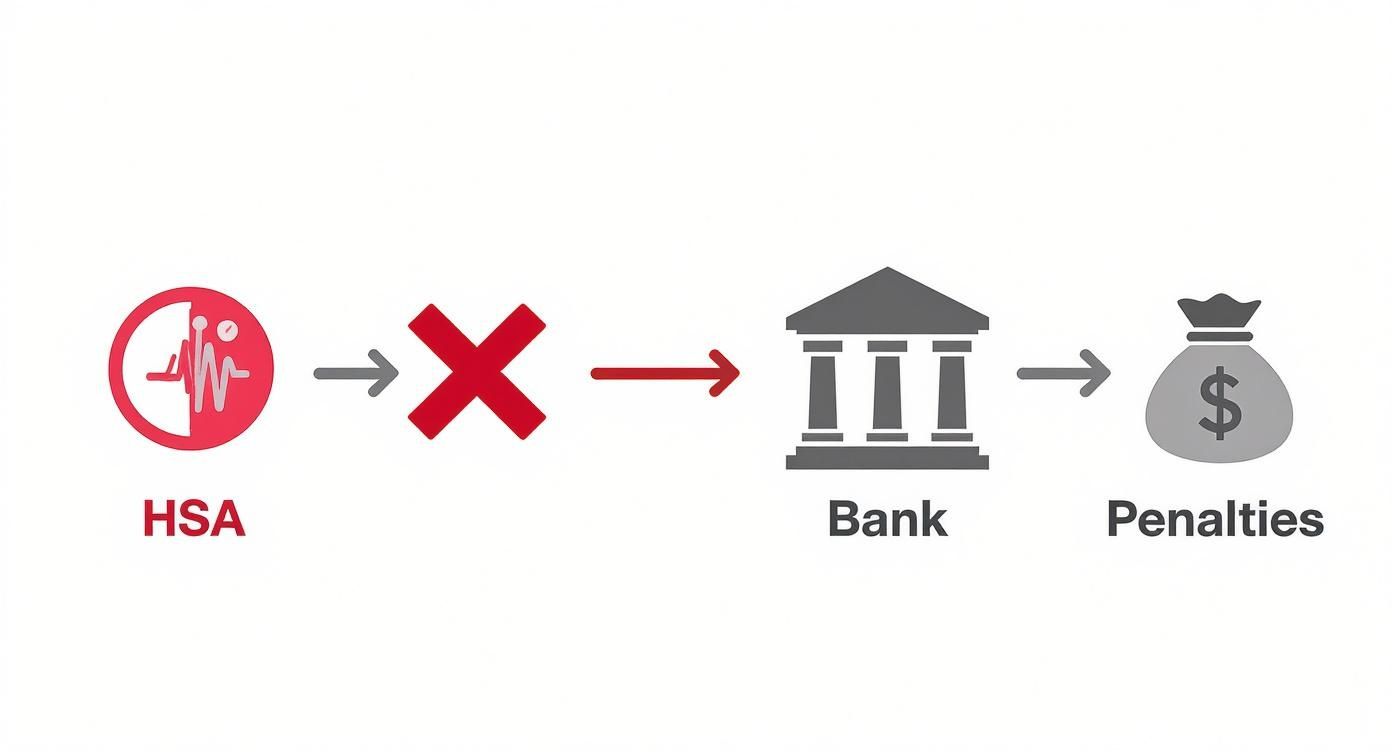

If you've been considering an HSA rollover to an IRA, let's get straight to the point: it's not allowed. U.S. tax law draws a firm line between Health Savings Accounts (HSAs) and Individual Retirement Accounts (IRAs) because they are designed for fundamentally different purposes.

At Spivak Financial Group, we help clients navigate complex financial rules every day. We understand why this question comes up so often, and our goal here is to provide the clear, expert guidance you need.

Why an HSA to IRA Rollover Is Not Allowed

The IRS has structured HSAs and IRAs with distinct purposes, rules, and tax advantages. An HSA is a specialized savings tool for healthcare costs, offering a powerful triple tax benefit: contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

An IRA, on the other hand, is designed purely for retirement savings. Because of these fundamental differences, attempting to move money from an HSA directly into an IRA is treated as a non-qualified distribution.

This is a costly mistake. The entire amount would be subject to ordinary income tax, plus a steep 20% penalty if you're under age 65.

Understanding the Key Differences

The core reason you cannot merge these accounts is their intended use. While both are excellent tools for your long-term financial health, they operate on separate tracks.

- HSA Purpose: To help you save for current and future medical expenses in the most tax-efficient way possible.

- IRA Purpose: To help you build a nest egg for your general retirement needs, with rules designed to encourage long-term, untouched growth until you stop working.

To clarify, let's compare these two accounts side-by-side.

HSA vs Traditional IRA A Quick Comparison

This table highlights why the IRS maintains a strict separation between these funds. Each account has a unique role, and combining them would undermine their specific tax-advantaged structures.

| Feature | Health Savings Account (HSA) | Traditional IRA |

|---|---|---|

| Primary Purpose | Paying for qualified medical expenses | Saving for general retirement expenses |

| Contribution Tax Treatment | Tax-deductible | Tax-deductible |

| Account Growth | Tax-free | Tax-deferred |

| Withdrawal Tax Treatment | Tax-free for qualified medical expenses | Taxed as ordinary income |

| Penalty for Non-Qualified Withdrawal | Income tax + 20% penalty (if under 65) | Income tax + 10% penalty (if under 59½) |

| Required Minimum Distributions (RMDs) | No | Yes, starting at age 73 |

As you can see, the tax treatment, especially for withdrawals, is completely different, which is why the separation is so strict.

The strict separation between these accounts is intentional. It ensures HSA funds are preserved for their primary purpose—covering healthcare costs—rather than being used to supplement general retirement savings outside the established rules.

Essentially, the IRS views these as two distinct pools of money that cannot be combined without triggering taxes and penalties. Under current law, a direct HSA rollover to IRA is prohibited. You can find a deeper dive into the strict definitions of these transactions in our guide on what a rollover is.

Interestingly, the law does permit a special one-time transfer from an IRA to an HSA, but never the other way around. Any attempt to force an HSA into an IRA is simply treated as a taxable distribution—a financial headache you definitely want to avoid.

Exploring the One-Way IRA to HSA Transfer

While the path from an HSA to an IRA is permanently closed, the IRS did create a narrow, one-way street for funds to flow in the opposite direction.

A special, little-known transaction called a Qualified HSA Funding Distribution (QHFD) allows you to move money from your IRA to your HSA. However, this is a highly regulated maneuver you can only perform once in your lifetime. The amount you can move is also capped—it cannot exceed the maximum annual HSA contribution limit for the year of the transfer.

The diagram below emphasizes how strict the rules are about trying to go the other way.

This visual makes it clear: attempting an HSA rollover to an IRA is a prohibited move that leads directly to taxes and penalties. This makes the one-way QHFD the only IRS-approved bridge between these accounts.

The Critical Testing Period Rule

The IRS wants to ensure this transfer is used for its intended purpose: funding an HSA for genuine healthcare needs. To prevent abuse, they enforce a strict “testing period.”

Here’s the rule: after completing a QHFD, you must remain eligible to contribute to an HSA for the following 12 months.

What does this mean in practice?

- You must maintain coverage under a High-Deductible Health Plan (HDHP).

- You cannot have other health coverage that would disqualify you from an HSA.

- You cannot be claimed as a dependent on someone else’s tax return.

If you fail to meet these requirements during that 12-month window, the money you transferred from your IRA becomes taxable income. Even worse, the IRS will add an additional 10% penalty, completely negating any benefit from the transfer.

A QHFD can be a powerful financial move, but it demands careful planning. Think of it as a strategic injection of funds to jump-start a new HSA or quickly meet a large deductible without having to dip into your cash savings.

Why This Transfer Is Uncommon

Despite its utility, the IRA-to-HSA transfer is rare. The vast majority of HSA funding comes from direct contributions made by employers and employees.

Industry research on HSA funding sources shows the average individual HSA contribution was $2,197, while rollovers from IRAs make up a tiny fraction of total deposits. This is largely due to the strict once-in-a-lifetime rule and the annual cap. This makes the QHFD a specialized tool for very specific financial situations, not a go-to funding strategy for most people.

Understanding Penalties for Improper HSA Withdrawals

Thinking about using your Health Savings Account (HSA) for non-medical reasons before age 65? It's a costly mistake.

Since the IRS strictly forbids a direct HSA rollover to IRA, any attempt to move the money this way is treated as a non-qualified withdrawal. The IRS imposes a double-whammy penalty designed to keep those funds reserved for healthcare.

First, any amount you take out for a non-medical expense is added to your taxable income for the year. This can easily push you into a higher tax bracket.

Second, on top of the income tax, the IRS imposes a stiff 20% penalty on the entire withdrawn amount. This is a flat penalty applied regardless of your tax bracket.

A Real-World Penalty Example

Let's illustrate with an example. Imagine you pull $5,000 from your HSA to cover a home repair.

Here’s a breakdown of the cost:

- Initial Withdrawal: $5,000

- Federal Income Tax: If you're in the 22% tax bracket, you’ll owe $1,100 ($5,000 x 0.22).

- IRS Penalty: The extra 20% penalty costs another $1,000 ($5,000 x 0.20).

After paying a combined $2,100 in taxes and penalties, your $5,000 withdrawal has shrunk to just $2,900 in usable cash. You've lost over 40% of your money to avoidable penalties.

This two-part penalty underscores the importance of treating your HSA differently from a standard savings or checking account. The rules are strict to protect its tax-advantaged status for healthcare, and missteps are expensive.

This 20% HSA penalty is significantly harsher than the 10% early withdrawal penalty for IRAs. While there are some 10% early withdrawal penalty exceptions for retirement plans, the rules for HSAs are far more rigid. The takeaway is simple: unless it's for a qualified medical expense, leaving your HSA funds untouched before age 65 is the smartest financial move.

Turning Your HSA Into a Powerful Retirement Account

The discussion around an HSA rollover to IRA often misses the bigger picture. While you cannot merge the accounts, your HSA undergoes an incredible transformation once you turn 65, effectively becoming one of the most flexible retirement accounts available.

The day you turn 65, the dreaded 20% penalty for non-medical withdrawals from your HSA disappears entirely. This is a game-changer.

Your HSA begins to function much like a traditional IRA. You can withdraw money for any reason—a vacation, home renovations, or supplemental income—and you will only owe ordinary income tax, just as you would with a 401(k) withdrawal.

The Best of Both Worlds

This newfound flexibility doesn't eliminate the HSA's primary advantage. Even while functioning like a traditional IRA for general expenses, it retains its unique power for medical costs. Any funds withdrawn for qualified medical expenses remain 100% tax-free, for life.

This dual-purpose nature provides a significant strategic edge in retirement:

- For Healthcare: It remains your go-to, tax-free fund for prescriptions, doctor visits, dental work, and even Medicare premiums.

- For Everything Else: It serves as a backup, tax-deferred retirement account, similar to a 401(k) or traditional IRA, for any other expense.

This unique setup positions the HSA as a core component of a robust retirement plan, offering a dedicated, tax-advantaged source for healthcare while also serving as a supplemental income stream.

By age 65, the HSA matures from a specialized health savings tool into a hybrid retirement account. It offers the tax-free medical benefits it always did, plus the withdrawal flexibility of a traditional IRA, making it unparalleled in its utility.

Maximizing Your HSA for the Long Haul

Despite their growing popularity, many people still view HSAs as short-term accounts for immediate medical bills. While total HSA assets have climbed to over $146 billion, data on how HSA funds are currently being used shows that only a small fraction of account holders are investing their funds for long-term growth.

The inability to perform an HSA rollover to IRA is part of the confusion, but the key is a shift in mindset. Instead of only spending from your HSA, focus on contributing the maximum amount each year and investing the balance. By letting your funds grow tax-free over decades, you build a powerful nest egg that can serve both your health and your wealth in retirement.

Smart Alternatives to an HSA Rollover

Since a direct HSA rollover to IRA is not an option, the focus should shift to smarter, IRS-approved strategies for managing your account. Instead of attempting a prohibited merger, you can use powerful techniques to maximize your HSA’s potential for both healthcare and long-term wealth building.

These methods allow you to improve investment options, reduce fees, and even create a source of tax-free cash in retirement—all within the rules.

Use a Trustee-to-Trustee Transfer

If your current HSA provider has high fees or poor investment choices, you are not stuck. A trustee-to-trustee transfer is the safest and most efficient way to move your HSA funds to a new custodian.

With this method, you never take possession of the money. You open an account with a new provider and complete their transfer paperwork. They then coordinate directly with your old provider to move the funds.

This process has major advantages:

- No Tax Consequences: Because the money moves directly between institutions, the IRS does not consider it a distribution, so it is not a taxable event.

- No Rollover Limits: Unlike the 60-day IRA rollover rule (which is limited to one per year), you can perform as many trustee-to-trustee HSA transfers as you need.

- Better Options: It allows you to find HSA providers with superior investment platforms, lower administrative fees, and better service.

A trustee-to-trustee transfer is like moving money from a mediocre bank to a great one. You aren't withdrawing it to spend; you're simply changing where it's managed to get a better deal, all while keeping its tax-advantaged status intact.

Master the Reimbursement Strategy

One of the most powerful and underutilized HSA strategies is the delayed reimbursement. The IRS does not impose a time limit on when you must reimburse yourself for qualified medical expenses.

This creates a remarkable opportunity:

- Pay Out-of-Pocket: When you incur a medical expense, pay for it with personal funds instead of your HSA.

- Save Your Receipts: Keep meticulous records of every qualified medical expense you paid. This includes digital copies of receipts, bills, and explanations of benefits.

- Let Your HSA Grow: By leaving your HSA untouched, you allow the funds to remain invested, growing completely tax-free for years or even decades.

Then, whenever you need cash in the future—perhaps in retirement or for a major purchase—you can "reimburse" yourself from your HSA for all those accumulated past medical expenses. The withdrawal is 100% tax-free because it’s tied to legitimate expenses, even if they occurred 20 years ago. This effectively turns your HSA into a tax-free emergency fund or a flexible income source.

This strategy requires discipline but offers an incredible payoff. For those looking at unconventional ways to access funds, especially for early retirement, understanding these nuances is critical. You can learn more about accessing retirement funds early to see how different accounts offer unique pathways.

Frequently Asked Questions About HSA and IRA Rules

The rules around HSAs and IRAs can be complex, especially when planning for early retirement. Let's clarify some common questions.

What Happens to My HSA if I No Longer Have an HDHP?

If you switch jobs or your new insurance plan is not a high-deductible health plan (HDHP), you do not lose your HSA.

You simply cannot make new contributions to it. The existing funds remain yours, can stay invested, and continue to grow tax-free. You can also still withdraw money tax-free for any qualified medical expenses. The only change is that the ability to contribute is paused.

Can I Use My HSA to Pay for Family Members?

Yes. This is a powerful feature of an HSA. You can use your funds tax-free to cover qualified medical costs for yourself, your spouse, and any dependents you claim on your taxes.

A key feature of the HSA is its flexibility for family healthcare. Your family members do not need to be covered by your HDHP for you to use your HSA funds on their behalf, making it a versatile tool for managing everyone's medical costs.

Think of it as a family medical fund. It does not matter if your spouse or children are on a different health plan; your HSA can still be used to pay for their legitimate medical needs.

Does an IRA to HSA Rollover Count Toward My Annual Limit?

Yes, it does. The special one-time Qualified HSA Funding Distribution (QHFD) is not extra contribution space. It counts directly against your annual HSA contribution limit for that year.

For example, if the family contribution limit for the year is $8,300 and you execute a one-time rollover of $5,000 from your IRA to your HSA, you are only left with $3,300 of contribution room for that tax year. You have simply pre-funded a large portion of your limit with IRA money instead of cash.

Navigating the complex financial rules for retirement can be challenging, but you don't have to do it alone. At Spivak Financial Group, we specialize in helping people like you create penalty-free income streams from their retirement funds. A 72(t) SEPP plan could provide the consistent income you need to achieve your financial goals. Our office is located at 8753 E. Bell Road, Suite #101, Scottsdale, AZ 85260, and you can reach us at (844) 776-3728. Discover how we can help at 72tprofessor.com.