Tapping into your 401k before retirement can feel like a lifeline when you're facing a serious financial crunch. But that quick fix comes with a nasty sting: a 10% early withdrawal penalty from the IRS, slapped right on top of your usual income taxes.

The good news? It doesn't have to be that way. The IRS has carved out specific, legitimate exceptions that can help you avoid that penalty and save you thousands. Knowing what they are is the first step.

The Real Cost of Early 401k Withdrawals

When you need cash, that big number on your 401k statement can look awfully tempting. Before you pull the trigger, you absolutely have to understand what it's really going to cost you. This goes way beyond just seeing your retirement balance go down; it’s about immediate, substantial costs that shrink the amount of cash that actually hits your bank account.

The hit comes from two directions. First, since your traditional 401k was funded with pre-tax money, every dollar you take out is taxed as ordinary income for the year. Then, if you’re under age 59½, the IRS piles on that dreaded 10% penalty.

A Real-World Withdrawal Example

Let’s make this real. Imagine you need $20,000 for a massive, unexpected expense. You're in the 24% federal tax bracket and decide your only option is an early 401k withdrawal.

Here’s how the math plays out:

- Initial Withdrawal: $20,000

- Federal Income Tax (24%): -$4,800

- IRS Early Withdrawal Penalty (10%): -$2,000

- Total Reduction: -$6,800

Just like that, your $20,000 withdrawal becomes only $13,200 in your pocket. You lose over a third of it right off the bat. And that’s before we even factor in state income taxes, which could take another bite.

To see the difference an exception makes, have a look at this comparison.

The Real Cost of a $20,000 Early 401k Withdrawal

This table illustrates the financial impact of a standard early 401(k) withdrawal versus a penalty-free withdrawal, assuming a 24% federal income tax bracket.

| Expense Item | Standard Early Withdrawal | Penalty-Free Withdrawal (Using an Exception) |

|---|---|---|

| Gross Withdrawal Amount | $20,000 | $20,000 |

| Federal Income Tax (24%) | -$4,800 | -$4,800 |

| 10% Early Withdrawal Penalty | -$2,000 | $0 |

| State Income Tax (example 5%) | -$1,000 | -$1,000 |

| Net Cash Received | $12,200 | $14,200 |

As you can see, simply qualifying for an exception puts an extra $2,000 directly into your hands—money you would have otherwise handed over to the IRS.

The loss isn't just the immediate tax hit. You also forfeit all future growth and compounding on the withdrawn funds, which could amount to tens of thousands of dollars by the time you actually retire.

Finding a Penalty-Free Path

While the standard rules are tough, the IRS gets that life happens. They’ve built several legitimate escape hatches into the tax code to help people access their funds early without the pain of the 10% penalty. This guide is here to walk you through those options so you can make a smart decision, not a costly one.

We'll dig into several key strategies, including:

- Hardship Exceptions: These cover situations the IRS deems worthy of a penalty waiver, like massive medical bills or disability.

- The Rule of 55: A special provision for people who leave their job in the year they turn 55 or older.

- 72(t) Payment Plans: This is a method for setting up "Substantially Equal Periodic Payments" (SEPPs) to create a steady income stream, no matter your age.

Understanding these rules is your first line of defense. The tax code even makes room for extraordinary circumstances. For example, the CARES Act of 2020 temporarily allowed people affected by the pandemic to withdraw up to $100,000 without the 10% penalty. While that was a unique response to a crisis, it shows that penalty-avoidance strategies are a real and established part of the system. You can discover more insights about these unique exceptions on MortgageCalculator.org.

Navigating IRS Penalty-Free Withdrawal Exceptions

While that 10% penalty is a powerful motivator to keep your retirement funds locked up, the IRS isn't completely inflexible. They understand that major life events happen, and they’ve carved out specific exceptions that let you tap into your 401(k) early without that extra financial hit.

It's important to see these not as loopholes, but as clearly defined, rule-based provisions for genuine, often difficult, life circumstances.

Successfully using one of these exceptions isn't as simple as checking a box on a form. It demands precise documentation and strict adherence to the criteria. For many, the first big question is simply whether they can touch their funds at all. Our guide on understanding how to access 401k funds early is a great place to start sorting through those initial questions.

Total and Permanent Disability

If a medical condition leaves you totally and permanently disabled, the IRS allows you to take distributions from your 401(k) penalty-free, regardless of your age.

To meet the IRS definition, you must be unable to perform any "substantial gainful activity" due to a medically diagnosed physical or mental impairment. The key is that this condition must be expected to either be fatal or to persist for a long, indefinite period.

You will absolutely need a physician's certification to prove this. A common misstep is thinking that a disability award from the Social Security Administration is all you need. While it’s strong supporting evidence, your 401(k) plan administrator will still require their own specific medical proof before they process a penalty-free withdrawal.

Unreimbursed Medical Expenses

Sky-high medical bills can throw anyone's finances into chaos. Recognizing this, the IRS created an exception allowing you to withdraw funds without penalty to cover unreimbursed medical costs that exceed 7.5% of your adjusted gross income (AGI).

Let's walk through a quick example. Imagine your AGI for the year is $80,000. The threshold you have to clear is $6,000 (7.5% of that $80,000). If you're facing $15,000 in medical bills that your insurance didn't cover, you could withdraw up to $9,000 of that ($15,000 minus the $6,000 threshold) from your 401(k) without the penalty.

Important Takeaway: You can only withdraw the amount exceeding the 7.5% AGI floor penalty-free—not the total bill. And don't forget, you’ll still owe regular income tax on every dollar you take out.

Keep meticulous records of everything: doctor invoices, hospital receipts, and insurance statements. This paper trail is non-negotiable when you file your taxes to claim the exception.

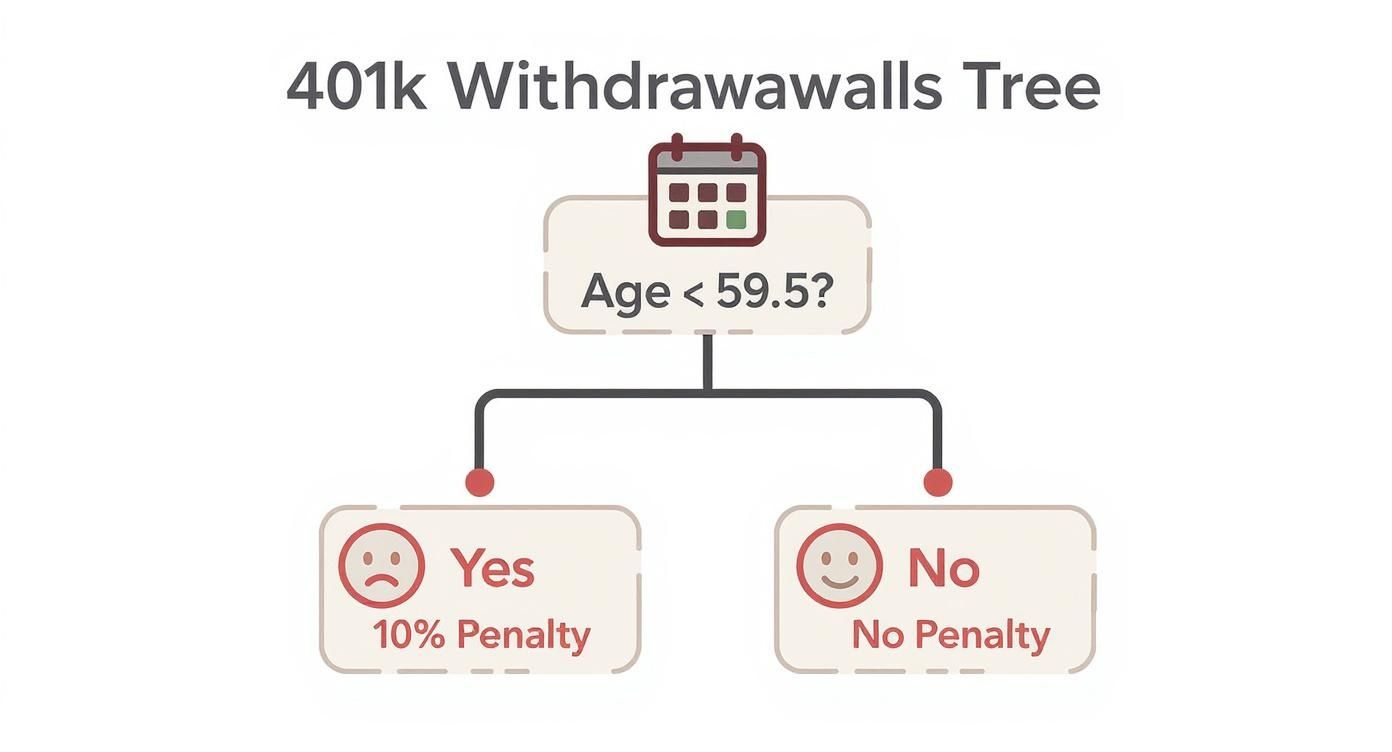

This decision tree shows the first and most basic question in determining if you'll face a penalty.

This visual really simplifies the baseline rule: age is the default trigger for the 10% penalty, but these exceptions provide critical pathways to avoid it.

Qualified Domestic Relations Orders (QDRO)

Divorce proceedings often involve the difficult task of dividing assets, and retirement accounts are usually a huge piece of that puzzle. A Qualified Domestic Relations Order, or QDRO, is a specific type of court order that greenlights the transfer of 401(k) funds to a former spouse, child, or other dependent.

When money is distributed to an "alternate payee" (like your ex-spouse) under a QDRO, the 10% early withdrawal penalty is waived. This is a massive financial relief during an already stressful time.

The key word here is qualified. A generic divorce decree stating that assets will be split won't cut it. The document must contain very specific information mandated by federal law and must be formally approved by the 401(k) plan administrator to be considered a valid QDRO.

Called to Active Duty

Members of the military reserves have a unique provision available if they're called to active duty. If you're a qualified reservist called up for more than 179 days (or for an indefinite period), you can take a penalty-free distribution from your 401(k).

This exception covers withdrawals made anytime from the date you receive your orders until the end of your active-duty period. It’s designed specifically to help military families bridge financial gaps that can pop up during a deployment.

Unlocking the Rule of 55 for Early Retirement

If you're dreaming of leaving the workforce a few years ahead of schedule, the "Rule of 55" might be your golden ticket. It's a powerful—but often misunderstood—IRS provision that lets you tap into your 401(k) without that dreaded 10% early withdrawal penalty.

The concept itself is simple. If you leave your job for any reason—quit, get laid off, or retire—during or after the calendar year you turn 55, you can start taking money from that specific company's 401(k) penalty-free.

This is a game-changer. For many, it's the financial bridge that makes an early exit from the 9-to-5 grind a real possibility, providing income until they hit the standard retirement age of 59½.

How the Rule of 55 Works in Practice

Let's look at a real-world scenario to see how this plays out. Picture two colleagues, Sarah and David.

- Sarah is 56 when her company announces layoffs, and her position is cut. Because she left her employer after turning 55, she has immediate, penalty-free access to her 401(k) funds. She'll still owe regular income tax on the withdrawals, of course, but she dodges the extra 10% hit.

- David is 54 when he decides to leave the same company to start a business. Even though he’s just months from his 55th birthday, the Rule of 55 doesn't apply. If he tries to pull money from his 401(k), he'll face the full 10% penalty on top of income taxes.

The lesson here is crystal clear: the timing of when you leave your job is everything. You have to separate from service in or after the calendar year you turn 55.

Critical Details You Cannot Overlook

Like most things involving the IRS, the devil is in the details. The Rule of 55 has some very specific limitations that can trip people up if they aren't careful.

First and foremost, this rule only applies to the 401(k) plan of the employer you just left. It doesn't work for 401(k)s from previous jobs or for any of your IRAs. If you have money in an old 401(k) you want to access, you'd need to roll it into your current employer's plan before you leave—and that’s only if their plan allows it.

Key Takeaway: The Rule of 55 is tied to a specific 401(k) from a specific employer. The moment you roll those funds into an IRA, you lose this privilege and have to wait until age 59½ for penalty-free access.

Another crucial point is that while the IRS permits this, your employer isn't required to offer it. Most major 401(k) plans do, but you absolutely must check with your plan administrator to confirm their policies before you hand in your notice.

Strategically planning for this is one of the smartest ways how to avoid 401k early withdrawal penalty. It’s a direct path for people leaving their job at 55 or older to access their funds without a penalty, though normal income taxes will always apply to traditional 401(k) withdrawals. For a deeper dive, Schwab has a great detailed guide on the Rule of 55.

When used correctly, the Rule of 55 is a fantastic tool for a well-planned early retirement. Just make sure you understand the fine print before you take the leap.

Using 72(t) Payments for a Steady Income Stream

What if you could create your own personal pension—a steady, predictable income stream straight from your retirement funds—long before you hit the traditional retirement age? That's precisely the idea behind a strategy called Substantially Equal Periodic Payments (SEPP), governed by IRS code Section 72(t).

This is one of the most powerful ways how to avoid 401k early withdrawal penalty. It works by letting you set up a series of scheduled withdrawals at any age, bypassing the dreaded 10% early-out fee.

Think of it as a handshake deal with the IRS. You get penalty-free access to your money early, and in exchange, you agree to take a specific, calculated amount for a predetermined period. This isn't a quick fix for a one-time cash crunch; it's a structured approach for people who need consistent income to bridge the gap to retirement, maybe after an early career exit or to fund a new chapter in life.

Understanding the Three Calculation Methods

The IRS doesn't let you just pull a number out of thin air for your withdrawals. They've laid out three distinct, approved methods for calculating your annual payment. Each one factors in your account balance, life expectancy, and a reasonable interest rate, but the results can vary quite a bit.

-

Required Minimum Distribution (RMD) Method: This is the most straightforward of the three. It simply divides your account balance by a life expectancy factor from an official IRS table. The catch? Your payment gets recalculated every single year, so it will rise and fall with your account balance and age. This usually gives you the smallest payout to start but allows for growth over time.

-

Fixed Amortization Method: This approach calculates a fixed annual payment for the entire life of the plan. It essentially amortizes your account balance over your life expectancy (or joint life expectancy with a beneficiary). Once the number is set, it stays the same. This method is all about predictability—you'll know exactly what's coming in each year.

-

Fixed Annuitization Method: Very similar to the amortization method, this one also delivers a fixed annual payment. It uses an annuity factor from the IRS to figure out the amount, almost like simulating what an insurance company would pay you for a lifetime annuity. The payout is often very close to the amortization method, giving you another solid option for stable, predictable income.

So, how do they stack up?

| Calculation Method | Payment Structure | Typical Payout Amount | Best For |

|---|---|---|---|

| RMD | Recalculated annually, payments fluctuate. | Generally the lowest initial payout. | Someone who needs less income now but wants payments to grow with the market. |

| Amortization | Fixed for the entire plan duration. | Typically a moderate payout. | Someone needing a predictable, stable income that never changes. |

| Annuitization | Fixed for the entire plan duration. | Typically a moderate payout, similar to amortization. | Someone who prefers a calculation based on annuity principles for steady income. |

Choosing the right method is a huge decision that really hinges on your personal financial needs and future plans. For a much deeper dive into these calculations, check out our guide that explains in detail how a 72(t) plan works.

The Unbreakable Commitment of a 72(t) Plan

This is the part you absolutely cannot afford to misunderstand: once you start a 72(t) SEPP, you are locked in. You are legally required to continue taking these exact payments for a minimum of five full years or until you turn 59½, whichever period is longer.

This rule is absolute and unforgiving. If you modify the payments, miss a payment, or stop the plan early for any reason, the consequences are severe. The IRS will retroactively apply the 10% penalty to every single distribution you've taken since the plan began, plus interest.

Let's walk through a real-world example. If you start a plan at age 52, you must keep it going until you're 59½—that’s a 7.5-year commitment. But if you start at age 56, you have to continue until you're 61 (five full years), because that five-year period is longer than the time until you reach 59½.

This rigidity is exactly why a 72(t) plan requires serious thought and a solid financial game plan. It’s a fantastic tool for generating early retirement income, but it offers zero flexibility once it's in motion. One mistake can wipe out all the benefits and leave you with a massive, unexpected tax bill.

Smarter Alternatives to an Early Withdrawal

Before you pull the trigger on a permanent, and potentially very costly, 401(k) withdrawal, it’s absolutely vital to look at the alternatives. Tapping your retirement savings really should be the last resort, never the first move you make. Several smarter strategies can get you the cash you need without torpedoing your nest egg or getting hit with that painful 10% penalty.

One of the most common options out there is a 401(k) loan. This strategy basically lets you borrow from your own retirement savings, turning your account into a source of credit when you need it most.

Deep Dive into 401(k) Loans

Think of a 401(k) loan less like borrowing from a bank and more like borrowing from your future self. The mechanics are pretty simple: you take a loan from your vested account balance and pay it back over time, with interest. The best part? That interest you're paying doesn't go to a lender—it goes right back into your own 401(k), helping you replenish the funds you borrowed.

This setup is a powerful way how to avoid 401k early withdrawal penalty. By using a loan, you sidestep the penalty entirely. Most plans let you borrow up to 50% of your vested balance or $50,000, whichever is less. Repayment is usually spread out over five years. This gives you access to cash without the immediate tax hit or the 10% penalty that comes with a regular distribution. You can learn more about 401(k) loan specifics from Fidelity to see how it keeps your future growth on track.

But—and this is a big but—this option isn't without serious risks you need to think through.

The biggest risk of a 401(k) loan is what happens if you leave your job. Whether you quit, get laid off, or retire, most plans demand you repay the entire outstanding loan balance in a very short timeframe, often within just a couple of months.

If you can't pay it back, the outstanding balance gets reclassified as a distribution. That means it’s now subject to ordinary income taxes and, if you're under 59½, that 10% early withdrawal penalty you were trying to avoid suddenly reappears.

Comparing Your Options Thoughtfully

Deciding between a loan and a structured distribution like a 72(t) SEPP is a complex choice because they serve very different purposes. A loan is perfect for a one-time, short-term cash need when you have a solid plan for paying it back. A 72(t) plan, on the other hand, is built for creating a long-term income stream. It’s essential to explore the differences between a 401(k) loan versus a 72(t) SEPP to make sure your strategy matches your financial goals.

Beyond 401(k) loans, other avenues can provide cash without you having to touch your primary retirement account. Looking at these first might save you from a decision you'll regret later.

Here are a few other alternatives worth considering:

- Roth IRA Contributions: Have a Roth IRA? You can withdraw your direct contributions (not the earnings) at any time, for any reason, completely tax- and penalty-free. It's one of the most flexible sources of emergency cash you can have.

- Home Equity Line of Credit (HELOC): If you're a homeowner with some equity, a HELOC can work like a credit card that lets you draw funds when you need them. The interest rates are often better than personal loans, but it does use your home as collateral, which adds an element of risk.

- Personal Loan: While the interest rates might be higher, a personal loan from a bank or credit union is an unsecured option. It won't put your retirement savings or your home on the line.

Each of these has its pros and cons, but they all share one crucial advantage over an early 401(k) withdrawal: they keep your retirement money invested and growing for the long haul. A permanent withdrawal doesn't just cost you today in taxes and penalties; it also robs your future self of decades of potential compound growth.

Got Questions? We've Got Answers

After digging into the various strategies, you're bound to have some questions. It's totally normal. The rules around 401(k)s can be a maze, and getting straight answers is the only way to feel confident about your next move. Let's tackle some of the most common questions we hear from people just like you.

Can I Use the Rule of 55 on an Old 401k?

Nope, you can't. This is a huge point of confusion that trips a lot of people up. The Rule of 55 only works for the 401(k) plan you have with the company you're leaving. It has to be in the same year you turn 55 or later.

This special rule doesn't apply to old 401(k)s from previous jobs or any money you've already moved into an IRA. If you want to tap into those old funds using this rule, you'd have to first roll them into your current 401(k) before you separate from the company—and that's only if your current plan even accepts incoming rollovers.

What Happens if I Stop My SEPP 72(t) Payments Early?

Stopping your Substantially Equal Periodic Payments (SEPP) early is a financial disaster waiting to happen. Once you start, you're locked in for at least five full years, or until you hit age 59½, whichever is longer.

If you break that agreement for any reason, the IRS comes knocking. They'll retroactively slap the 10% early withdrawal penalty on every single dollar you've taken out since day one, plus interest. It’s a move that can turn a smart strategy into a very expensive lesson. This is why you should only start a SEPP if you are absolutely certain you can stick with the schedule.

This unbreakable commitment is the trade-off for getting your money penalty-free. Before starting a 72(t) plan, you have to be sure your financial situation is stable enough to handle those fixed withdrawals for the entire term.

Do I Still Pay Income Tax if I Qualify for a Penalty Exception?

Yes, you almost always do. Getting out of the 10% early withdrawal penalty is a big win, but it doesn't get you out of paying income tax. Any money you take from a traditional, pre-tax 401(k) is considered ordinary income.

That means the withdrawal amount gets added to your total income for the year and is taxed at your regular federal and state rates. The only real exception here is for a Roth 401(k), where qualified distributions of your contributions and earnings come out completely tax-free.

Is a 401k Loan Better Than a Withdrawal for a Short-Term Need?

For a temporary cash crunch where you know you can pay the money back, a 401(k) loan is almost always the smarter play. A loan isn't a taxable event, so you completely sidestep both the income tax hit and that nasty 10% penalty.

Better yet, you're paying the loan back—with interest—to yourself, directly into your own retirement account. It helps you get back on track. The biggest risk? Leaving your job. If you quit or are laid off, the entire loan balance can become due almost immediately. A withdrawal, on the other hand, is a permanent drain on your retirement savings and should always be your absolute last resort.

Navigating these complex rules requires careful planning and expert guidance. At Spivak Financial Group, we specialize in helping individuals create structured income streams from their retirement accounts. To explore your options and build a penalty-free withdrawal strategy, contact us today.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

The 72(t) Professor