Let's get right to it. The number every future retiree knows is 59½ years old. This is the magic age when the IRS generally lets you start taking money from your 401(k) without getting hit with an extra 10% early withdrawal penalty.

Think of it as the official green light for accessing the money you’ve worked so hard to save.

Your Roadmap to 401(k) Withdrawal Ages

But here’s the thing: age 59½ is just one stop on a longer journey. Your 401(k) isn't governed by a single rule. It’s a whole system with different milestones that unlock new possibilities—and responsibilities—for your money. Knowing these dates is absolutely critical if you want to make smart financial moves and avoid painful, expensive mistakes.

This guide will walk you through the entire timeline, breaking down the jargon and turning confusing regulations into a clear plan. We'll dig into each age-related rule so you can build a withdrawal strategy that actually fits your life.

Why Do These Age Rules Even Exist?

It all comes down to why 401(k)s were created in the first place. The government offers incredible tax breaks on these accounts—like tax-deferred growth—to encourage us to save for retirement. The age rules are simply the guardrails put in place to make sure the money is used for its intended purpose: funding your later years.

The standard age for penalty-free withdrawals, 59½, is the cornerstone of this system. Before you hit that birthday, any money you pull out is typically subject to that nasty 10% penalty on top of your regular income taxes. This isn't a new concept; it's a long-standing rule that has shaped how millions of Americans plan for their financial future.

You can think of your 401(k) as a vault with a time lock. The main lock is set to spring open on your 59½ birthday. While a few special keys (which we call exceptions) can open it sooner, that specific date is the primary gateway.

To help you get the full picture, here is a quick summary of the key age-related rules that we’ll be exploring in more detail.

Key 401k Withdrawal Age Milestones

| Age Milestone | Withdrawal Type | 10% Penalty Applies? | Key Consideration |

|---|---|---|---|

| Any Age Before 59½ | Early Withdrawal | Yes (usually) | Penalty waived only for specific IRS-approved exceptions. |

| Age 55 | Separation from Service | No (if you leave your job) | Known as the "Rule of 55." Only applies to the 401(k) at your most recent employer. |

| Age 59½ | Standard Withdrawal | No | This is the standard age for penalty-free access to all retirement funds. |

| Age 73+ | Required Minimum Distribution (RMD) | No (but penalties for not taking it!) | The IRS mandates you start taking withdrawals to ensure taxes are eventually paid. |

This table gives you a high-level overview, but as you can see, there’s more to it than just one number. Each of these milestones has its own set of rules you need to understand.

Key Milestones to Know

Navigating your 401(k) journey means knowing more than just the finish line. There are several important age thresholds that can dramatically impact your financial strategy long before—and long after—you officially retire.

To give you a clear map, we’ll be covering a few of the most important milestones and what they mean for your money, including:

- The Rule of 55: A fantastic exception that lets people who leave their job in the year they turn 55 (or later) tap their 401(k) early.

- Age 59½: The universal age for penalty-free access, no matter your employment status.

- Required Minimum Distributions (RMDs): The point where the IRS says, "Okay, it's time to start taking that money out and paying taxes on it."

Of course, knowing when you can take money out is only half the battle. You also need to understand the mechanics of how to do it. For a detailed breakdown of the logistics, you can check out our other guide on how to take money from a 401k. This article will build on that by focusing squarely on the timeline and the "why" behind each rule.

Unlocking Your 401(k): The Magic Age of 59½

For anyone with a 401(k), the age 59½ is more than just a number—it’s a major milestone on the road to retirement. This is the age when the IRS officially gives you the keys to your savings, letting you access your money without that painful 10% early withdrawal penalty. It’s the moment the game changes in your favor.

Think of it this way: your 401(k) has been in a vault with a time lock, steadily growing for decades. That lock is set to click open on your 59½ birthday. Suddenly, you have the freedom to take money out for any reason at all—whether it’s to fund your retirement, buy that boat you’ve been dreaming of, or just have extra cash on hand.

This newfound flexibility is a big deal. Before this age, you generally need a specific, IRS-approved reason to touch that money without getting hit with a penalty. But after 59½, the "why" doesn't matter anymore, at least not when it comes to penalties. You’ve met the main requirement.

Penalties vs. Taxes: A Critical Distinction

Here’s where things can get tricky, and it’s a point of confusion that has cost people a lot of money. While the 10% early withdrawal penalty vanishes at age 59½, your tax obligation absolutely does not.

Any money you pull from a traditional, pre-tax 401(k) is treated as ordinary income by the IRS. That means it gets added to your total income for the year and is taxed just like your salary would be.

Let’s walk through a quick example:

- You're 60 years old and decide to pull $20,000 from your 401(k).

- Penalty? None. You’re over 59½, so you pay $0 in penalties.

- Taxes? That $20,000 gets added to your income for the year. If you fall into the 22% federal tax bracket, you're looking at a $4,400 federal tax bill on that withdrawal, not including any state taxes you might owe.

This is exactly why you need a plan. A single large withdrawal can easily bump you into a higher tax bracket, meaning a bigger chunk of your hard-earned savings goes straight to Uncle Sam than you ever expected.

Here's the bottom line: Age 59½ gets rid of the penalty, but it doesn't get rid of the tax. Every dollar you withdraw from a traditional 401(k) is taxable, so you have to be ready for that bill.

It's Not Just If You Can Withdraw, but When You Should

Once you've passed the 59½ milestone, the big question shifts. It's no longer about what age you can take money out, but about when you should. You're finally in the driver's seat, and the choices you make now will directly affect how long your retirement savings last.

The goal is to create an income stream that's as tax-efficient as possible. This means being strategic about how much you take out each year to cover your living expenses without sending your tax bill through the roof.

Here are a few things to think about:

- Other Income: Are you still working part-time? Will you have Social Security or a pension coming in? Your 401(k) withdrawals are stacked right on top of that other income, so you'll need to manage the total to stay in a comfortable tax bracket.

- Your Budget: The bedrock of any good withdrawal strategy is knowing how much you actually need to live on. Don't take out more than you need—you’ll just end up paying unnecessary taxes on it.

- Big-Ticket Goals: Thinking about a major purchase, like an RV or a down payment on a vacation home? It might be much smarter to spread that withdrawal over two or three years instead of taking it all at once to minimize the tax hit.

Getting a handle on these moving parts is essential. While turning 59½ gives you access, smart, thoughtful planning is what lets you keep more of your money working for you deep into your retirement years.

How to Access Your 401k Before Age 59½

Let's be honest: life rarely follows the neat timeline laid out in a retirement brochure. A sudden job loss, a medical emergency, or any number of unexpected events can create an urgent need for cash long before you hit that magic retirement age of 59½.

While the 10% early withdrawal penalty is designed to keep you from raiding your nest egg, it’s not an iron-clad rule. The IRS has carved out several specific exceptions that act like safety valves for life's most challenging moments. Knowing what they are can give you real options when you need them most.

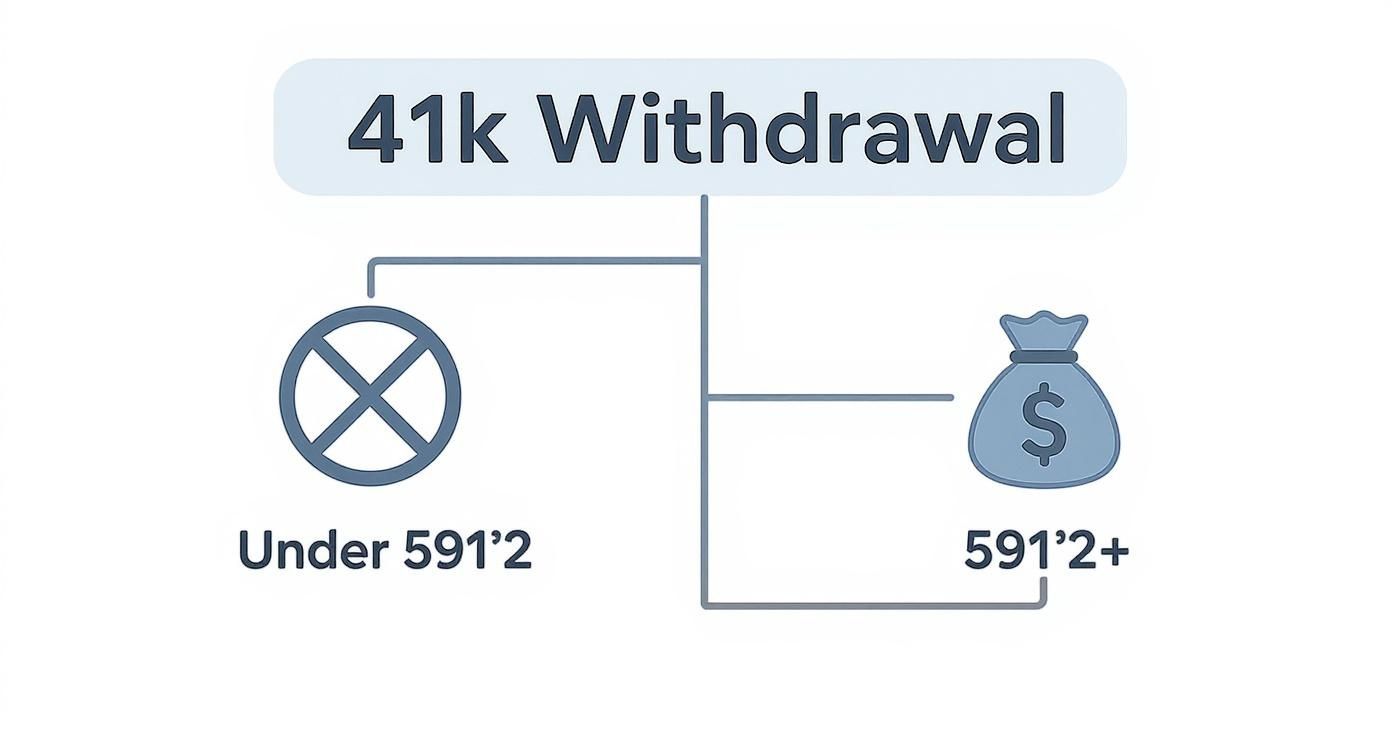

This diagram gives a simple, high-level look at the main fork in the road for 401(k) withdrawals.

As you can see, 59½ is the standard for penalty-free access, but there are legitimate pathways to get to your money earlier.

The Rule of 55 for Early Retirees

One of the most powerful—and often misunderstood—exceptions is the Rule of 55. For anyone planning an early retirement or facing a late-career layoff, this rule can be a complete game-changer.

Here's the deal: if you leave your job for any reason (quit, get laid off, or retire) during or after the calendar year you turn 55, you can start taking distributions from that specific employer’s 401(k) plan without the 10% penalty.

Think about Sarah, who gets laid off in March. Her 55th birthday isn't until August. Because she separated from her employer in the same calendar year she turns 55, she can immediately start tapping into that 401(k) penalty-free.

But there’s a catch. This rule only applies to the 401(k) from the job she just left. Any money in old 401(k)s or IRAs is still locked up until 59½ unless another exception applies.

Exceptions for Major Life Events

Life throws curveballs, and the tax code acknowledges that. Beyond the Rule of 55, the IRS allows for penalty-free withdrawals to help you navigate some of life’s biggest financial hurdles.

Keep in mind, you will still owe ordinary income tax on every dollar you take out. The exception just saves you from the extra 10% hit.

To give you a clearer picture, here are some of the most common situations where the penalty is waived.

Common 401k Early Withdrawal Exceptions (Penalty-Free)

| Exception | Who It's For | Key Requirement |

|---|---|---|

| Total & Permanent Disability | Individuals who can no longer work due to a physical or mental condition. | You must provide proof from a physician that you cannot perform any "substantial gainful activity." |

| Unreimbursed Medical Bills | Anyone with significant medical expenses not covered by insurance. | You can only withdraw the amount of your expenses that exceeds 7.5% of your adjusted gross income (AGI). |

| Qualified Domestic Relations Order (QDRO) | Individuals going through a divorce or legal separation. | A court must issue a QDRO to divide the 401(k) assets between spouses or for child support. |

| Death of the Account Holder | Beneficiaries inheriting a 401(k) plan. | The 10% penalty is waived for distributions to beneficiaries after the account owner's death. |

These are some of the most frequent scenarios, but they aren't the only ones. We cover the complete list in our detailed guide on the 10 early withdrawal penalty exceptions. Understanding all of your options is the first step.

Understanding the Process and Requirements

Claiming one of these exceptions isn't as simple as checking a box. The burden of proof is entirely on you, the taxpayer.

For instance, if you're taking a distribution for medical expenses, you need to keep meticulous records of your bills and carefully calculate exactly how much you can withdraw penalty-free. It's not a free-for-all.

Every 401(k) plan administrator will have its own paperwork and procedures for this. Your first move should be to call your plan provider to understand exactly what they need from you. If you don't follow their process to the letter, they might code the withdrawal incorrectly, and you could find yourself fighting the IRS over a penalty you shouldn't have owed.

Using a 72(t) SEPP for Early Retirement Income

The Rule of 55 is a great way to tap your 401(k) without penalties, but it has one major string attached: you have to leave your job. What if you need income years earlier, say in your 40s or early 50s, while you pivot to a new career or finally launch that passion project?

This is where a powerful—but admittedly complex—strategy called a 72(t) distribution enters the picture.

Officially known as Substantially Equal Periodic Payments (SEPP), a 72(t) plan lets you take a series of calculated withdrawals from your retirement account at any age without that nasty 10% early withdrawal penalty. Think of it as creating your own private pension. It’s a way to turn a lump sum of savings into a predictable, recurring payment that can bridge the financial gap until you hit age 59½.

This strategy is a lifesaver for people who saved diligently and find themselves able to retire early but need a reliable way to cover living expenses. It provides a structured path to your money when other exceptions just don’t fit.

How a SEPP Plan Works

Unlike a one-off hardship withdrawal, a SEPP is a serious commitment. You're not just taking out a single chunk of cash; you're kicking off a methodical series of payments that you absolutely must stick with for a specific period. The IRS is famously strict about this.

Here’s the core rule: you must continue taking these payments for whichever of these two periods is longer:

- A minimum of five full years.

- Until you reach age 59½.

Let's make that real. If you start a SEPP at age 52, you're locked in until you're 59½—that's seven and a half years of payments. But if you start at age 58, you have to continue until you're 63 to meet the five full years requirement, even though you’ve already passed the standard retirement age.

Don't take this commitment lightly. If you break the rules—by changing the payment amount or stopping the plan early—the IRS can retroactively slap the 10% early withdrawal penalty on every single dollar you've taken out since day one, plus interest. It’s a costly mistake.

Calculating Your SEPP Payments

The IRS doesn’t just let you pull out whatever amount you feel like. The "substantially equal" part of the name is key. Your payment amount has to be figured out using one of three specific, IRS-approved methods. Each formula uses your account balance, your life expectancy, and a reasonable interest rate to land on your annual distribution amount.

- Required Minimum Distribution (RMD) Method: This is the most straightforward calculation. It simply divides your account balance by a life expectancy factor from an IRS table. This approach gives you the lowest annual payment, and the amount gets recalculated each year.

- Amortization Method: This method works a lot like a mortgage, calculating a fixed annual payment by spreading your account balance over your life expectancy. It usually produces a higher, more consistent payment.

- Annuitization Method: This one uses an annuity factor from the IRS to set your annual payment. The amount is fixed and typically lands somewhere between what the RMD and amortization methods would give you.

Choosing the right method is critical. One might give you exactly the income you need, while another could leave you short. To really get into the weeds of how these formulas work, you can explore the details of the Substantially Equal Periodic Payments rules and see the nuances for yourself.

Is a 72(t) SEPP Right for You?

A SEPP isn't a casual decision. It’s a long-term financial strategy that demands absolute precision and careful planning. It’s best for people who have a crystal-clear picture of their income needs and are confident they can stick to the rigid payment schedule. For early retirees who have done their homework, it's a fantastic tool.

But it is absolutely not a flexible source of emergency cash. The second you start a SEPP, you lose the ability to tweak your withdrawals based on a market downturn or a sudden life change without risking those huge penalties.

Because the rules are so unforgiving and the math has to be perfect, this is one area where professional help isn’t just a good idea—it's essential. One small mistake in the setup or execution can be incredibly expensive. Working with a specialist who lives and breathes these complex strategies ensures your plan is compliant from the get-go and built to meet your specific income needs without running afoul of the IRS.

Navigating Required Minimum Distributions (RMDs)

Just when you think you have complete control over your 401(k), the government shows up with a rule you simply can’t ignore. It’s called the Required Minimum Distribution, or RMD for short. This is the point where the IRS officially requires you to start taking money out of your tax-deferred retirement accounts, including your 401(k).

Think of it like this: for decades, your investments have been growing in a tax-sheltered bubble. The RMD is the government’s way of finally collecting the taxes it patiently deferred all those years. This isn’t a friendly suggestion—it’s a mandate with some pretty serious consequences if you overlook it.

This shift marks a whole new phase in your financial life. You’re moving from the accumulation years into a period of planned, mandatory withdrawals. Getting a handle on the RMD age and how the math works is crucial for staying on the right side of the IRS and managing your retirement income effectively.

When Do RMDs Begin?

The starting age for your first RMD has changed a few times in recent years, so it pays to stay current. As of 2023, the RMD age was bumped up from 72 to 73 for anyone who turns 72 on or after January 1, 2023. You can dive deeper into retirement savings data with Kiplinger’s analysis of 401k balances.

You must take your very first RMD by April 1 of the year after you hit age 73. But here’s the catch: every RMD after that is due by December 31 of each year. If you put off that first withdrawal until the following April, you'll end up taking two RMDs in a single tax year, which could easily push you into a higher tax bracket.

Calculating Your RMD Amount

The amount you have to take out isn’t just a random number; it’s calculated with a straightforward formula from the IRS.

It comes down to two key pieces of information:

- Your Account Balance: This is the total value of your 401(k) on December 31 of the previous year.

- A Life Expectancy Factor: The IRS provides a Uniform Lifetime Table that assigns a "distribution period" based on your age.

You simply divide your prior year-end account balance by that life expectancy factor. That’s your RMD for the year. Your plan administrator can usually help you run the numbers.

The Penalty for Missing an RMD Is Severe

If you fail to withdraw the full RMD amount by the deadline, the penalty is one of the steepest in the entire tax code. The IRS can hit you with a 25% excise tax on the amount you should have withdrawn but didn't. This is a very expensive mistake to make, and it’s designed to make sure everyone complies.

Planning for RMDs in Your Strategy

RMDs shouldn’t be a surprise you dread. They should be a planned part of your overall retirement income strategy. Since these distributions are taxed as ordinary income, they will definitely affect your tax bill.

A little strategic planning goes a long way. For instance, think about how your RMDs will stack up with other income sources like Social Security or a pension. By anticipating this mandatory income, you can better manage your tax bracket and keep your financial plan on a steady, predictable course through your later retirement years.

Putting It All Together: Your Personal 401(k) Withdrawal Plan

Knowing the rules is one thing, but actually applying them to your life is where the rubber meets the road. It’s time to shift from theory to action and start mapping out a 401(k) withdrawal strategy that truly fits your goals.

This isn’t just about crunching numbers. It’s about getting crystal clear on what you want your retirement to look like, figuring out what that lifestyle will realistically cost, and being smart about your taxes. The end goal is to build a reliable, tax-efficient income stream you can count on for decades.

Key Questions to Guide Your Strategy

Before you touch a dime, you need to sit down and answer some foundational questions. Your honest answers here will become the blueprint for your entire plan.

- What’s my target retirement date? Nailing down your ideal date tells you which withdrawal rules will even apply to you in the first place.

- How much income will I actually need each year? This is non-negotiable. A detailed budget is the only way to know how much you’ll need to pull from your accounts.

- What other money will be coming in? Don’t forget to account for Social Security, a pension, or even part-time work. These all affect your overall tax bracket.

- What are my big-ticket retirement goals? Planning ahead for major expenses like that round-the-world trip or a kitchen remodel can prevent you from taking a huge, costly withdrawal down the line.

Why You Shouldn't Go It Alone

Trying to navigate all these complexities by yourself is incredibly risky. One small miscalculation or a simple misunderstanding of an IRS rule can trigger massive tax bills and penalties, potentially putting your entire financial future in jeopardy. This is especially true when you get into more specialized strategies that demand flawless execution.

A 72(t) SEPP, for example, is a fantastic tool for generating penalty-free income early on, but the rules are notoriously unforgiving. A single mistake can blow up the whole plan, triggering retroactive penalties on every single distribution you've already taken.

This is exactly why getting professional guidance is so important. An expert can look at your complete financial picture, help you weigh the pros and cons of every option, and build a compliant plan that’s tailored to your life. For something as intricate as a 72(t) SEPP, the expertise of a firm like Spivak Financial Group is invaluable. We make sure your plan not only achieves your goals but also follows every last IRS regulation to the letter, giving you true confidence and peace of mind.

Got Questions About 401(k) Withdrawals? We've Got Answers.

When it comes to tapping into your 401(k), the big-picture rules are one thing, but it’s the specific, real-life scenarios that often leave people scratching their heads. Let's tackle some of the most common questions that come up.

Can I Withdraw From My 401(k) if I Am Still Working?

Yes, you often can, but there are some big "ifs" involved. Once you hit age 59½, many plans offer what's known as an "in-service" withdrawal. This lets you access your money without the early withdrawal penalty, though you'll still owe regular income tax on the amount you take out.

If you haven't reached that magic age yet, your options are much more limited. You generally can't just take money out while you're still with your employer unless you're facing a specific, documented hardship or decide to take out a 401(k) loan. Every single plan has its own set of rules, so your first step should always be to check your Summary Plan Description (SPD) or give your plan administrator a call.

What Happens if I Withdraw From a 401(k) From a Previous Employer?

An old 401(k) you left behind at a former job is treated almost exactly like your current one by the IRS. If you're over 59½, you can take distributions penalty-free, but they'll be taxed. If you're younger, that dreaded 10% early withdrawal penalty will apply unless you qualify for one of the specific exceptions.

Here's a critical detail that trips a lot of people up: the Rule of 55 only works for the 401(k) at the company you leave in or after the year you turn 55. It absolutely does not apply to old 401(k)s from previous jobs. This is a major reason why many people choose to roll over old 401(k)s into a single IRA—it simplifies the rules and your life.

Do I Pay Taxes on a 401(k) Loan?

No, not as long as you play by the rules. A 401(k) loan isn't considered a taxable event because you're technically borrowing from yourself and paying yourself back. As long as you stick to the repayment schedule, the IRS stays out of it.

The danger comes if you leave your job—whether you quit, get laid off, or retire—before the loan is paid off. At that point, the entire outstanding balance is often reclassified as a distribution. If you’re under 59½, not only will you owe income tax on the full amount, but you'll get hit with the 10% penalty, too. A seemingly simple loan can quickly turn into a very expensive headache, so think carefully about your job stability before you take one out.

Navigating the complexities of 401(k) withdrawals, especially for early retirement, requires precision and expertise. At Spivak Financial Group, we specialize in creating compliant, penalty-free income strategies to help you reach your goals sooner.

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

Learn how we can help at https://72tprofessor.com.