The big promise of a Roth IRA is beautifully simple: pay your taxes upfront, and when you retire, your withdrawals are 100% tax-free. It sounds perfect, but there's a catch, and its name is qualified.

Knowing what makes a distribution "qualified" is the crucial difference between enjoying that tax-free income and getting a surprise bill from the IRS.

Are Roth IRA Distributions Truly Tax-Free?

The main draw of a Roth IRA is how it flips the traditional retirement model on its head. With a traditional IRA, you get a tax deduction now but pay taxes on every dollar you take out later. The Roth does the exact opposite.

You fund it with after-tax money, which means no tax break today. In exchange for that, your money grows tax-free, and most importantly, your qualified withdrawals won't cost you a dime in federal or state income tax down the road.

This is a game-changer for long-term planning. It allows you to lock in today's tax rates and create a source of retirement income that the government can't touch, as long as you play by the rules.

The Two Sides of Withdrawals

To really get a handle on the taxes on a Roth IRA distribution, you have to understand the line between "qualified" and "non-qualified" distributions. This is the single most important concept.

-

Qualified Distributions: This is the ultimate goal. A qualified distribution is completely tax-free and penalty-free. To get to this point, you have to satisfy two key tests: the 5-year rule and the age 59½ rule, which we'll break down in a bit.

-

Non-Qualified Distributions: Taking money out before you meet those requirements makes the withdrawal non-qualified. This doesn't automatically mean you owe taxes, but it makes things a lot more complicated.

It helps to think of your Roth IRA as having layers of money stacked in a specific order. The IRS has very clear rules about which layer you pull from first. You always take out your direct contributions first, and the great news is that this money can be withdrawn anytime, for any reason, completely tax-free and penalty-free.

This flexibility is a massive perk, but you have to know exactly where your contributions end and your earnings begin. For a deeper dive into choosing the right account for you, our guide on deciding whether to Roth or not to Roth offers some valuable perspective.

The real power of a Roth IRA isn't just the tax-free growth; it's the clarity and predictability it offers for your retirement income. Knowing your distributions won't be taxed gives you a level of financial certainty that is hard to find elsewhere.

To help you get a quick visual, here’s a simple breakdown of how the two distribution types stack up.

Qualified vs Non-Qualified Roth IRA Distributions at a Glance

| Distribution Type | Tax on Contributions | Tax on Earnings | 10% Early Withdrawal Penalty |

|---|---|---|---|

| Qualified | Never taxed | Never taxed | Never applied |

| Non-Qualified | Never taxed | Taxable | May apply to earnings portion |

As you can see, hitting "qualified" status is where the magic happens. Your contributions are always yours to take back, but protecting the earnings from taxes and penalties requires careful planning.

This guide will walk you through all the essential rules—from the 5-year clock to penalty exceptions—giving you a practical roadmap for managing your Roth IRA and unlocking its full tax-free potential.

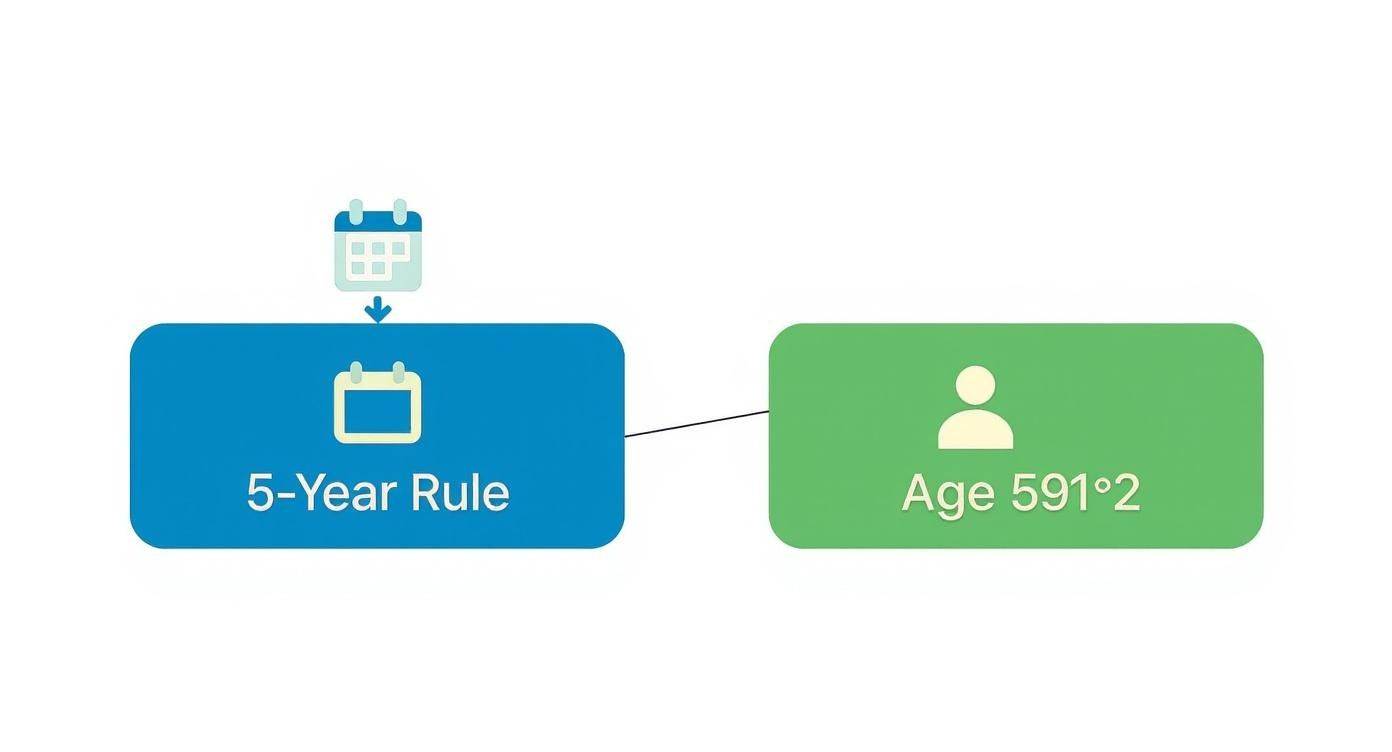

The Two Keys to Unlocking Tax-Free Earnings

To get your Roth IRA's investment growth out completely tax-free, you have to satisfy two big IRS requirements. Think of it like a safe deposit box that needs two separate keys to open; you absolutely need both to get to your tax-free earnings. One key is about time, and the other is about age.

Getting these two rules down is the bedrock for understanding how taxes on a Roth IRA distribution work. If you miss either one, any earnings you pull out could get hit with both income tax and a nasty penalty. Let's break down exactly what you need to do.

The 5-Year Rule Explained

The first key is the 5-year rule. This is a one-time waiting period that every single Roth IRA owner has to get through. The rule is simple: five full years have to pass before you're allowed to withdraw any of your investment earnings tax-free.

The good news is that the IRS is pretty generous with how this clock starts. It begins on January 1st of the tax year you made your very first contribution to any Roth IRA. This is a huge point—it doesn't matter if you opened the account and funded it in April or even on New Year's Eve. Your 5-year clock gets backdated to the beginning of that year.

Once you’ve satisfied this 5-year period, it’s done. Forever. You never have to think about this specific 5-year rule for your contributions again, even if you open more Roth IRAs down the road.

People often get tripped up here, thinking that every new contribution restarts the clock. That's not how it works for your regular annual contributions. The single 5-year holding period that started with your first Roth IRA covers all the contributions you make after that, to that account or any other Roth IRA you own.

Let’s walk through a quick example to see it in action.

Timeline Example

- April 10, 2024: Sarah, who is 50, opens her first Roth IRA and puts in $7,000 for the 2024 tax year.

- January 1, 2024: Even though she didn't contribute until April, her 5-year clock officially started ticking on this date.

- January 1, 2029: Sarah’s 5-year waiting period is now officially over.

From this day on, Sarah has permanently checked one of the two boxes required to access her earnings tax-free.

The Age 59½ Rule

The second key is much simpler: you must be at least age 59½ to take out your earnings without getting dinged. This is a standard rule you'll see across most retirement accounts, and it's there to make sure people are actually saving for, well, retirement.

Unlike the 5-year rule, which you can satisfy fairly early on, the age requirement is a hard-and-fast milestone. Until you hit that birthday, the IRS generally considers any withdrawal of investment earnings to be "early."

It's critical to see how these two rules have to work together.

- Met the 5-year rule but you're not 59½? Your earnings are likely taxable and penalized.

- You're over 59½ but haven't met the 5-year rule? Your earnings are still taxable.

You have to satisfy both conditions at the same time for your withdrawal to be what the IRS calls a "qualified," tax-free distribution. For Sarah in our example, her 5-year clock ends in 2029 when she's 55. But she still has to wait until she turns 59½ to take a qualified, tax-free distribution of her earnings. Understanding this interplay is central to managing the taxes on a Roth IRA distribution. We'll get into some important exceptions to the age rule later, but for now, just know this is the core principle.

How the IRS Sees Your Roth IRA Withdrawal

Not all money inside your Roth IRA is treated the same. To really understand the taxes on a Roth IRA distribution, you have to see your account through the eyes of the IRS. Luckily, the agency has a specific, three-tier ordering rule that dictates which funds come out first—and it’s incredibly favorable for account holders.

Imagine your Roth IRA is like a bucket filled with three distinct layers of water. The IRS says you must always drain the top layer first before you can get to the one below it. This simple structure is the key to strategically accessing your money when you need it.

Your Contributions Come Out First

The top and most accessible layer in your Roth IRA bucket is your direct contributions. This is all the after-tax money you’ve personally put into the account over the years.

Here's the best part: You can withdraw 100% of your direct contributions at any time, for any reason, without paying a dime in taxes or penalties. It doesn’t matter if you’re 35 or 65, or whether you’ve had the account for one year or twenty. The IRS sees this as a simple return of your own money, so it’s always yours, free and clear.

This feature makes a Roth IRA a surprisingly flexible savings vehicle. Need cash for an emergency? Your contributions can be pulled out without the steep penalties common in other retirement accounts. Just be sure to keep excellent records of your contributions. Your financial institution sends you Form 5498 each year, which is a great tool for tracking this.

Next in Line Are Converted Funds

Only after you have withdrawn every single dollar of your direct contributions do you dip into the second layer of the bucket: converted funds. This tier consists of money you rolled over from a pre-tax account, like a Traditional IRA or an old 401(k), into your Roth IRA.

When you perform a Roth conversion, you pay income tax on that money upfront. Because those taxes have been paid, the converted principal (the original amount you converted) can also be withdrawn tax-free.

However, there's a catch. A 10% penalty might apply if you're not careful. Each conversion has its own separate 5-year clock that you must satisfy to avoid this penalty. This is a crucial detail that often trips people up, and we'll dig into it more later. For now, just know that conversions are the second type of money you access.

Last to Be Touched Are Your Earnings

The final layer, at the very bottom of the bucket, is your investment earnings. This is all the growth—the interest, dividends, and capital gains your money has generated inside the account. This is the only part of your Roth IRA that is potentially subject to both taxes and penalties.

You only touch this layer after you've exhausted all your contributions and all your converted funds. For your earnings to be completely tax-free and penalty-free, the withdrawal must be "qualified," which means you've met both the 5-year rule and the age 59½ requirement.

The IRS withdrawal order is a massive built-in benefit. It lets you access a significant chunk of your account (all contributions and converted principal) tax-free long before you might meet the official requirements for a "qualified" distribution.

This flowchart gives you a simple visual guide for determining if your withdrawal of earnings will be tax-free.

As the decision tree shows, satisfying both the 5-year holding period and reaching age 59½ are the two keys to unlocking completely tax-free earnings.

How It All Comes Together

Let’s put this ordering rule into a practical example to see how it plays out in the real world.

Here's a breakdown of how the IRS sources a non-qualified distribution and what the tax impact is at each level.

Roth IRA Withdrawal Ordering Rules and Tax Impact

| Withdrawal Tier | Source of Funds | Taxable Status | 10% Penalty Status |

|---|---|---|---|

| Tier 1 | Direct Contributions | Tax-Free | Penalty-Free |

| Tier 2 | Converted Principal | Tax-Free | Potentially Penalized (if within 5 years of conversion) |

| Tier 3 | Investment Earnings | Taxable | Penalized |

This tiered system ensures you always access your most favorable money first, pushing off any potential taxes or penalties on earnings until the very end.

Let's look at a scenario:

- Who: Alex is 45 years old and has a Roth IRA.

- What's Inside: He contributed $30,000 over the years. He also converted $20,000 from a Traditional IRA three years ago. His account has grown and now has $10,000 in earnings. The total account value is $60,000.

- The Need: Alex needs $35,000 for a major expense.

Here’s how the IRS treats his withdrawal, piece by piece:

- The first $30,000 is considered a return of his contributions. This portion is 100% tax-free and penalty-free.

- The next $5,000 comes from his converted funds. This is also tax-free because he paid taxes at the time of conversion. However, because he is under 59½ and the conversion happened less than five years ago, this $5,000 is hit with the 10% early withdrawal penalty.

- His $10,000 in earnings remains completely untouched and continues to grow.

When you take any distribution, your financial institution will issue a Form 1099-R. For a detailed breakdown of this crucial document, you can learn more about how to read your Form 1099-R and report your distribution correctly. Getting this right is essential for ensuring you file your taxes accurately and avoid headaches with the IRS.

Navigating Early Withdrawals and Penalty Exceptions

Life doesn't always go according to plan. While the goal is to keep your retirement money tucked away until you hit age 59½, sometimes things come up that force you to tap into it sooner. The good news is, the IRS understands this. While they typically slap a 10% early withdrawal penalty on earnings you take out too soon, they’ve built in several key exceptions for when life throws you a curveball.

Knowing these exceptions is absolutely critical if you're facing a non-qualified distribution. They can let you access the earnings portion of your Roth IRA—the part that's normally taxable and penalized if withdrawn early—without that extra 10% sting. Just remember, these exceptions only get you out of the penalty. You'll still owe income tax on any earnings you withdraw if you haven't yet met the 5-year rule.

Common Penalty Waivers You Should Know

The IRS provides a handful of penalty waivers for specific, major life events. Each one has its own set of strict rules you have to follow to the letter. Getting the details right can save you a ton of money.

Here are a few of the most common exceptions people use:

- First-Time Home Purchase: You can pull out up to a $10,000 lifetime maximum from your Roth IRA earnings, penalty-free, to buy, build, or rebuild a first home. This can be for you, your spouse, your kids, or even your grandkids.

- Qualified Higher Education Expenses: Need to pay for college? You can use Roth earnings penalty-free to cover tuition, fees, books, and supplies at an eligible school for yourself, a spouse, children, or grandchildren.

- Significant Medical Expenses: If you're hit with big medical bills, you can take penalty-free withdrawals to cover unreimbursed expenses that are more than 7.5% of your adjusted gross income (AGI).

- Disability: Should you become totally and permanently disabled, you can access your Roth IRA earnings without the 10% penalty. The IRS has a very specific definition of what counts as a qualifying disability, so be sure to check the fine print.

It's worth repeating: these exceptions only waive the 10% penalty. If you take out earnings before your account is five years old, you'll still have to pay regular income tax on that money, even if one of these situations applies to you.

Figuring out the specifics of each waiver can be a headache. For a deeper dive into all the available options, check out our complete guide on the 10 early withdrawal penalty exceptions to see if your situation qualifies.

An Advanced Strategy for Early Income Needs

But what if you don't just have a single, one-time expense? What if you need a steady, reliable stream of income before you reach retirement age? For that scenario, the IRS offers a more structured—but incredibly powerful—option called a Substantially Equal Periodic Payment (SEPP) plan, which you'll often hear referred to as a 72(t) distribution.

A SEPP plan lets you take a series of scheduled withdrawals from your retirement account for at least five years or until you turn 59½, whichever is longer, without that pesky 10% penalty. The withdrawal amounts are calculated using one of three specific, IRS-approved methods that factor in your account balance and life expectancy.

This isn't just a simple withdrawal, though; it's a formal plan that demands absolute precision. Once you start a SEPP, you are locked into that payment schedule. If you deviate from it in any way, the IRS can retroactively disqualify the entire plan, and you'll owe all the penalties and interest you were trying to avoid. Because it's so complex, it's a tool best used with professional guidance.

The rules around early withdrawals and SEPP plans are genuinely intricate. One wrong move can lead to a surprise tax bill and penalties, completely defeating the purpose of using an exception in the first place. This is where working with a specialist who lives and breathes these nuances, like the team at Spivak Financial Group, becomes essential. We can help you analyze your unique situation, figure out if a penalty exception or a full-blown SEPP plan is the right move, and make sure you follow every rule correctly to get your money without any costly mistakes.

Understanding the 5-Year Rule for Roth Conversions

When you move money from a Traditional IRA into a Roth IRA, it’s called a conversion. This is a popular strategy that lets you pay taxes on the money now so you can enjoy completely tax-free withdrawals down the road. But there’s a catch: this move comes with a unique and often misunderstood waiting period.

Each time you complete a Roth conversion, you start a brand-new, separate 5-year clock for that specific chunk of money. This rule exists to prevent folks from using a conversion as a quick backdoor to get retirement funds out without facing a penalty.

A very common mistake is thinking the original 5-year rule—the one that started with your very first contribution—covers everything in the account. It doesn't. To avoid a surprise 10% penalty, you have to track each conversion amount and its unique 5-year timeline.

How Multiple Clocks Work

It helps to think of your Roth IRA as a big container holding different buckets of money. One bucket has all your regular contributions. Every time you do a conversion, you create a new, separate bucket. Each of these conversion buckets gets its own timer, which officially starts on January 1st of the year you made the conversion.

Now, this rule doesn't have anything to do with the taxability of the converted principal itself; you already paid income tax on that money when you converted it. Instead, this clock is all about whether you’ll get hit with a 10% penalty if you withdraw that specific converted amount before its 5-year timer is up and before you’re 59½.

The key takeaway is simple but crucial: every Roth conversion has its own 5-year holding period for penalty purposes. This applies to each conversion, creating multiple timelines you must manage if you convert funds over several years.

Getting this detail right is critical for managing the taxes on a Roth IRA distribution and making sure your financial strategy pays off as expected.

A Practical Example of Conversion Timelines

Let's walk through an example to see how this plays out in the real world. Meet David, who is 50 years old and has had a Roth IRA for a while.

-

Conversion 1 (2022): David converts $20,000 from his Traditional IRA. The 5-year clock for this specific pot of money starts ticking on January 1, 2022, and will end on January 1, 2027.

-

Conversion 2 (2024): He decides to convert another $30,000. This starts a completely new 5-year clock for this amount, beginning on January 1, 2024, and ending on January 1, 2029.

Fast forward to 2026. David is now 54 and needs to withdraw $25,000. Let’s assume he’s already taken out all of his regular contributions. The IRS ordering rules dictate that converted funds come out on a first-in, first-out basis.

- The first $20,000 of his withdrawal comes from the 2022 conversion. Since more than five years have passed since January 1, 2022, this portion comes out completely penalty-free.

- The next $5,000 needed must come from the 2024 conversion. Because this withdrawal is happening inside the 5-year window for that specific conversion, this $5,000 is hit with the 10% penalty.

This scenario highlights why keeping meticulous records is an absolute must. Strategic conversions are often made based on what you think future tax rates will be. In fact, research analyzing 2019 tax law found that under those rates, nearly half of savers would have ended up with more retirement wealth in Roth accounts than traditional ones. You can read more about the findings on retirement tax shields. Mastering these conversion rules is how you ensure you can capture those benefits without getting tripped up by accidental penalties.

Your Roth IRA Distribution Questions Answered

We’ve covered the core mechanics of Roth IRA distributions—the 5-year clocks, the penalty exceptions, and all that good stuff. But let's be honest, the real questions pop up when you try to apply those rules to your own life.

This section is all about tackling those practical, "what if" scenarios. We'll clear up some of the most common questions we hear to give you the confidence you need to handle the taxes on a Roth IRA distribution like a pro.

Do I Have to Report a Tax-Free Roth IRA Distribution on My Tax Return?

Yes, you absolutely do. Even if your withdrawal is 100% tax-free, you still have to tell the IRS about it.

Here’s how it works: When you take money out, your financial institution sends you a Form 1099-R. Think of this as the starting gun. You’ll then need to file Form 8606 with your tax return. This is your chance to officially show the IRS that your withdrawal was qualified and not taxable income. It's also how you and the IRS stay on the same page about your contribution basis.

Don't skip this step. If you do, the IRS might just assume your withdrawal is taxable and send you a notice you really don’t want to see.

What Happens If I Inherit a Roth IRA?

Inheriting a Roth IRA is one of the more favorable scenarios for a beneficiary. As long as the original owner had already satisfied their 5-year holding period, any distributions you take are generally tax-free.

Here’s another big plus: as the beneficiary, you are not subject to the 10% early withdrawal penalty, no matter how old you are.

But there's a catch. Thanks to the SECURE Act, most non-spouse beneficiaries can't just let the money grow tax-free forever. You're now required to withdraw all the funds from the account within 10 years of the original owner's death. It's a limited window, but every dollar you pull out during that time remains completely tax-free.

Can I Put Money Back into My Roth IRA After Taking It Out?

Usually, a withdrawal is a one-way street. Once the money is out, it's out for good. But the IRS offers one critical escape hatch that can act like a short-term, interest-free loan from yourself: the 60-day rollover rule.

This rule lets you take money out of your Roth IRA and avoid all taxes and penalties, but only if you put the full amount back into a Roth IRA within 60 calendar days. Miss that deadline, even by a day, and the withdrawal becomes a standard distribution, subject to all the usual tax and penalty rules. Just be aware, you can only use this little trick once every 12 months.

Keeping meticulous records is the foundation of smart Roth IRA management. Your records are your proof to the IRS, ensuring you never pay taxes on money that should be yours, free and clear.

Good documentation is what proves your contribution basis and helps you track your 5-year clocks. It’s your best defense against unnecessary taxes and penalties.

How Do I Keep Track of My Roth IRA Contributions?

This is one of the most important habits you can build as a Roth IRA owner, especially if you think you might ever need to tap your funds early. Your contributions are your get-out-of-jail-free card—the money you can always pull out tax and penalty-free.

Your financial institution helps by sending you Form 5498 each year, which is the official record of your IRA contributions for the previous tax year. My advice? Save every single one of them. Many people also track their contributions in a simple spreadsheet for a quick, at-a-glance total. These records are your ultimate proof to the IRS of just how much of your account is tax-free principal.

The popularity of IRAs has exploded over the years. Back in 1998, over three-quarters of the eligible population had access to a deductible or Roth IRA. Fast forward to 2019, and data showed that about 25% of all U.S. households owned some type of IRA, proving just how vital these accounts have become for American savers.

Getting a handle on these details is what unlocks the true power of your Roth IRA.

At Spivak Financial Group, we specialize in helping individuals access their retirement funds early and strategically, ensuring every withdrawal is structured to minimize taxes and avoid costly penalties. If you're considering a SEPP plan or need guidance on complex distribution rules, visit us at https://72tprofessor.com or call (844) 776-3728 to learn how we can help you achieve your financial goals.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260