Thinking about converting a traditional IRA to a Roth IRA? This is a popular strategy that involves moving your pre-tax retirement funds into a post-tax account. You'll take an immediate tax hit on the amount you convert, but in return, you get the promise of tax-free withdrawals down the road. It’s a powerful move that lets your investments grow completely tax-free and frees you from required minimum distributions (RMDs) once you retire.

Why a Roth IRA Conversion Is a Powerful Retirement Tool

Deciding whether to convert your traditional IRA is a major fork in the road for your long-term financial plan. It's a calculated trade-off: you're choosing to pay income taxes on the converted amount now to lock in significant tax advantages later on. This isn't just shuffling paperwork; it's a strategic play based on where you are financially today and where you expect to be in the future.

The real magic is in turning tax-deferred savings into a source of completely tax-free income. With a traditional IRA, you get a tax deduction when you contribute, but every single dollar you take out in retirement gets taxed as ordinary income. A Roth IRA completely flips that script.

Key Benefits of a Roth Conversion

At its core, the Roth conversion offers three game-changing advantages that can completely reshape how you approach retirement.

- Tax-Free Growth and Withdrawals: This is the big one. Once the money is sitting in your Roth IRA, all future growth and qualified withdrawals are 100% tax-free. No questions asked.

- No Required Minimum Distributions (RMDs): Traditional IRAs make you start taking taxable withdrawals at age 73. With a Roth IRA, the original owner never has to take a distribution. Your money can keep growing, untouched and tax-free, for your entire life if you want.

- Powerful Estate Planning Tool: When you pass on your Roth IRA, your heirs can inherit it and enjoy those same tax-free withdrawals. It’s an incredible way to transfer wealth without saddling your loved ones with a huge tax bill.

A Roth IRA conversion is more than just moving money between accounts. It's an investment in tax certainty for your future, giving you control over when you pay your taxes—now, rather than later when rates may be higher.

This strategy is all about building tax diversification. Just like you wouldn't put all your money into a single stock, you shouldn't have all your retirement savings in a single type of tax-advantaged account.

Having a Roth IRA gives you a bucket of tax-free money you can draw from in retirement. This flexibility can be a lifesaver, helping you manage your taxable income and potentially keeping you in a lower tax bracket. Navigating these choices can be complex, and the team at Spivak Financial Group is here to help you build a strategy that fits your unique situation.

To put it all in perspective, here’s a quick rundown of how a Traditional IRA stacks up against a Roth IRA after a conversion.

Roth Conversion At-a-Glance Decision Matrix

| Feature | Traditional IRA | Roth IRA (Post-Conversion) |

|---|---|---|

| Contributions | Pre-tax dollars (often tax-deductible) | N/A (Funded by converting pre-tax money) |

| Tax on Growth | Tax-deferred | Tax-free |

| Withdrawals in Retirement | Taxed as ordinary income | Completely tax-free (qualified) |

| Required Minimum Distributions (RMDs) | Yes, starting at age 73 | No, not for the original owner |

| Benefit for Heirs | Inherited funds are taxable upon withdrawal | Inherited funds are tax-free upon withdrawal |

This table makes the trade-off crystal clear. You're prepaying the taxes with a conversion, but in exchange, you're buying a future of tax-free income, more flexibility, and a cleaner estate transfer for your family.

Navigating the Tax Implications of a Roth Conversion

When you decide to convert a traditional IRA to a Roth IRA, the biggest piece of the puzzle is the tax bill. This isn't some surprise fee—it's a deliberate move where you're choosing to prepay your taxes to secure a lifetime of tax-free growth and withdrawals. When you reframe it this way, what might seem like a scary tax event becomes one of the most powerful strategic tools in your financial arsenal.

The basic idea is simple: every dollar you convert gets added to your taxable income for that year. If you move $50,000 from your traditional IRA to a Roth, the IRS sees that $50,000 as ordinary income, plain and simple. It's treated just like your salary. This is exactly why a bit of foresight and careful planning is so critical.

Understanding the Bracket-Filling Strategy

One of the smartest ways to manage the conversion tax is a technique known as “bracket-filling.” The goal here is to convert just enough from your traditional IRA to fill up your current marginal tax bracket, but not so much that you push yourself into a higher one. It’s a way to pay taxes at a rate you’re already in, rather than accidentally triggering a much bigger tax hit.

Think of your tax bracket as a bucket. If you have some room left before it overflows into the next, more expensive bucket, you can fill that empty space with converted funds.

Let's say you're a single filer with a taxable income of $70,000. For 2024, the 22% tax bracket for single filers goes all the way up to $100,525. That means you have $30,525 of "room" ($100,525 – $70,000) before your next dollar gets taxed at the higher 24% rate. You could strategically convert exactly $30,525, knowing the entire amount is taxed at your current 22% rate.

This tax-planning approach is especially timely. With current tax rates set to expire, we have a clear roadmap for the next couple of years. Someone with $150,000 in taxable income could convert another $56,700 to top out their 22% bracket, effectively locking in today’s rates on that chunk of their retirement savings before they potentially go up. For more on this, check out the tactical opportunities discussed at Echelon Financial.

Pay Conversion Taxes with Outside Funds

Here’s a non-negotiable piece of advice we give at Spivak Financial Group: always pay the conversion tax with money from a non-retirement account. Use cash from a checking, savings, or brokerage account. It can be tempting to just have the taxes withheld directly from the conversion amount, but this is a costly mistake for a couple of reasons.

- You Shrink Your Roth Balance: The money withheld for taxes never even makes it into your Roth IRA. That means it loses out on decades of potential tax-free growth.

- You Might Get Hit With Penalties: If you're under age 59½, the IRS treats the withheld tax amount as an early distribution. That means you could get slapped with a 10% early withdrawal penalty on top of the income tax you already owe.

By paying the tax bill with outside funds, you ensure every last dollar of your conversion gets into the Roth IRA to start working for you, tax-free. This is how you maximize the long-term power of the strategy.

The Impact of Nondeductible Contributions

Now, the tax math can get a little trickier if you've made nondeductible (after-tax) contributions to your traditional IRAs over the years. This after-tax money is what’s known as your IRA basis. Since you already paid taxes on this money once, the IRS doesn't make you pay taxes on it again during a conversion. You can learn more about how to calculate your IRA basis in our detailed guide, which is a must-read before starting this process.

The IRS uses the pro-rata rule to figure out how much of your conversion is taxable. Essentially, it views all of your traditional, SEP, and SIMPLE IRAs as one big account. The rule calculates the percentage of your total IRA balance that is after-tax money versus pre-tax money. That same percentage is then applied to whatever amount you convert, which determines the nontaxable portion. This prevents people from cherry-picking only their after-tax dollars to convert.

Don't Forget State Tax Implications

Finally, remember that the IRS isn't the only one interested in your conversion. Most states have their own income tax, and they'll want their cut, too. The income you recognize from a Roth conversion will almost certainly be taxable at the state level, adding to your total tax bill for the year.

This is where location can make a huge difference. A few states have no income tax at all, which can make them very attractive for executing large conversions. If you're planning a move to a state like Florida, Texas, or Nevada, timing your conversion until after you've officially established residency could lead to massive tax savings. Always factor your state's specific tax code into your strategy.

The Mechanics of Executing Your IRA Conversion

Once you've made the decision to convert a traditional IRA to a Roth, the next part is simply execution. It’s less about financial wizardry and more about following a clear, methodical path.

The journey starts with a simple conversation with your brokerage firm. You'll want to get a handle on their specific procedures and what paperwork they require.

Choosing Your Conversion Method

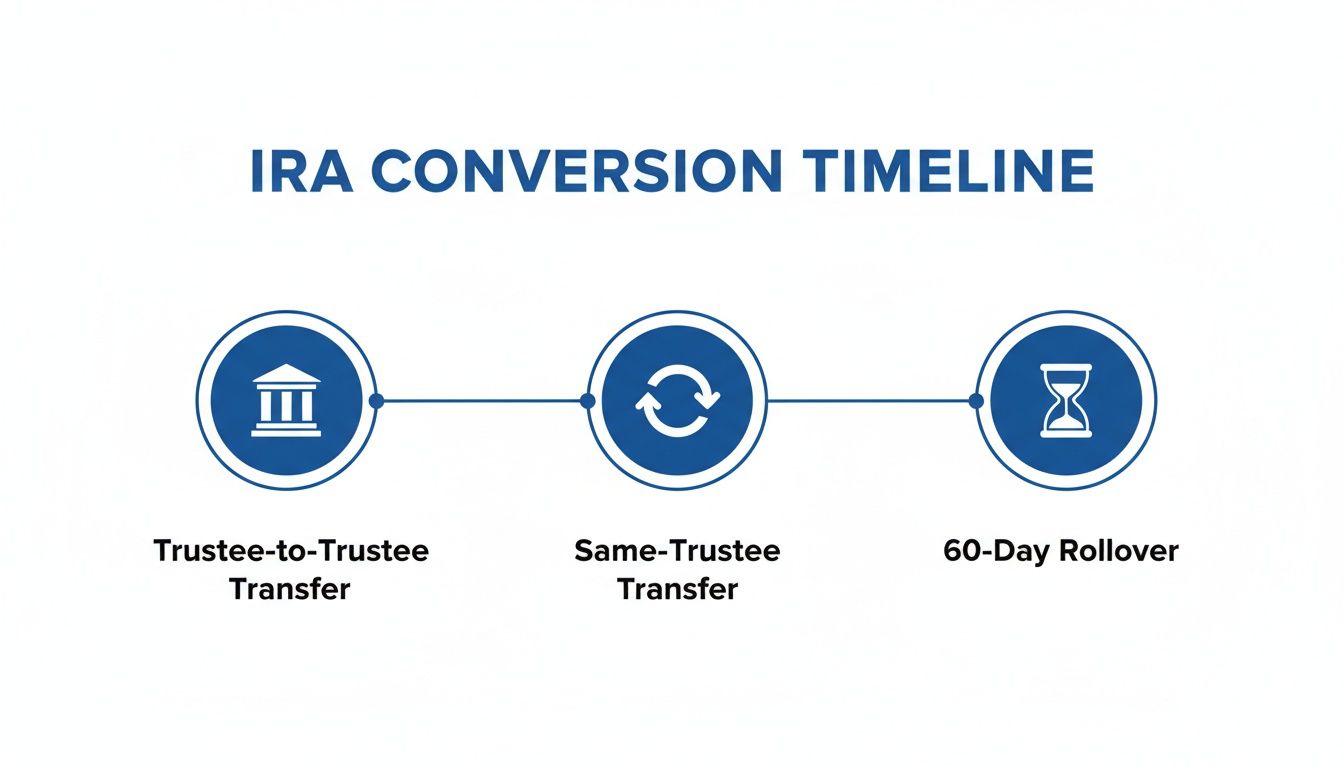

While every firm has its own nuances, the conversion itself generally happens in one of three ways. Knowing the difference is key to choosing the safest and most efficient route for your money.

How you move the funds from your traditional IRA to your new Roth IRA matters—a lot. While you have options, direct transfers are almost always the right call to sidestep potential tax headaches.

- Trustee-to-Trustee Transfer: This is the gold standard and the method we almost always recommend. Your current IRA custodian sends the funds directly to the custodian of your new Roth IRA. The money never touches your personal bank account, which keeps things clean and eliminates the risk of missing a crucial deadline.

- Same-Trustee Transfer: This is even simpler. If you’re keeping your accounts at the same financial institution (like Fidelity or Vanguard), you’re essentially just re-labeling the account from traditional to Roth within their system. It's clean, fast, and about as foolproof as it gets.

- 60-Day Rollover: This method is the riskiest and, frankly, one you should probably avoid. Your custodian cuts you a check, and you have 60 days to get that money into a Roth IRA. If you miss that deadline for any reason, the IRS treats the whole amount as a taxable distribution. To make matters worse, if you're under 59½, they’ll likely hit you with a 10% early withdrawal penalty.

The safest path is always a direct transfer, either between trustees or within the same one. It removes the risk of human error that comes with the 60-day rollover and ensures a smooth, compliant conversion.

Demystifying the Paperwork and Reporting

Getting the money moved is a big step, but your job isn’t quite done. You must report the conversion to the IRS on your tax return for the year it happened.

This is where a crucial piece of paperwork comes into play: IRS Form 8606, Nondeductible IRAs. This form is how you officially tell the IRS about the conversion. It’s also where you track your IRA "basis"—that is, any after-tax money you may have contributed to your traditional IRAs over the years. Filling this out correctly ensures you don't get taxed twice on the same dollars.

Your brokerage will also send you a Form 1099-R showing the gross distribution from your traditional IRA. Don't panic if this form labels the entire amount as taxable. Form 8606 is where you get to clarify the actual taxable portion after accounting for any nondeductible contributions you've made.

Handling the Pro-Rata Rule

Here's where things can get tricky. If you have any pre-tax funds in any of your traditional, SEP, or SIMPLE IRAs, you're going to run into the pro-rata rule.

The IRS looks at all of your non-Roth IRAs, adds them all up, and treats them as one giant account for tax purposes. This means you can't just cherry-pick your after-tax contributions to convert.

Let's walk through an example. Say you have $90,000 in pre-tax IRA funds and $10,000 in after-tax (nondeductible) funds scattered across your accounts. Your total IRA balance is $100,000, and 10% of it is after-tax money.

If you decide to convert $20,000 that year, the pro-rata rule kicks in. It dictates that only 10% of that conversion ($2,000) is tax-free. The other 90% ($18,000) is fully taxable income.

This rule can be a major roadblock. One potential workaround, for those with a current 401(k) plan that accepts incoming rollovers, is to move your pre-tax IRA funds into that 401(k). This could effectively isolate your after-tax basis in the IRA, making a subsequent Roth conversion fully tax-free. We dig into similar strategies in our guide on the 401(k) rollover to IRA process. This is a sophisticated maneuver that requires careful planning, and consulting with a professional at Spivak Financial Group can ensure you navigate these rules correctly.

The Roth Conversion Ladder for Early Retirement

For anyone dreaming of retiring well before the traditional age, one of the biggest roadblocks is getting to your retirement money without getting hammered by penalties. The IRS hits you with a 10% penalty on most traditional IRA withdrawals before you turn 59½. This is exactly where a powerful strategy called the Roth Conversion Ladder comes into play.

This isn't just a clever trick; it's a foundational strategy for many in the early retirement community. It’s a methodical way to build a pipeline of tax-free and penalty-free income years before you're "supposed to" retire.

Building Your Ladder Rung by Rung

The concept itself is surprisingly straightforward. A Roth Conversion Ladder is just a series of planned, annual conversions from your traditional IRA over to a Roth IRA. You intentionally move a chunk of money each year—enough to cover one year's living expenses in retirement—and pay the income tax on that conversion upfront.

Each of these yearly conversions creates a "rung" on your ladder. The magic is in the IRS's five-year rule. For every dollar you convert, a five-year clock starts ticking. Once that five years is up, you can pull out the principal (the original amount you converted) without any penalty, even if you're under 59½.

Think of it like aging a fine wine. Each year, you set aside a new batch of funds to "season" for five years. After the first batch has matured, it's ready to drink. The next year, the second batch is ready, creating a continuous flow of accessible cash.

As you can imagine, this takes some serious planning. You essentially have to start building your income stream at least five years before you actually need it.

This infographic lays out the mechanics of getting the money from point A to point B. For building a ladder, direct transfers are by far the safest option.

You can see why the trustee-to-trustee or same-trustee transfers are preferred. They are direct and remove the risk of human error that comes with a 60-day rollover, where a missed deadline can trigger a nasty tax bill and penalties.

A Real-World Early Retirement Scenario

Let's make this real. Meet Sarah, who is 45 years old and has her sights set on retiring at 50. She's calculated that she'll need $60,000 a year to live comfortably. To make that happen, she starts building her Roth Conversion Ladder now.

- Age 45 (Year 1): Sarah converts $60,000 from her traditional IRA to a Roth. She pays the income tax on this chunk of money out of her cash savings. This first "rung" of her ladder will be fully seasoned and ready for her at age 50.

- Age 46 (Year 2): She converts another $60,000. This rung will be accessible at age 51.

- Age 47 (Year 3): She moves a third $60,000 over, which will be available at age 52.

- Age 48 (Year 4): A fourth $60,000 conversion is made, earmarked for age 53.

- Age 49 (Year 5): She completes her fifth $60,000 conversion, which will mature when she hits 54.

The day Sarah retires at 50, that first $60,000 she converted five years prior is available. She can withdraw that entire amount—tax-free and penalty-free—to fund her first year of freedom. The next year, the second rung is ready, and so on, giving her a predictable income stream.

An Alternative to a 72(t) SEPP Plan

People often compare this strategy to another early access method: a 72(t) Substantially Equal Periodic Payment (SEPP) plan. A 72(t) can also get you penalty-free income, but it's incredibly rigid. Once you start a 72(t), you're locked into taking the exact same calculated distribution amount for five years or until you turn 59½, whichever is longer. No exceptions.

The Roth Conversion Ladder, by contrast, offers incredible flexibility.

- Variable Income: You aren't stuck with a fixed withdrawal amount. If a "rung" has matured, you can pull out any amount up to the total converted principal for that year.

- No Long-Term Commitment: There's no rigid, multi-year payment schedule you're forced to stick to.

- Control Over Taxes: You decide how much to convert each year, giving you direct control over the tax impact during your ladder-building phase.

For anyone serious about an early exit from the workforce, learning how to convert a traditional IRA to a Roth IRA via the ladder strategy is a complete game-changer. It turns funds that felt locked away into a flexible, powerful source of income. This is a complex area, and experts like the team at Spivak Financial Group or a specialized resource like 72tProfessor.com can help you decide if this strategy is the right tool for your early retirement goals.

Strategic Timing and Common Conversion Mistakes to Avoid

Executing a Roth conversion is a powerful move, but knowing when to pull the trigger is just as critical as knowing how. The right timing can slash your tax bill, while the wrong timing can lead to some expensive and irreversible mistakes. Get this part right, and you elevate your strategy from good to great.

One of the absolute best times to convert a traditional IRA to a Roth IRA is during a year when your income is lower than usual. Maybe you're changing careers, taking a sabbatical, or even dealing with an unexpected layoff. Since the converted amount is taxed as ordinary income, a dip in your earnings means you'll pay taxes at a much lower marginal rate.

Another prime opportunity pops up during a stock market downturn. It feels counterintuitive, but when the market is down, so is your IRA balance. Converting at this moment means you're moving the same number of shares over to your Roth, but the dollar value—and thus your tax bill—is significantly less. You're essentially getting a discount on the taxes for assets that have the potential to rebound and then grow tax-free forever.

Sidestepping Common Conversion Pitfalls

Even with perfect timing, I've seen a few common mistakes derail an otherwise solid conversion plan. Navigating these is essential.

- Misunderstanding the 5-Year Rules: This one trips people up all the time. There are two different five-year rules. One applies to your entire Roth IRA for withdrawing earnings tax-free, and another applies to each individual conversion for taking out the principal penalty-free before age 59½. Confusing them can lead to a nasty surprise of taxes and penalties.

- Ignoring the Pro-Rata Rule: If you have any pre-tax money in any of your traditional, SEP, or SIMPLE IRAs, you can't just pick and choose to convert only your after-tax contributions. The IRS looks at all of them together and forces you to convert a proportional mix of pre-tax and after-tax funds, which can trigger an unexpected tax bill.

- Not Having a Plan for the Taxes: The golden rule of conversions is to pay the conversion tax with non-retirement funds. If you use money from the conversion itself to pay the tax, you’re shrinking the amount that gets to grow tax-free. Worse, if you're under 59½, that could also trigger a 10% early withdrawal penalty.

The Medicare IRMAA Surcharge Trap

Here's one of the sneakiest and most expensive mistakes you can make: triggering Medicare’s Income-Related Monthly Adjustment Amount, or IRMAA. A large Roth conversion can spike your income, pushing you into a higher income tier. The result? Steep surcharges on your Medicare Part B and Part D premiums two years down the road.

A big Roth conversion can dramatically increase your Modified Adjusted Gross Income (MAGI), which is the number Medicare uses to set your premiums. This isn't a small change; it can lead to thousands of dollars in extra healthcare costs each year.

Strategic, multi-year planning is the key to avoiding this. For instance, I've worked with couples in their early 60s with $2.4 million in traditional IRAs. We might map out a plan to execute $220,000 conversions each year before they enroll in Medicare. Once they're on Medicare, we could drop the conversion amount to $180,000 to keep them just under the IRMAA income thresholds. You can see more on how this forward-thinking strategy works for early retirees at stwserve.com.

This is the kind of meticulous planning that makes a real difference. The goal is always to maximize your tax-free growth without accidentally creating other financial headaches. A professional at Spivak Financial Group can help you map out a conversion plan that accounts for these nuances, making sure your strategy is both effective and efficient.

Answering Your Top Roth Conversion Questions

Even the most buttoned-up financial plan can leave you with a few lingering questions when it's time to actually convert a traditional IRA to a Roth IRA. Let's walk through some of the most common ones I hear from clients to give you the clarity you need to move forward.

Can I Only Convert Part of My Traditional IRA?

Yes, you can—and frankly, you probably should. You are absolutely not required to convert your entire traditional IRA balance in a single shot.

In fact, breaking the conversion up over several years is one of the smartest tax planning moves you can make. This strategy lets you control the tax hit by converting just enough each year to stay within a desired tax bracket. For example, converting $200,000 at once could easily bump you into a painfully high tax bracket. But converting $50,000 a year over four years? That keeps the tax bill predictable and much more manageable.

What Is the 5-Year Rule for Roth Conversions?

This is a big source of confusion because there isn't just one "5-year rule"—there are two, and they do very different things. Getting them straight is critical for avoiding nasty surprises from the IRS.

-

The Overall Roth IRA 5-Year Rule: This clock starts on January 1st of the year you made your very first contribution to any Roth IRA you own. Once five years have passed and you're over age 59½, you can pull earnings out of your Roth IRAs completely tax-free.

-

The Conversion-Specific 5-Year Rule: This one is different. It applies separately to each amount you convert. For every conversion you do, a unique five-year waiting period begins. If you’re under 59½, you have to let that converted principal sit for five full years before you can withdraw it without getting hit with a 10% early withdrawal penalty. This rule is the powerhouse behind the Roth Conversion Ladder strategy for early retirees.

Think of it this way: The first rule is about when your earnings become tax-free. The second rule is about when your converted principal becomes penalty-free if you need it early.

Can I Undo a Roth Conversion If I Change My Mind?

No. This is a huge one. You cannot reverse a Roth conversion.

Before the Tax Cuts and Jobs Act of 2017, you could do something called a "recharacterization," which was basically a do-over for a Roth conversion. That option is gone. Today, once you pull the trigger on a conversion, that decision is permanent and irrevocable. This makes your upfront planning absolutely essential. You have to be certain about the move and know exactly how you'll pay the taxes before you start the process.

Does My Income Affect My Ability to Convert to a Roth IRA?

Nope. Your income has absolutely no impact on whether you can perform a Roth conversion. There are zero income limits for converting a traditional IRA to a Roth IRA.

The income limits you hear about are for making direct contributions to a Roth IRA. This is an important distinction and is exactly what makes the popular "Backdoor Roth IRA" strategy work for high-income earners. They make a non-deductible contribution to a traditional IRA and then immediately convert it to a Roth, neatly sidestepping the direct contribution limits.

As you map out your long-term plan, it's also a good idea to understand the rules for taking money out. You can learn more about the rules for taxes on a Roth IRA distribution in our detailed guide. Making sure your entire plan—from conversion to withdrawal—is airtight is the key to success.

Navigating the rules around retirement account conversions and distributions can be complex. At Spivak Financial Group, we specialize in helping individuals unlock their retirement funds for early retirement or other life goals. Learn how a 72(t) SEPP plan might fit into your financial picture at https://72tprofessor.com.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

https://72tprofessor.com