The 60-day IRA rollover rule is a pretty straightforward concept, but one where the details really matter. In short, it’s an IRS regulation that gives you a two-month window to move money from one retirement account to another without getting hit with taxes or penalties.

If you get a check from your old 401(k) or IRA, you have precisely 60 calendar days to deposit the full, original amount into a new retirement account. Get it done in time, and it's a valid, tax-free rollover.

What Is the 60-Day Rollover Rule?

When you leave a job or just want to consolidate your retirement accounts, you’ve got a couple of ways to move the money. One of these is called an "indirect rollover," and this is the one governed by that strict 60-day rule.

Think of it like getting a short-term, interest-free loan from your own retirement savings. The second you receive that distribution check from your old plan administrator, a 60-day countdown starts ticking.

Your mission is simple: get that money into a new, eligible retirement account before the clock hits zero. If you succeed, the transfer is completely tax-free and penalty-free, keeping your nest egg growing without interruption.

But if you fail to meet that deadline, the consequences are severe. The IRS will reclassify the entire distribution as a taxable withdrawal. This means two things happen:

- The full amount is added to your gross income for the year and taxed at your ordinary income tax rate.

- If you're under age 59½, you'll almost certainly face an additional 10% early withdrawal penalty on top of the income tax.

Why This Rule Is So Important

The 60-day window is a critical piece of the U.S. retirement puzzle, especially with how often people change jobs these days. With millions of Americans switching employers every year, this rule provides a structured way to consolidate retirement assets and keep them growing.

In fact, research shows that a huge percentage of new IRAs are funded entirely with rollover money, which tells you just how vital this process is for building long-term wealth. Many people start planning their rollover well before they even leave an employer just to make sure they get it right. You can explore more about how rollovers are shaping the retirement landscape to see the full picture.

The cost of a simple mistake can be staggering. Imagine you miss the deadline on a $100,000 rollover. Assuming a 24% federal tax bracket, that could trigger a $24,000 tax bill plus a $10,000 early withdrawal penalty. Just like that, $34,000 of your savings is gone.

Getting this rule right isn't just about following the IRS's playbook; it's about protecting the financial future you've worked so hard to build. At Spivak Financial Group, we help clients navigate these exact complexities, making sure every dollar keeps working toward their retirement goals.

How to Complete an Indirect Rollover Step by Step

Pulling off an indirect rollover without a hitch really comes down to careful execution. One wrong move and you could find yourself in a tax nightmare. This roadmap breaks the whole thing down into four key steps, getting you from withdrawal to deposit while staying on the right side of the IRA rollover 60 days rule.

Following these steps is your best bet for moving your retirement funds safely and without triggering any penalties. The process itself isn't complicated, but the devil is in the details—especially when it comes to deadlines and tax withholding.

Step 1: Initiate the Distribution

First things first, you need to get in touch with the administrator of your old retirement plan, whether it's a 401(k) or another IRA. Tell them you want a full distribution of your funds. You have to be crystal clear that you intend to perform a rollover, and for an indirect one, you must specify that the check should be made payable directly to you.

Step 2: Receive Your Funds and Start the Clock

The moment you get that check, the 60-day countdown begins. This is the single most critical part of the entire process. The IRS is notoriously strict with this deadline, and it includes every single weekend and holiday. Mark the date on your calendar, set a few reminders on your phone—do whatever you need to do to remember that final deposit day.

The 20% Withholding Trap: If you're moving money out of an employer plan like a 401(k), the plan administrator is legally required to withhold 20% for federal income taxes. This isn't optional; it's a mandatory rule for indirect rollovers from employer plans and it can create a huge shortfall if you aren't ready for it.

Step 3: Prepare Your New IRA

Ideally, before your check even arrives, you should have already opened a new IRA with the financial institution of your choice. Make sure the new account is set up and ready to accept the rollover deposit. If you’re not familiar with how different accounts work, learning about other transfer rules, like those for a SIMPLE IRA transfer, can give you some helpful background.

Step 4: Deposit the Full Gross Amount

This is where that 20% withholding rule really comes into play. You are required to deposit the entire original amount of your distribution into the new IRA—not just the smaller amount you received in the check.

Let's look at an example of how this shortfall works:

- Original 401(k) Balance: $100,000

- Mandatory 20% Withholding: $20,000

- Check You Receive: $80,000

- Amount You Must Deposit: $100,000

To complete a totally tax-free rollover, you have to find that missing $20,000 somewhere—usually from your personal savings—and deposit it along with the $80,000 check. The good news is you’ll get that withheld $20,000 back when you file your tax return for the year. But you absolutely have to front the money yourself to prevent that portion from being taxed and penalized.

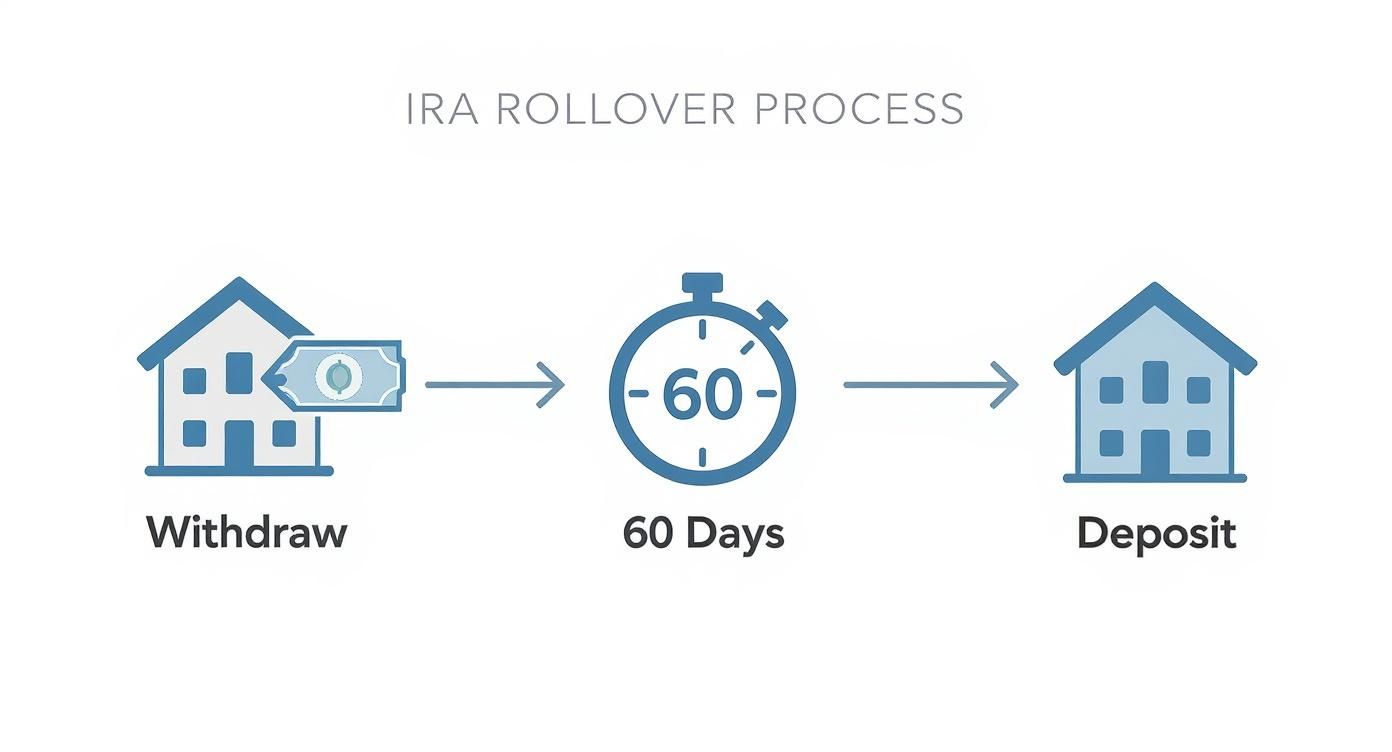

This simple graphic shows the basic flow of a rollover, which is the foundation of this 60-day process.

The visual drives home the point: the money has to move from one qualified plan and end up in another to keep its tax-deferred status.

Common Rollover Mistakes That Trigger Penalties

Trying to handle an indirect rollover yourself is a bit like walking a tightrope. It requires careful attention to detail, because a few common slip-ups can easily turn a tax-free move into a costly, taxable distribution. Even financially savvy people can stumble into these traps, but understanding them ahead of time is the best way to protect your nest egg during the IRA rollover 60 days process.

These aren't some obscure technicalities buried deep in the tax code; they are frequent, real-world errors the IRS sees every single year. By getting familiar with these pitfalls now, you can manage your funds with confidence and sidestep those dreaded tax bills and penalties.

Misunderstanding The One-Rollover-Per-Year Rule

One of the most confusing regulations out there is the IRS's "one-rollover-per-year" rule. A lot of people hear that and assume it limits all types of rollovers, but the rule is actually much more specific. It applies only to rollovers between two IRAs—for example, moving money from one traditional IRA to another traditional IRA.

You're allowed to make just one of these IRA-to-IRA indirect rollovers in any 12-month period. That's it. However, this limit doesn't touch other common types of retirement account moves.

Here’s what the rule does not limit:

- Plan-to-IRA Rollovers: Moving money from a 401(k), 403(b), or other employer plan into an IRA. You can do this as many times as you need to within a year.

- Roth Conversions: Shifting funds from a traditional IRA to a Roth IRA is not considered a rollover for the purposes of this rule.

- Trustee-to-Trustee Transfers: These are direct transfers where the money goes straight from one financial institution to another. Since you never personally touch the funds, you can make an unlimited number of these.

This distinction is absolutely critical. If you're just consolidating an old 401(k) into a new IRA, the one-per-year rule isn't something you need to worry about. For a deeper dive into the specifics of employer plans, our guide on how to take money from a 401(k) offers more context.

Failing to Replace The 20% Withholding

When you take a distribution from an employer plan like a 401(k), the plan administrator is required by law to withhold 20% for federal taxes. This is where a very common and very expensive mistake happens: depositing only the 80% check you received into your new IRA. As far as the IRS is concerned, that's an incomplete rollover.

To complete a fully tax-free rollover, you must deposit 100% of the original gross amount, even though you only received a check for 80%. This means you have to come up with the missing 20% from another source, like your personal savings account.

The good news is you'll get that withheld money back when you file your annual tax return. But you absolutely have to front the cash within the 60-day window to avoid having that missing 20% taxed as income and hit with an early withdrawal penalty.

Miscalculating The 60-Day Window

The 60-day deadline is brutally strict. It starts the day after you receive the funds and includes every single day—weekends and holidays are counted. There is no grace period. If your 60th day happens to land on a Sunday or a federal holiday, too bad. You don't get an extension to the next business day.

The only safe way to approach this is to plan on making your deposit long before the deadline is even on the horizon. A simple calendar mistake can blow up the entire rollover. At Spivak Financial Group, we tell our clients to aim for day 45 as their absolute latest, which builds in a cushion for any unexpected delays. To make sure your timeline is secure, give us a call at (844) 776-3728.

What to Do If You Miss the 60-Day Deadline

Realizing you’ve blown past the IRA rollover 60-day deadline can send a jolt of panic through anyone. Your first thought might be that the money is now permanently stuck outside of its tax-advantaged home, triggering a massive tax bill and penalties.

The good news? It’s not automatically a lost cause. The IRS knows that life happens, and they’ve built-in some relief options for situations that are genuinely beyond your control. While that 60-day window is firm, it isn't always unbreakable.

IRS Relief for Missed Rollovers

The IRS has the power to waive the 60-day requirement if enforcing it would be "against equity or good conscience." This isn't a get-out-of-jail-free card for simple forgetfulness, but it does cover legitimate events like a natural disaster, a serious illness, or other circumstances you couldn't reasonably have prevented. Think of it as a safety net for when a serious, documentable problem gets in the way of your best-laid plans.

To make things a little easier, the IRS created a self-certification procedure. This is a game-changer. It allows you to certify—under penalty of perjury—that you missed the deadline for one of 11 specific, pre-approved reasons. If your situation fits one of those scenarios, you can sidestep the expensive and time-consuming process of requesting a formal private letter ruling from the IRS.

For a self-certification to be valid, you have to make the rollover contribution to the new IRA as soon as you possibly can after the reason for the delay is gone. If you wait more than 30 days after the issue is resolved, the IRS will generally not consider that a reasonable delay.

This self-certification is a powerful tool, but you have to use it correctly. It involves preparing a written letter for the financial institution that will be receiving your late rollover, clearly stating which of the approved reasons applies to your case.

Valid Reasons for Self-Certification

The IRS provides a specific list of circumstances where you can self-certify that you missed the deadline for a valid reason. You just need to meet one of these conditions to qualify.

Here are some of the most common reasons people use:

- Financial Institution Error: The bank or brokerage firm receiving or sending the money made a mistake that caused the delay.

- Lost or Misplaced Check: The distribution check got lost in the mail, you misplaced it, or for some reason, it was never cashed.

- Serious Personal Issues: You were dealing with a severe illness, the death of a family member, or were hospitalized.

- Postal Errors: A verifiable mistake by the U.S. Postal Service held up your check.

- Home Damaged: Your primary residence was severely damaged, perhaps in a storm or another disaster.

If your situation lines up with one of the approved reasons, you can write a letter to your IRA custodian. This letter simply needs to state that you're making a late rollover contribution and that you qualify for a waiver under the self-certification rules. Navigating these complex situations can be tricky, and the team at Spivak Financial Group can offer guidance. Feel free to contact us at (844) 776-3728 to talk through your options.

How to Report Your Rollover on Your Tax Return

You’ve successfully navigated the IRA rollover 60 days deposit window. Great job! But you're not quite at the finish line yet. The final, crucial step is reporting the transaction correctly on your tax return. This is how you prove to the IRS that the whole thing was a non-taxable event.

If you skip this part, all that careful planning goes out the window, and the IRS might treat the entire distribution as taxable income. Ouch. The good news is that once you know which forms to look for, telling the story to the IRS is pretty straightforward. Think of it as creating a simple paper trail showing the money left one account and landed safely in another within the legal timeframe.

Understanding Your Key Tax Forms

When tax season rolls around, keep an eye out for two specific forms that tell the two halves of your rollover story. The IRS looks at both to confirm everything was handled by the book.

- Form 1099-R (Distributions from Pensions, Annuities, etc.): This one comes from the financial institution you took the money from. It's their official record of the distribution you received.

- Form 5498 (IRA Contribution Information): This form is sent by the new institution where you deposited the funds into. It reports the rollover contribution you made.

These two forms are a team. The 1099-R essentially tells the IRS, "This person took money out," and the 5498 follows up with, "Don't worry, they rolled that money right into a new retirement account." When the numbers match, you've shown them a legitimate, non-taxable move.

Decoding Your Form 1099-R

The most important piece of information on your Form 1099-R is in Box 7. This little box contains a distribution code that tells the IRS why you took the money out.

For a rollover from a 401(k) or other employer plan, you'll probably see code ‘G’ for a direct rollover. If you did an indirect rollover (where the check was made out to you), you’ll likely see code ‘1’ if you're under 59½ or ‘7’ if you're over 59½. Getting familiar with these codes is key, and you can get the full rundown in our lesson on interpreting your Form 1099-R.

Reporting the Rollover on Your Form 1040

Okay, this is the final piece of the puzzle: reporting the rollover on your personal tax return, Form 1040. This is where you connect the dots and make it crystal clear to the IRS that no tax is due.

The goal is simple: report the total distribution on your tax return but show that the taxable amount is $0. This action officially tells the IRS that you completed a valid rollover.

Here’s the play-by-play for your Form 1040:

- Find line 4a (for IRAs) or 5a (for pensions and annuities). Report the total gross distribution from Box 1 of your Form 1099-R here.

- On the very next line, 4b or 5b, you will enter $0 for the taxable amount.

- Next to that line, simply write the word "ROLLOVER" to explain why the taxable amount is zero.

That's it. This simple act of reporting the gross amount and then zeroing out the taxable portion is what officially closes the loop. It confirms you followed the IRA rollover 60 days rule and keeps your retirement nest egg growing tax-deferred, exactly as planned.

Your Top IRA Rollover Questions Answered

Even after getting the basics down, it’s natural to have a few lingering questions about the IRA rollover 60 days rule. Think of this as your final check-in, where we tackle the most common "what ifs" to make sure you're ready to move forward with total confidence.

Let's clear up these common points of confusion so you have a complete picture of the rules and can sidestep any costly mistakes.

Can I Temporarily Deposit a Rollover Check Into My Bank Account?

Yes, you certainly can. Once that check is in your hands, the money is yours to hold in a personal checking or savings account during the 60-day window.

Just remember, that clock starts ticking the moment you receive the funds. It is 100% your responsibility to get the full, original gross amount redeposited into a new IRA before day 60. If your old 401(k) provider withheld taxes, you'll have to come up with that cash out of your own pocket to complete a full tax-free rollover.

Does the One Rollover Per Year Limit Apply to a 401(k) to IRA Transfer?

This is a huge point of confusion, and the answer is no, it does not. It's a critical distinction to understand. The one-rollover-per-12-month rule applies only to rollovers between two IRAs (like from one traditional IRA to another traditional IRA).

Moving money from an old employer plan—like a 401(k), 403(b), or the federal Thrift Savings Plan (TSP)—into an IRA is completely exempt from this rule. You are free to do as many of these types of rollovers as you need to in a single year without breaking the once-per-year limit.

Key Takeaway: The once-per-year rule exists to stop people from repeatedly taking short-term, tax-free loans from their IRA. It was never intended to get in the way of consolidating old 401(k)s into a central IRA.

What Is a Safer Alternative to a 60-Day Rollover?

Without a doubt, the safest and most recommended method is a direct rollover, which you’ll often hear called a trustee-to-trustee transfer. For most people, this is the superior option, and it's what most financial pros will tell you to do.

With a direct rollover, you never touch the money. The funds are wired directly from your old 401(k) custodian to your new IRA custodian. This simple change eliminates nearly all the risk and offers massive advantages:

- No 60-Day Deadline: The countdown is a non-issue because the money never hits your bank account.

- No 20% Withholding: That mandatory 20% federal tax withholding from a 401(k) distribution doesn't apply.

- Massively Reduced Risk: It almost completely removes the possibility of a costly mistake, like missing the deadline or failing to replace withheld tax money.

How Does the IRS Know I Completed My Rollover Correctly?

The IRS follows the money using a simple but effective paper trail created by tax forms. They connect the withdrawal from your old account to the deposit into your new one.

Here’s how it works: Your old plan custodian sends the IRS a Form 1099-R, reporting that you took a distribution. Then, your new IRA custodian sends the IRS a Form 5498, showing they received a rollover contribution.

When you file your taxes, you’ll report the distribution shown on your 1099-R but you'll also note that it was rolled over, making the taxable amount $0. As long as the numbers on these forms match what you report, the IRS sees it as a complete, non-taxable event.

Navigating the complexities of retirement fund management is our specialty. At Spivak Financial Group, we help clients make informed decisions to protect and grow their assets for the future. Whether you're considering a rollover or exploring early retirement strategies, we're here to provide the expert guidance you need. Learn more by visiting us at https://72tprofessor.com.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

https://72tprofessor.com