An IRA rollover within 60 days is a way to move your retirement money tax-free, but it puts you on a strict timeline. You personally take possession of the funds and have exactly 60 calendar days to get them into another retirement account. It's often called an indirect rollover, and while it gives you temporary access to your cash, it’s loaded with rules that can trip you up if you aren't careful. It’s a completely different beast than a direct, trustee-to-trustee transfer, and knowing the difference is key to protecting your nest egg.

Understanding The 60 Day IRA Rollover Rule

When you need to move money between retirement accounts, you really have two choices: a direct rollover or an indirect, 60-day rollover. The 60-day route is unique because, for a short time, your retirement savings are sitting in your personal bank account.

Here’s how it works. You ask for a distribution from your 401(k) or IRA, and the custodian cuts you a check. The moment you get that money, the clock starts ticking—you have 60 days on the dot. To avoid taxes and penalties, you have to deposit that entire amount into another IRA before the deadline hits. Think of it as a very short-term, interest-free loan from yourself.

The Critical Once-Per-Year Limitation

One of the biggest gotchas is the once-per-year rollover limit. This rule has gotten much tougher over the years. Back before 2015, you could do a 60-day rollover for each separate IRA you owned within a year. It was a bit of a loophole.

The IRS slammed that door shut. Now, all of your IRAs—Traditional, Roth, SEP, and SIMPLE—are lumped together and treated as one big account for this rule. That means you get only one IRA-to-IRA 60-day rollover across your entire portfolio in any 12-month period. This change was a big deal, and it means you have to be much more strategic about your rollovers.

Key Takeaway: The once-per-year rule applies to all your IRAs combined, not each account individually. Mess this up, and the rollover gets disqualified, triggering taxes and penalties.

It's important to know this limit doesn't apply to direct trustee-to-trustee transfers, which is a big reason they're often the better choice. It also doesn't apply to Roth conversions. And if you’re dealing with different account types, there are other specific guidelines to follow, which is why it's good to understand the nuances of SIMPLE IRA transfer rules if one is involved.

Direct Vs Indirect Rollovers

Choosing how to move your funds is probably the most important decision you'll make in this whole process. While the 60-day rollover gives you temporary use of your cash, the direct rollover is almost always the safer, simpler bet. With a direct rollover, the money goes straight from one custodian to the next. You never touch it, which completely eliminates the risk of missing a deadline or dealing with tax withholding headaches.

Let’s put these two methods side-by-side to really see the differences.

Direct Rollover Vs Indirect 60 Day Rollover

This table breaks down the two main ways you can move your retirement funds. As you'll see, the method you choose has significant implications for taxes, risk, and overall complexity.

| Feature | Direct Rollover (Trustee-to-Trustee) | Indirect Rollover (60-Day) |

|---|---|---|

| Fund Handling | Funds are transferred directly between financial institutions. You never touch the money. | You receive a check for the distribution amount and are responsible for depositing it. |

| Tax Withholding | No mandatory tax withholding. 100% of your funds are moved to the new account. | Mandatory 20% federal tax withholding for distributions from employer plans (like 401(k)s). |

| Deadline Risk | No risk of missing the 60-day deadline, as the transfer is handled by the institutions. | High risk. Missing the 60-day deadline results in the distribution becoming taxable income plus potential penalties. |

| Once-Per-Year Rule | Not subject to the once-per-year rollover limitation. You can do as many as needed. | Limited to one IRA-to-IRA rollover across all your accounts within a 12-month period. |

| Complexity | Simple and hands-off. The custodians manage the entire process for you. | Requires careful tracking, documentation, and personal responsibility to complete correctly. |

Ultimately, while the 60-day rollover offers a level of flexibility, the direct rollover provides peace of mind. For most people, avoiding the stress of deadlines and tax withholding makes the direct, trustee-to-trustee transfer the clear winner.

Executing Your Rollover: A Timeline For Success

Pulling off an IRA rollover within 60 days isn't something you can do casually. It demands precision. Every single day on that calendar counts, and one small mistake can create a surprisingly large tax headache. The trick is to have a clear game plan from the moment you decide to move your money until it's safely tucked away in its new account.

Here’s the detail that trips up so many people: the clock doesn't start when your old custodian cuts the check. The 60-day countdown begins the moment you physically receive the funds. This tiny distinction is the number one reason rollovers fail, and it can derail your plans in a hurry.

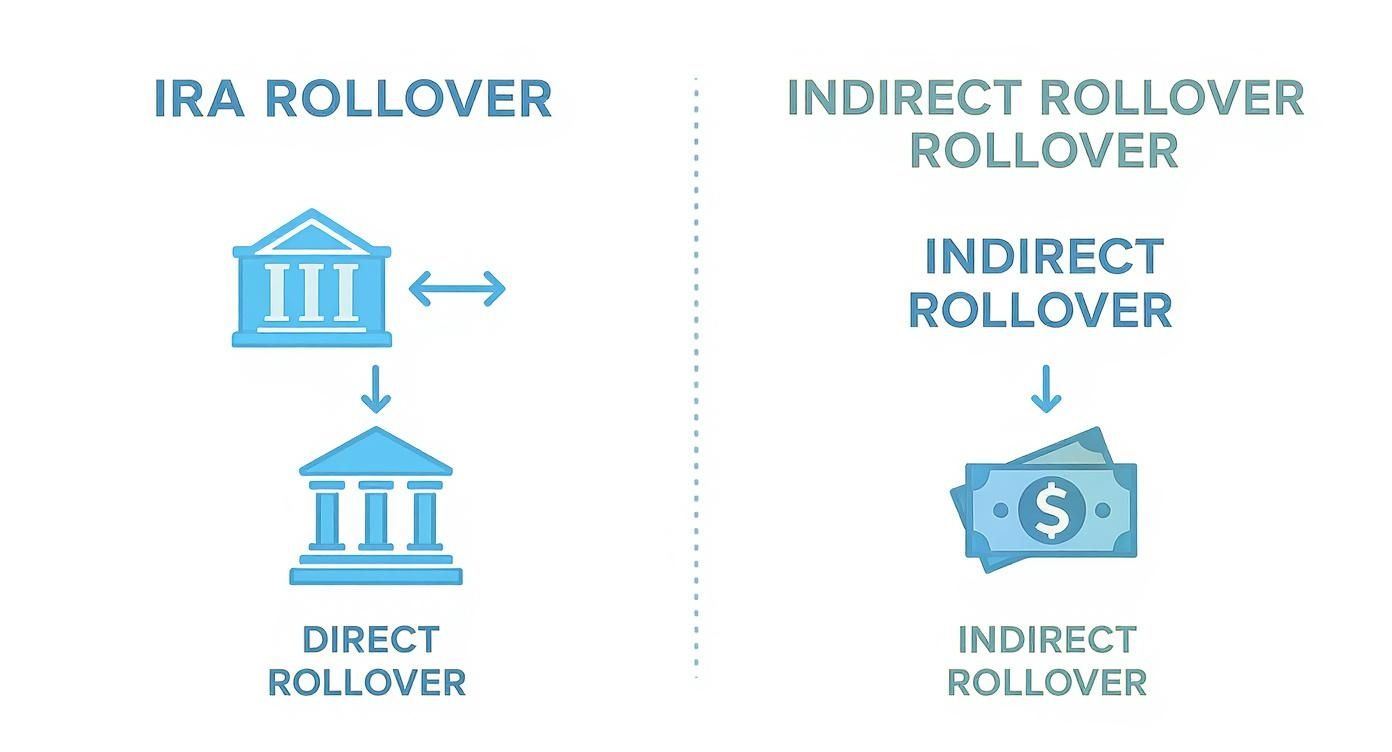

This visual breaks down the two main ways to move your money, showing just how different a direct, hands-off rollover is from an indirect one where you're holding the cash.

As you can see, a direct rollover is a simple transfer between your financial institutions. With an indirect rollover, you take possession of the funds, which means you also take on all the responsibility—and the risk.

Getting Started: Initiating The Withdrawal

First things first, you'll need to reach out to the administrator of your current retirement plan, whether it's a 401(k), 403(b), or another IRA. You’ll have to request a distribution, making it crystal clear you plan to do an indirect rollover. Get ready for some paperwork.

This is also the point where a critical rule kicks in if you're moving money from a company plan like a 401(k). The plan administrator is required by law to withhold 20% of your money for federal taxes. This isn't optional for indirect rollovers from employer plans.

So, if you’re rolling over $100,000 from your 401(k), you won't get a check for that amount. You'll only receive $80,000. The other $20,000 gets sent straight to the IRS. Honestly, this mandatory withholding is a huge reason most people choose a direct, trustee-to-trustee transfer instead.

The Clock is Ticking: Receiving the Funds and The Withholding Trap

The day that check arrives, your 60-day clock officially starts. Now you’re facing the 20% withholding problem. To complete a 100% tax-free rollover, you have to deposit the entire original distribution amount, not just the cash you received.

Let's stick with our example:

- Your Total Distribution: $100,000

- Tax Withheld by Your Old Plan: $20,000

- The Check You Actually Get: $80,000

To keep this entire transaction tax-free, you must deposit the full $100,000 into your new IRA within the 60-day window. That means you have to find that missing $20,000 somewhere else—like your savings account—to make up the difference. You'll eventually get the withheld money back as a refund when you file your taxes, but you have to front the cash now.

This is the single most misunderstood part of a 60-day rollover. If you don't make up that 20% shortfall with your own money, the IRS will treat the withheld amount as a taxable distribution. And if you're under 59½, you'll likely get hit with a 10% early withdrawal penalty on it, too.

The Final Stretch: Depositing Funds and Getting Confirmation

Long before your 60-day deadline, you need to have your new IRA open and ready. Get those funds deposited. Don't even think about waiting until day 59. You need to leave a buffer for any potential processing delays at the new institution.

Remember, the 60-day period is calendar days, not business days. It’s a strict deadline. Miss it, and any money that didn't make it into the new IRA becomes a taxable distribution. On top of paying income tax, you'll probably face that 10% early withdrawal penalty if you're under 59½.

Once the deposit is made, get written confirmation from your new custodian. You need proof that the money was received on time and correctly coded as a rollover. This piece of paper is your best friend. Later, you’ll get two crucial tax forms: a Form 1099-R from the old custodian showing the withdrawal and a Form 5498 from the new custodian showing the deposit. Both are essential for filing your taxes correctly. Our guide on understanding your Form 1099-R can help you decipher this critical document.

Your Essential Rollover Document Checklist

Trying to do this without staying organized is a recipe for disaster. Keep these documents handy.

- Distribution Request Form: The paperwork you sent to your old plan to kick things off.

- Copy of the Distribution Check: A scan or photo of the check you received is a must-have for your records.

- New IRA Application Form: The account opening documents for your new IRA.

- Deposit Confirmation: A receipt or statement from the new institution showing the date and amount of your deposit.

- Form 1099-R: The tax form from your old custodian that reports the distribution.

- Form 5498: The tax form from your new custodian confirming they received your rollover.

By following this timeline and keeping meticulous records, you can navigate the choppy waters of an IRA rollover within 60 days and make sure your retirement funds keep growing without an unexpected tax bill.

Common Rollover Mistakes And How To Avoid Them

Pulling off an IRA rollover within 60 days requires more than just meeting a deadline; you have to navigate a minefield of potential traps. A simple oversight can turn what should be a tax-free move into a costly taxable event. Let's walk through the most common mistakes I see people make and, more importantly, how you can sidestep them completely.

Most of these errors boil down to misunderstandings of the rules. By learning from others' experiences, you can keep your retirement funds safe and ensure your rollover stays tax-free.

Miscalculating The 60 Day Window

This is probably the most frequent—and most costly—error. People hear "60 days" and think business days. The IRS is brutally strict here: it’s 60 calendar days, which includes every single weekend and holiday. The clock starts ticking the day after you receive the funds, not when the check was mailed or dated. Letting that check sit on your desk for a week means you’ve already lost seven precious days.

How to Avoid This:

The second you have that check in hand or see the funds in your account, pull up your calendar. Mark the date you got it, then count out exactly 60 days. That’s your final, absolute deadline. To be even safer, set a few reminders on your phone: one for day 30, another for day 45, and a final alert a week before time is up. This leaves no room for guessing.

I've seen this happen: someone waits until the last minute, only to discover their new bank needs several days to process the deposit. Your best bet is to aim to get the deposit done by day 45 at the latest. That buffer is your safety net against unexpected delays.

Forgetting The 20% Withholding Shortfall

When you move money from an employer plan like a 401(k), the administrator is required by law to withhold 20% for federal taxes. This isn't optional for indirect rollovers from company plans. The mistake comes when you only deposit the 80% you received, not the full 100% that was distributed.

Here’s a real-world example: You decide to roll over $50,000. You’ll get a check for $40,000, and the other $10,000 goes straight to the IRS. To make this a tax-free rollover, you must deposit the entire $50,000 into the new IRA. That means you have to find that missing $10,000 from your own savings to complete the deposit.

How to Avoid This:

Think of the withheld 20% as a short-term loan you’re giving yourself. If you can’t easily cover that shortfall, a direct, trustee-to-trustee rollover is a much better path. With a direct rollover, the money never touches your hands, 100% of your funds go straight to the new account, and there is zero withholding. Problem solved.

Violating The Once Per Year Rule

This rule trips up a lot of people. Since 2015, the IRS only allows one IRA-to-IRA 60-day rollover across all of your IRAs in any rolling 12-month period. It doesn't matter if you have five different IRA accounts; for the purpose of this rule, the IRS sees them as one. People get into trouble thinking the rule applies per account, not per person.

It’s critical to know what this rule covers and what it doesn't:

- It applies to: IRA-to-IRA and Roth IRA-to-Roth IRA rollovers.

- It does not apply to: Rollovers from a 401(k) to an IRA, rollovers from an IRA back to an employer plan, or Roth conversions.

How to Avoid This:

Before you even think about an IRA-to-IRA 60-day rollover, check your records. Have you done another one in the last 365 days? If you need to consolidate funds from multiple IRAs, just use direct trustee-to-trustee transfers. They aren't subject to this limitation, and you can do as many as you need. At Spivak Financial Group, we consistently advise clients that direct transfers are the simplest way to avoid these common yet costly mistakes.

What To Do If You Miss The 60-Day Deadline

That sinking feeling when you realize you’ve blown past the 60-day window for your IRA rollover is awful. It can feel like a costly, irreversible mistake. The good news? It might not be a total loss, but you have to jump on it, and fast. Ignoring the missed deadline triggers some serious and immediate financial pain.

First things first, the IRS no longer sees that money as a rollover. It's immediately reclassified as a taxable distribution. This means the entire amount gets tacked onto your ordinary income for the year. This can easily shove you into a higher tax bracket and leave you with a surprisingly large tax bill.

On top of the income tax hit, if you’re under age 59½, you're almost guaranteed to get slapped with a 10% early withdrawal penalty. That one-two punch of taxes and penalties can vaporize a significant chunk of the retirement funds you were trying to move. This is your signal to start exploring every possible fix right now.

Understanding IRS Waivers For Late Rollovers

Thankfully, the IRS isn't a completely heartless machine. They recognize that life happens and some things are genuinely outside of our control. For these very specific scenarios, they've built a waiver process that can forgive a missed deadline, but you'll need a legitimate, documented reason.

The IRS has a clear list of what they consider valid excuses to qualify for a waiver. These aren't just get-out-of-jail-free cards; they're for situations where finishing the IRA rollover within 60 days was truly impossible.

Some of the most common reasons include:

- Financial Institution Error: The bank or brokerage firm messed up, not you. This is often the strongest argument for a waiver.

- Serious Illness: You were dealing with a severe illness, hospitalization, or a death in your immediate family that made it impossible to handle your finances.

- Postal Error: The check got lost or massively delayed in the mail, and you have proof.

- Incorrect Information: Your financial institution gave you bad advice or wrong information that led to the delay.

- Check Deposited in Error: The funds were mistakenly deposited into an account you couldn't access, and you didn't catch the error in time.

The rules around this have become a bit more forgiving over time. For example, there's now an automatic waiver if a financial institution admits they were entirely at fault. History also shows the IRS can be flexible. One ruling granted a waiver to someone who genuinely misunderstood the rules, got tangled in paperwork, and even had a courier service that was closed on weekends. You can dig into more of these complex 60-day rollover rule cases at TheTaxAdviser.com.

Self-Certification: A Simpler Path To A Waiver

For some of the more straightforward situations, the IRS created a much simpler process called self-certification. This lets you claim a waiver on your own, without getting pre-approval from the IRS, as long as your reason is one of the valid excuses they've listed.

To go this route, you have to complete the rollover as soon as you possibly can after the problem that caused the delay is resolved. Then, you'll provide a written letter to your new IRA custodian certifying that you meet the requirements for a waiver.

Important Note: Self-certification is easier, but it’s not a blank check. The IRS can still audit your tax return and decide your reason wasn't valid, which would retroactively disqualify the rollover. Honesty and good documentation are your best friends here.

When A Private Letter Ruling Is Necessary

What if your situation is messy or doesn't fit neatly into one of the self-certification boxes? Your last resort is to request a Private Letter Ruling (PLR) directly from the IRS. Be warned: this is a formal, slow, and expensive process.

You'll have to submit a formal, detailed request explaining every aspect of your situation, provide a mountain of supporting documents, and pay a hefty user fee that can run into thousands of dollars. After a long wait, the IRS will review your case and issue a formal ruling on whether to grant you the waiver.

This option is really reserved for unique, high-stakes scenarios where self-certification just won't work. Given the complexity, working with an experienced tax professional or a firm like Spivak Financial Group is pretty much essential if a PLR is your only path forward. When you've missed the 60-day deadline, acting quickly and understanding all your options is the key to damage control.

Why Partnering With A Financial Advisor Makes Sense

After walking through the complexities of a 60-day IRA rollover, it’s pretty clear this isn't just about moving money from point A to point B. It’s a high-stakes financial maneuver. One tiny misstep—a missed deadline or a misunderstanding of the withholding rules—can trigger substantial tax penalties that take a bite out of your retirement savings.

The strict deadlines, confusing tax rules, and the unforgiving once-per-year limitation create a minefield for even the most detail-oriented DIY investor.

This is exactly where getting professional guidance can turn a risky process into a secure one. When you go it alone, you're suddenly wearing multiple hats: project manager, compliance officer, and treasurer. An experienced financial advisor steps in as your dedicated guide, eliminating the guesswork and protecting your hard-earned money.

Gaining Clarity and Confidence

An advisor’s first job is to map out a clear, strategic path for you. They’ll look at your specific financial picture to figure out if a 60-day indirect rollover is even the right move. Sometimes, a safer direct trustee-to-trustee transfer is a much better fit. That initial conversation alone can stop a costly mistake before it ever happens.

At Spivak Financial Group, our experts do more than just offer advice. We get in the trenches with you to:

- Handle all the paperwork with both the old and new financial institutions.

- Coordinate the communication between custodians to make sure the transfer is seamless.

- Track every critical deadline so that each step is completed well within the window.

- Create a solid plan for covering the mandatory 20% tax withholding, so you aren't caught off guard.

Choosing to work with an advisor is really an investment in your own peace of mind. It’s about ensuring the funds you've spent a lifetime saving are shielded during a very vulnerable transition. The goal isn't just to move the money—it's to move it correctly, securely, and without any expensive surprises.

A Partner for Your Entire Retirement Journey

Often, the rollover is just one piece of a much bigger retirement puzzle, especially if you’re planning to retire early. A skilled advisor integrates your rollover into your broader financial strategy, which might include specialized income plans like a 72(t) distribution. They make sure every move you make is working together to support your long-term vision.

Choosing the right professional to guide you is a crucial first step. For a detailed breakdown of what to look for, check out our guide on how to choose the right advisor for your unique situation.

To get personalized guidance on your rollover, connect with the experts at Spivak Financial Group by calling (844) 776-3728. Our office is located at 8753 E. Bell Road, Suite #101, Scottsdale, AZ 85260.

Got Rollover Questions? We’ve Got Answers.

Even with the best-laid plans, a 60-day IRA rollover can throw a few curveballs your way. The rules have nuances that can feel tricky, especially when your nest egg is in transit. We get these kinds of specific, nitty-gritty questions all the time from people planning for early retirement.

Think of this as your go-to guide for those "what if" scenarios. Let's dive into some of the most common questions we hear.

Can I Just Roll Over Part of My Account?

Yes, you absolutely can, and it's a common strategy. A partial rollover gives you flexibility.

Let's say you have $200,000 in an old 401(k) but need $20,000 for a short-term cash crunch. You could take out that $20,000 as a distribution. From there, you have a couple of choices. You could use the cash for up to 60 days and then deposit the full $20,000 into your new IRA, completing the rollover tax-free. Or, you could roll over just $15,000 and keep the other $5,000. Just know that the $5,000 you keep becomes a permanent, taxable distribution, likely subject to a 10% early withdrawal penalty.

What if My Rollover Check Gets Lost or Delayed?

This is a nerve-wracking situation, but it happens more often than you'd think. If the check from your old brokerage is lost in the mail or seriously delayed, you might be able to get a waiver from the IRS for missing the 60-day deadline. The key here is proving the delay was due to circumstances reasonably beyond your control.

Expert Tip: The second you suspect a problem, get on the phone with the distributing institution. Ask them to track the check. If it's truly lost, have them issue a stop payment and cut you a new one. Document everything—every call, every email, every person you talk to, and every date. That paper trail is your best defense if you need to ask the IRS for a waiver.

Does the Money Have to Go Into My Checking Account First?

It does. This is one of the defining features of an indirect rollover. When you get the distribution check, it's almost always made out to you personally. You’ll need to deposit it into a personal bank account, like checking or savings, before you can write a new check or initiate a transfer to your new IRA.

This is the very thing that separates a 60-day rollover from a direct one—the money temporarily passes through your hands. Just don't forget that the 60-day clock starts ticking the moment you receive the funds, not when you get around to depositing them. Don't let that cash sit idle in your account for too long.

How Does This Work With an Inherited IRA?

It doesn't. The rules for inherited IRAs are a completely different ballgame and far more restrictive. A non-spouse beneficiary is prohibited from doing a 60-day rollover. It's just not an option. Any money taken out of an inherited IRA can never be put back in.

If a non-spouse beneficiary needs to move those funds, the only approved method is a direct trustee-to-trustee transfer. Trying an indirect, 60-day rollover will trigger a massive tax headache. The entire distribution becomes taxable income, and the money is permanently stripped of its tax-advantaged status. It's a critical distinction that can save you from a costly and irreversible mistake.

Can I Split One Rollover Check Into a Few Different IRAs?

Generally, no. You can't take a single distribution check and chop it up to fund multiple new IRAs. The funds from one distribution are meant to be rolled over into one new retirement account.

If your goal is to spread your retirement money across different accounts or investment firms, there's a much better way to do it. The proper approach is to request multiple direct trustee-to-trustee transfers from the original account. This lets you send specific dollar amounts to as many new accounts as you like, all without the risks and limitations of the 60-day rule. For anyone planning a more complex asset move, it's by far the safer and more efficient route.

Navigating the specifics of an IRA rollover within 60 days requires precision and expertise. At Spivak Financial Group, we help clients manage these complexities every day, ensuring their retirement funds are protected. To unlock consistent income from your retirement savings and explore strategies like a 72(t) SEPP, visit us at 72tprofessor.com.