contribute enough to your company's 401(k) or 403(b) to get the full employer match. This is a 100% guaranteed return on your money. Turning this down is literally throwing away free cash.

- Max Out an IRA: Next up, fully fund an IRA. Whether you choose a Traditional or a Roth IRA depends on if you think you’ll be in a higher tax bracket now or in retirement. A lot of early retirement planners lean toward the Roth IRA because all your withdrawals in retirement are completely tax-free.

- Max Out Your 401(k): Circle back to your 401(k) and keep contributing until you hit the annual IRS maximum. Every dollar you put in here lowers your taxable income for the year, giving you an immediate tax break.

- Health Savings Account (HSA): If your health insurance plan is a high-deductible one, the HSA is a secret weapon. It has a triple tax advantage that's unmatched: your contributions are tax-deductible, the money grows tax-free, and you can withdraw it tax-free for medical expenses.

- Taxable Brokerage Account: After you've maxed out all of the above tax-advantaged accounts, any leftover investment money can flow here. A taxable brokerage account gives you the most flexibility, but it comes with the fewest tax perks.

Following this structured plan is a cornerstone of solid early retirement planning. It makes sure your wealth-generation engine isn't just powerful but also ruthlessly efficient, cutting down your tax bill and letting more of your money work for you.

How to Access Retirement Funds Early with a 72(t) SEPP

You’ve done the hard work, built your wealth engine, and you’re closing in on your financial independence number. But there’s a classic roadblock that trips up many aspiring early retirees: a timing problem. Most of your hard-earned savings are probably locked away in retirement accounts like a 401(k) or traditional IRA, which the IRS slaps with a penalty if you touch them before age 59½.

That presents a serious challenge. How do you actually fund your life in those crucial years between leaving the workforce and reaching the traditional withdrawal age? This is exactly where a specific IRS provision, Rule 72(t), comes into play.

A Substantially Equal Periodic Payments (SEPP) plan, governed by Rule 72(t), is a powerful way to take penalty-free distributions from your retirement accounts before you turn 59½. It’s like having a special key to unlock your own money on your own timeline, without handing 10% of it back to the government in penalties.

What Is a 72(t) SEPP Plan?

Think of a SEPP as a formal agreement you make with the IRS. You agree to withdraw a specific, precisely calculated amount from your retirement account every single year for a set period. In exchange for sticking to that rigid payment schedule, the IRS agrees to waive the usual 10% early withdrawal penalty.

This strategy is built for people who need to create a predictable income stream from their retirement savings to bridge the financial gap until they hit age 59½. But it’s not a decision to take lightly. Once you kick off a SEPP, you are locked into that payment plan for at least five years, or until you turn 59½—whichever is longer.

A 72(t) SEPP is a highly specialized tool, not a flexible line of credit. It demands precision and a long-term commitment, making it essential to understand all the rules before you begin.

The challenge of mapping out a formal retirement plan is surprisingly common. Most workers around the world are operating without a written financial strategy. According to one study, less than 25% of workers in major markets have a formal written retirement plan, which really highlights the need for clear guidance on complex tools like SEPPs.

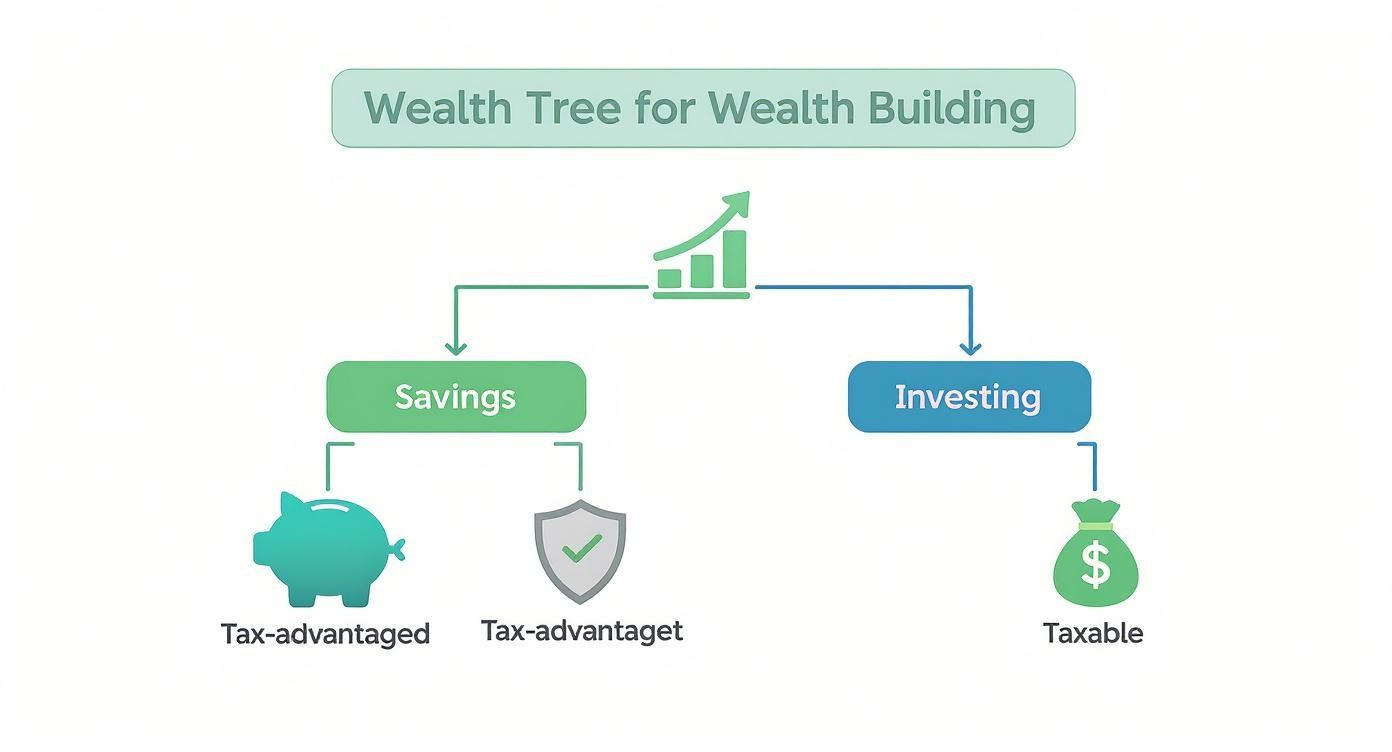

This decision tree visualizes the fundamental choices in building wealth, showing how every path leads to different tax implications.

As the graphic shows, deciding between tax-advantaged and taxable accounts is one of the first critical steps in any effective savings and investment strategy.

The Three IRS Calculation Methods

The IRS gives you three different ways to calculate your annual SEPP distribution amount. Each method uses your account balance, life expectancy, and an interest rate to figure out your payment, but they can produce wildly different results. Choosing the right one comes down entirely to your income needs and overall financial picture.

- Required Minimum Distribution (RMD) Method: This is the most straightforward option. It simply divides your account balance by your life expectancy factor from an IRS table. This calculation gives you the lowest annual payment, which will change each year as your account balance and age change.

- Amortization Method: This method calculates a fixed annual payment by spreading your account balance over your life expectancy, much like a loan. It typically produces a higher payment than the RMD method and is a solid choice if you need a larger, consistent income stream.

- Annuitization Method: Also providing a fixed annual payment, this calculation uses an annuity factor from an IRS table to determine your distribution. The resulting payment amount often falls somewhere between what the RMD and amortization methods would produce.

Getting the nuances of these calculation methods right is absolutely critical. If you want to really get into the nuts and bolts, you can explore how a 72t works in our detailed guide.

The Benefits and Pitfalls of a SEPP

A 72(t) SEPP can be a total game-changer for early retirees, but it's a double-edged sword. The benefits are clear, but the risks of messing it up are severe.

Key Benefits of Using a SEPP

- Penalty-Free Access: The biggest win is avoiding that nasty 10% early withdrawal penalty, which can make early retirement financially possible in the first place.

- Predictable Income: A SEPP provides a steady, reliable stream of income that you can build a budget around during your early retirement years.

- Bridge to 59½: It perfectly serves its purpose as a financial bridge, funding your lifestyle until your other retirement funds become accessible without penalty.

Critical Pitfalls to Avoid

- Extreme Inflexibility: Once a SEPP is up and running, you cannot change the payment amount. If you take too much, too little, or even miss a payment, the plan is considered "busted."

- Severe Penalties for Errors: If you break the SEPP rules, the IRS will retroactively apply the 10% penalty to every single distribution you've ever taken, plus interest. It's a costly mistake.

- Complexity: The rules are notoriously intricate, and a small miscalculation can have disastrous consequences. This is not a DIY project; it almost always requires guidance from a specialist to make sure it's executed flawlessly.

Avoiding Common Early Retirement Pitfalls

The road to early retirement is an exciting one, but it’s easy to hit a pothole if you aren't paying attention. Think of it like a pilot running through a pre-flight checklist; you need to anticipate the common traps that can throw even the best-laid plans off course. Knowing what to watch for is the first step toward building a plan that can handle a little turbulence.

After all, a successful early retirement isn't just about how much you can save. It's about protecting that nest egg and making sure it lasts for what could be a 30, 40, or even 50-year retirement. Let's walk through the biggest risks and how you can steer clear of them.

Underestimating Inflation and Healthcare Costs

One of the sneakiest risks is failing to account for the rising cost of living. It's so easy to anchor your financial plans to today's dollars, but inflation is a silent portfolio killer. It slowly eats away at your purchasing power, meaning the $80,000 you plan to live on each year will buy a whole lot less a decade or two from now.

This problem is even worse when you realize that retiree costs have actually outpaced general inflation. In fact, research shows that from 2000 to 2023, retiree spending climbed at an annual rate of 3.6%, which is quite a bit higher than the 2.6% inflation rate over the same period. You can dig into these trends and what they mean for your savings in a detailed Goldman Sachs retirement survey.

A successful early retirement plan doesn’t just account for inflation; it anticipates it. Building a 2-3% annual inflation adjustment into your expense projections is not conservative—it’s essential.

Healthcare is the other financial giant in the room. Before you turn 65 and Medicare kicks in, you're on your own for health insurance. Private plan premiums can be a serious drain, and one unexpected medical crisis can wipe out years of savings if you're not properly insured.

Ignoring the Sequence of Returns Risk

When it comes to retirement, timing is almost everything. Sequence of returns risk is the danger of hitting a nasty bear market right in the first few years after you stop working. If a downturn strikes just as you start making withdrawals, you’re forced to sell more of your investments at rock-bottom prices. This can permanently cripple your portfolio's ability to bounce back and last your lifetime.

Imagine two people, each retiring with an identical $1 million portfolio. One retires into a roaring bull market and watches their nest egg grow. The other retires right before a major crash. Even if their average long-term returns end up being the same, the second person could run out of money decades sooner simply because of bad luck at the start.

To fight back against this risk, you have a few options:

- Create a Cash Buffer: Keep one to two years of living expenses in cash or something very close to it. This gives you a fund to draw from so you don't have to sell stocks when the market is down.

- Use a Bucket Strategy: Mentally divide your money into different "buckets." Your short-term bucket holds cash for immediate needs, while your long-term bucket stays invested for growth.

- Be Flexible with Withdrawals: This is key. Be prepared to tighten your belt and pull out less money during down years.

The Dangers of an Inflexible Plan

While you absolutely need a detailed plan, one that’s too rigid can shatter under pressure. Life happens. You might face an emergency expense, or maybe your goals and dreams change over time. A plan that’s too restrictive leaves you with no wiggle room to adapt.

This is especially true when you’re using complex strategies like a 72(t) SEPP. It's a fantastic tool for getting to your funds early, but one tiny mistake can trigger massive penalties from the IRS. It’s absolutely vital to understand the common errors people make, because a rigid plan with no backup can be a recipe for disaster. For a closer look, check out our guide on the top 10 things to not do with a Rule 72(t) SEPP. A truly solid plan has flexibility baked right in to handle whatever curveballs life throws your way.

Your Early Retirement Questions Answered

Even with the best strategy laid out, the path to early retirement is filled with specific, real-world questions. The details can sometimes feel like a lot to handle, but finding clear answers is what keeps you moving forward. Let’s dig into some of the most common questions that pop up as you design your own route to financial freedom.

This section gives you direct, no-nonsense answers to help you navigate these big decisions.

Can You Retire Early on an Average Income?

There's a stubborn myth out there that early retirement is a club for high-income earners only. That's just not true. While a bigger paycheck makes it easier to save a lot, what really matters is the gap between what you earn and what you spend.

Think about it: someone earning $60,000 a year who manages to save 40% of their income is on a much faster track than someone earning $150,000 who only saves 10%.

Pulling this off on an average income comes down to a few core principles:

- Intentional Spending: This isn't about being cheap. It’s about spending with purpose. You have to get really good at separating true needs from wants and then being ruthless about cutting costs, especially on the "big three"—housing, transportation, and food.

- Unwavering Consistency: You must commit to investing a serious chunk of your income every single month. No excuses, no breaks. It has to become a non-negotiable habit for years.

- Patience is Your Superpower: Your timeline might be a bit longer than the person with a massive salary, but financial independence is still a mathematical certainty if you just stick with the plan.

Should You Use a Side Hustle to Retire Sooner?

Absolutely. A side hustle is like pouring gasoline on your early retirement fire. It’s one of the most effective ways to speed things up because it attacks the problem from both sides—it raises your income, which lets you pump up your savings rate.

Here's why it works so well: every extra dollar you earn from a side gig can go straight into your investments, since your main job is already covering your day-to-day expenses. This creates a financial fast lane. For example, bringing in an extra $1,000 a month and investing all of it could literally shave years off your retirement date, turning a far-off dream into something you can reach much sooner.

How Do You Get Health Insurance Before Medicare?

This is often the single biggest hurdle for early retirees in the U.S., both financially and logistically. You won't be eligible for Medicare until you're 65, so you need a bulletproof plan to cover that gap. The good news is, you have options, each with its own price tag and perks.

Your main choices for health coverage usually boil down to these:

- ACA Marketplace Plans: The Affordable Care Act (ACA) marketplace is a great place to start. You might even qualify for income-based subsidies that can dramatically lower what you pay each month.

- COBRA: This lets you keep your old employer's health plan for up to 18 months. The catch? You have to pay the full premium yourself, and it can be shockingly expensive.

- Private Plans: You can always buy a plan directly from an insurance company, but these tend to cost more than what you'd find on the marketplace.

- Spouse's Plan: If your spouse is still working, this is often the easiest and most affordable route. Getting on their employer's plan can be a simple solution.

When Should You Consult a Financial Professional?

While you can handle a lot of the initial saving and investing on your own, some situations absolutely call for professional help. Complicated strategies, especially anything involving the IRS, are not the place for DIY guesswork.

"A financial advisor can act as a crucial sounding board and a technical expert, especially when you're navigating complex withdrawal strategies. Their role is to stress-test your plan and ensure a small mistake doesn't lead to a major penalty."

You should strongly consider talking to a specialist when you are:

- Implementing a 72(t) SEPP: The rules are incredibly strict. One tiny mistake can trigger massive penalties. A professional who specializes in SEPPs, like the team at Spivak Financial Group, can make sure the plan is built and managed perfectly.

- Nearing Retirement: An expert can guide you through the transition, help protect you from sequence of returns risk, and build the most tax-efficient withdrawal strategy possible.

- Feeling Overwhelmed: If the complexity is causing you stress and analysis paralysis, getting professional advice can bring clarity and give you the confidence to move forward.

For more detailed answers to these and other questions, our comprehensive FAQ on early retirement topics can provide further insights.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

Navigating the complexities of early retirement, especially when considering a 72(t) SEPP, requires expertise and precision. The team at Spivak Financial Group specializes in crafting these plans to help you access your funds penalty-free and achieve your financial goals sooner. Learn more about how we can help at https://72tprofessor.com.