Opening up a Roth IRA is one of the smartest things you can do for your future self, promising a nest egg that's 100% tax-free in retirement. It's far less complicated than it sounds. At its core, the process boils down to three simple actions: making sure you're eligible, picking a financial institution to hold your account, and then actually opening and funding it.

Your Quick Guide to Opening a Roth IRA

Let's cut to the chase. A Roth IRA is a powerhouse retirement tool because you fund it with after-tax dollars. Unlike a traditional IRA or 401(k), where you pay taxes on withdrawals, with a Roth, your qualified distributions in retirement are completely tax-free. This is a massive advantage, especially if you think you’ll be in the same or even a higher tax bracket down the road.

The whole journey kicks off with a quick eligibility check. The IRS has income limits that dictate who can contribute, so you'll want to confirm you're under the threshold first. After that, your biggest decision is simply where to open the account. This single choice affects everything from your investment options and fees to how much you'll need to manage it yourself.

Choosing Your Roth IRA Provider

The "provider" is just the financial company that holds your Roth IRA. Think of them as the home for your investments. The big three are brokerage firms, robo-advisors, and banks, and each one is built for a different type of person. Getting this choice right from the start is key to aligning your account with your personal financial style.

Here at Spivak Financial Group, we've seen time and again that the best fit is a provider that matches a client's comfort level with managing investments and their sensitivity to costs. It might not seem like a big deal, but a tiny difference in annual fees can easily snowball into tens of thousands of dollars lost over your lifetime.

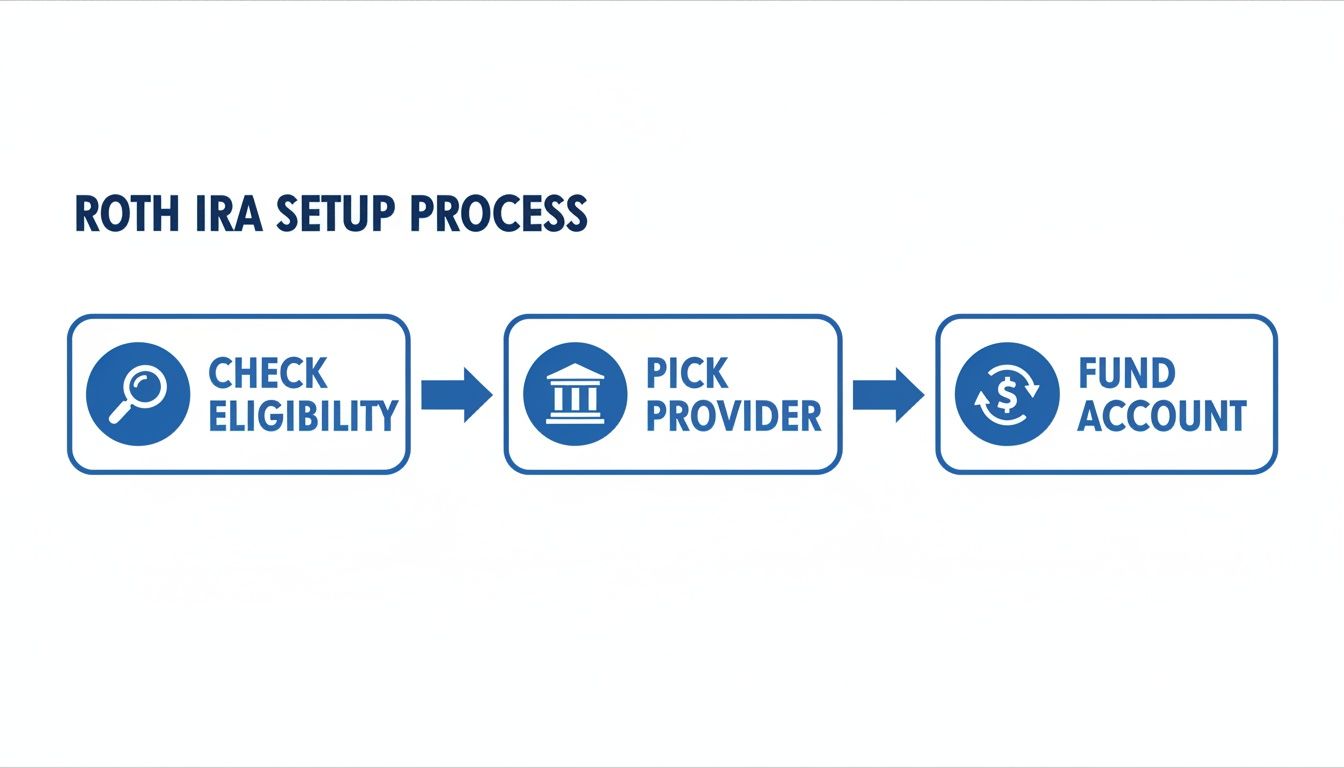

You can really think of the whole setup process in three distinct phases.

This flowchart nails it—once you've confirmed you're eligible, it's all about picking your partner and getting the money in there.

To make that decision a little easier, let's break down what each type of provider brings to the table.

Choosing Your Roth IRA Provider at a Glance

Deciding where to open your account can feel overwhelming, but it really comes down to how hands-on you want to be. This table gives you a quick snapshot of the main players.

| Provider Type | Best For | Investment Options | Typical Fees |

|---|---|---|---|

| Brokerage Firm | The DIY investor who wants total control and a massive menu of stocks, ETFs, and mutual funds. | Extensive; includes individual stocks, bonds, mutual funds, and ETFs. | Low to zero commissions on trades; some may have small account maintenance fees. |

| Robo-Advisor | The hands-off investor who wants a professional, automated portfolio built for them based on their goals. | A curated list of low-cost ETFs managed entirely by the platform's algorithm. | An annual management fee, usually around 0.25% – 0.50% of your balance. |

| Bank or Credit Union | The conservative investor who values safety and familiarity over the potential for high growth. | Very limited; usually just CDs, money market accounts, or high-yield savings. | Generally very low or no account fees, but the returns are significantly lower. |

Picking the right home for your Roth IRA is the foundation of your tax-free retirement strategy. By thinking through these key factors—how much control you want, how much convenience you need, and what costs you're willing to pay—you can confidently choose a provider that will serve you well for years to come. If you need help sorting through these big retirement decisions, that's what we're here for at Spivak Financial Group.

First Things First: Are You Eligible to Contribute?

Before you jump into comparing different providers or picking investments, we need to hit the brakes for a moment. There's a critical gatekeeper to the Roth IRA party: the IRS.

The rules for who can contribute boil down to two simple things: where your money comes from and how much of it you make. Getting this part right is the absolute first step in learning how to set up a Roth IRA correctly.

First, you must have earned income. This is the key. It's money you get from actually working, not from your investments paying you dividends. The IRS is pretty clear on what counts:

- Wages, salaries, tips, and other taxable employee pay

- Commissions and bonuses

- Net earnings from your own business or side hustle

Money from interest, dividends, or capital gains? That doesn't count. Your contribution is capped by your earned income for the year or the annual maximum, whichever is lower.

Understanding the Income Limits

The second hurdle—and the one that trips more people up—is your Modified Adjusted Gross Income (MAGI). If your income climbs too high, the IRS will reduce or even completely eliminate your ability to contribute directly.

These income limits get adjusted for inflation every so often and change based on how you file your taxes.

For 2024, here’s the breakdown of the income phase-out ranges:

- Single, Head of Household, or Married Filing Separately (and didn't live with your spouse): The phase-out starts at a MAGI of $146,000 and ends at $161,000. If you make more than $161,000, you can't contribute directly.

- Married Filing Jointly or Qualifying Widow(er): For couples, the phase-out range is between $230,000 and $240,000. A MAGI over $240,000 means you're ineligible.

If your income lands somewhere in that phase-out zone, you're not totally locked out—but you can only make a partial contribution. This is a common point of confusion.

A Real-World Scenario

Let's say you're a single filer who gets a fantastic and well-deserved promotion. Your salary gets a nice bump, and your MAGI for the year ends up at $150,000.

Because you're in that phase-out range, you can no longer put in the full annual amount. The IRS uses a specific formula to figure out your reduced contribution limit. You can still contribute something, just not the max. Navigating these rules can get tricky fast, which is why having a professional in your corner can make all the difference.

"Many people overlook the nuances of MAGI calculations until it's too late. At Spivak Financial Group, we help clients proactively plan for income changes to ensure they remain eligible or pivot to other strategies like a backdoor Roth IRA if needed."

A great feature many people ask about is the spousal contribution. If one spouse works and the other is a stay-at-home parent, for example, the non-working spouse can absolutely open and fund their own Roth IRA using the household’s earned income. It's a fantastic way for a family to essentially double down on their retirement savings efforts.

When you're ready to explore these options, the team at Spivak Financial Group is here to help at (844) 776-3728.

Finding the Right Home for Your Roth IRA

Alright, you've confirmed you're eligible to contribute. Now for the next major decision: choosing where your Roth IRA will live. This is far more important than just picking a familiar brand name.

The financial institution you select—your custodian—directly influences your investment options, the fees you'll pay, and ultimately, how much your money can grow. Think of this as choosing a long-term partner for your retirement journey.

You have three main candidates: traditional brokerage firms, robo-advisors, and banks or credit unions. Each one serves a different type of investor, and figuring out which fits your style is central to setting up a Roth IRA correctly.

Breaking Down Your Provider Options

Your choice really comes down to how hands-on you want to be.

A traditional brokerage is ideal for the DIY investor who wants full control and a wide selection of stocks, ETFs, and mutual funds. If you’d rather "set it and forget it," a robo-advisor will build and manage a diversified portfolio for you based on your goals, usually for a small annual fee.

Banks and credit unions are the most conservative choice. They generally offer safer, lower-return options like CDs or money market accounts. While secure, they often can't match the long-term growth potential you'd find with an investment-focused provider. Understanding the core differences between these accounts is vital; our guide comparing a 401(k) vs. an IRA vs. a Roth IRA can provide more clarity on that front.

A common mistake we see at Spivak Financial Group is investors focusing solely on a provider's marketing. The real story is in the fee schedule. A seemingly small 0.5% difference in annual fees can compound into tens of thousands of dollars in lost returns over a few decades.

Why Fees Are the Deciding Factor

The financial services industry has become incredibly competitive, which is great news for you. When you're setting up a Roth IRA, you'll find that many major U.S. discount brokerages and robo-platforms now boast zero account opening fees and extremely low expense ratios on popular index funds—often between 0.03% and 0.20%.

This shift makes cost a primary differentiator. Over time, even a 0.5%–1.0% difference in annual fees on a $200,000 portfolio can erode your wealth significantly. That makes a thorough fee comparison an absolutely essential step. You can discover more insights about how providers present their fee structures directly from their own resources.

This is where you need to get granular and look past the flashy dashboards. The hidden costs are what will impact your bottom line the most.

Your Provider Evaluation Checklist

Before you commit, ask yourself these critical questions about any provider you're considering. This simple checklist ensures you cover all the important bases.

- What are the account fees? Are there annual maintenance fees, inactivity fees, or account closure fees? Dig into the fine print.

- What are the investment costs? Look at the expense ratios on the mutual funds or ETFs you plan to buy. Are there commissions on trades?

- Is the platform easy to use? A confusing interface can be a major barrier. Can you easily open, fund, and manage your account online or through a mobile app?

- What is the quality of customer support? Can you easily reach a real person by phone or chat if you run into a problem?

Taking the time to answer these questions will help you find a provider that not only meets your investment needs but also protects your hard-earned money from unnecessary costs. Getting this right sets you up for long-term success.

The Nuts and Bolts of Opening Your Account

Now that you've confirmed you're eligible and picked a provider, you're ready to make it official. The actual process of opening a Roth IRA is surprisingly painless and usually takes about 15 minutes online.

To get going, you'll need to have some basic personal info ready. Financial institutions are required by law to verify who you are—a standard fraud prevention measure—so they’ll ask for a few common details.

Information You Will Need

Having these items on hand before you start will make the application a breeze.

- Social Security Number or Taxpayer ID Number (TIN): This is how the IRS keeps track of your account.

- Driver's License or Other Government-Issued ID: Standard identity verification.

- Your Contact Information: Your physical address, email, and phone number.

- Employment Details: Be ready with your employer's name and address.

- Bank Account Information: You’ll want your bank's routing number and your account number handy to set up electronic funding.

With your account officially open, the next step is putting money into it. You've got a few ways to fund your new Roth IRA, and the right choice often depends on where the cash is coming from.

Funding Your New Roth IRA

The most straightforward way to fund your account is with a simple electronic transfer from your linked bank account. Most platforms let you set this up as a one-time deposit or, even better, as recurring automatic investments. It's a fantastic way to put your savings on autopilot.

Another powerful option is a rollover from a different retirement plan, like an old 401(k) from a past employer. This lets you bring your retirement assets together under one roof. Of course, you'll want to be sure you understand the rules and any tax implications. You can dig into the specifics in our detailed guide on the 401(k) rollover to an IRA while still employed.

A critical piece of advice from our team at Spivak Financial Group is to be mindful of contribution deadlines. You can contribute for a specific tax year right up until the tax-filing deadline, which is typically April 15 of the following year. This flexibility offers a strategic window for last-minute financial planning.

Knowing the contribution rules is just as vital as picking a funding method. The IRS sets annual limits on how much you can sock away in an IRA. When the Roth IRA first appeared back in 1997, the limit was a modest $2,000. It has climbed steadily over the decades, hitting $7,000 for the 2024–2025 tax years. You can see the historical evolution of these contribution limits and watch how they've grown.

For savers aged 50 and over, the IRS offers an extra boost called the catch-up provision. This lets you contribute an additional $1,000 per year, raising your total potential contribution to $8,000 if you're 50+ in 2025. It’s a great feature designed to help people closer to retirement ramp up their savings.

Putting Your Money to Work: Your First Investments

Alright, congratulations! You've officially opened and funded your Roth IRA. Now comes the part where the real magic happens: actually investing the money.

It's a surprisingly common mistake to let contributions just sit in the account's cash settlement fund. That's a huge missed opportunity. The money earns next to nothing there, defeating the whole purpose. The true power of a Roth IRA comes from the tax-free growth of your investments over decades, so putting that cash to work is non-negotiable.

This step can feel like the most intimidating, but I promise it doesn't have to be complicated. Your goal is to choose investments that line up with your financial goals, your timeline until retirement, and your personal comfort level with the market's ups and downs.

Choosing Your Investment Path

When you're just starting, you really don't need to overcomplicate things. In fact, keeping it simple is often the best strategy. There are several straightforward and incredibly effective options perfect for a new Roth IRA. The key is to avoid "analysis paralysis" and just get your money in the game so it can start compounding.

Here are a few of the most popular starting points:

- Target-Date Funds: These are the ultimate "set it and forget it" option. You just pick a fund with a year closest to when you think you'll retire (like a "Target 2060 Fund"). The fund manager does the rest, automatically adjusting the mix of stocks and bonds to get more conservative as you get older.

- Low-Cost Index Funds or ETFs: These are a favorite for a reason. These funds simply aim to mirror a broad market index, like the S&P 500. For a very low fee, you get instant diversification across hundreds or thousands of companies.

- Individual Stocks: This is for the hands-on investor who enjoys the research. Buying individual company stocks gives you more control, but it also requires more active management and carries significantly more risk than a diversified fund.

At Spivak Financial Group, we often see new investors get stuck right here. The best advice I can give is to start simple. A single, well-diversified, low-cost index fund is a fantastic and powerful starting point for the vast majority of people setting up their first Roth IRA.

Aligning Investments with Your Timeline

Your investment strategy should be a direct reflection of your personal situation. The two biggest factors to consider are your risk tolerance and your time horizon.

Your time horizon is just a fancy way of saying how many years you have until you plan to use this money. If you're in your 20s or 30s, you have decades for your investments to grow and recover from any market downturns. This long runway generally allows for a more aggressive portfolio, weighted heavily toward stocks for their higher growth potential.

On the flip side, if you're nearing retirement in the next five to ten years, your focus will naturally shift from aggressive growth to capital preservation. In this case, a larger allocation to less volatile investments like bonds probably makes more sense.

Think of it this way: the further away your retirement destination, the more fuel (risk) you can afford to burn for speed (growth). The closer you get, the more you want to focus on a smooth, safe landing. Making these informed choices is the final, crucial step in learning how to set up a Roth IRA for long-term success.

Common Questions About Setting Up a Roth IRA

Even with a step-by-step guide, it's natural for a few specific questions to pop up when you're getting ready to open a Roth IRA. Getting these answers straight can give you that final bit of confidence to pull the trigger and get your account working for you.

Let's walk through some of the most common questions people have during the setup process.

Can I Have a Roth IRA and a 401(k) at the Same Time?

Absolutely. Not only can you have both, but it's a fantastic strategy for diversifying your tax situation in retirement.

The contribution limits for your workplace 401(k) are completely separate from your personal Roth IRA. This means you can max out your 401(k) and also contribute the full amount to your Roth IRA in the same year, provided you meet the income requirements.

Having both pre-tax money (in a traditional 401(k)) and post-tax money (in a Roth IRA) gives you incredible flexibility down the road. You can learn more about how this plays out by understanding the taxes on a Roth IRA distribution.

What Happens If I Contribute but My Income Is Too High?

This is a really common fear, especially if your income tends to fluctuate or you get a surprise bonus at the end of the year. Don't panic. If you contribute to a Roth IRA and later realize your income was over the IRS limit for the year, you have a few ways to fix it before the tax deadline.

The most common solution is to recharacterize the contribution. This is just a fancy way of saying you ask your brokerage to move your contribution—plus any money it earned—from the Roth IRA into a Traditional IRA. It's like you hit an undo button, and the IRS treats it as if you had put the money in the Traditional IRA from the very beginning, saving you from any excess contribution penalties.

What Is a Backdoor Roth IRA?

A backdoor Roth IRA isn't some official account type you can open. It's simply a strategy—a completely legal one—that high-income earners use to get money into a Roth IRA when they're phased out of contributing directly.

Here's how it works in two simple steps:

- You make a non-deductible contribution to a Traditional IRA.

- Then, you immediately convert that Traditional IRA to a Roth IRA.

Because the initial contribution was made with after-tax dollars, the conversion itself usually has little to no tax impact, assuming you don't have other pre-tax funds sitting in other Traditional IRAs.

For many high earners, the backdoor Roth IRA is the only game in town. It's the one strategy that allows them to move thousands of dollars into a Roth account each year, even when their income is well above the normal limits.

Do I Have to Invest My Contributions Immediately?

You don't have to, but you absolutely should. This is one of the most critical mistakes I see new investors make. They do the hard part of funding their Roth IRA and then just let the cash sit there, uninvested, in the account's settlement fund.

While the money is technically "in" your Roth, it's not doing anything for you. The real magic of a Roth IRA comes from decades of tax-free compound growth on your investments. As soon as your contribution clears, put that money to work by choosing your investments, whether that's a simple index fund or a target-date fund.

Navigating the rules of retirement accounts can be complex, but you don't have to do it alone. At Spivak Financial Group, we specialize in helping individuals plan for their financial future, including early retirement strategies. Contact us to see how we can help you achieve your goals.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

Learn more at https://72tprofessor.com.