Retiring early is a common dream, but a major obstacle stands in the way for most: accessing retirement funds before age 59½ without incurring a stiff 10% penalty from the IRS. This penalty can significantly erode a nest egg, making early financial independence feel out of reach. However, a well-planned approach can make all the difference. The key is understanding the specific exceptions and frameworks the tax code provides for precisely this scenario. These aren't loopholes; they are established early retirement withdrawal strategies designed for those who have diligently saved and planned for a non-traditional retirement timeline.

Successfully funding an early retirement requires a dual focus: accumulating sufficient savings and creating a compliant plan to access those funds. As you navigate the path to financial freedom, remember that effective saving is the foundation, and you can explore various proven money-saving strategies to build your nest egg. Once that foundation is solid, the next crucial step is designing a withdrawal plan.

This guide moves beyond generic advice to provide a detailed roadmap for seven distinct and powerful early withdrawal methods. We will break down the mechanics, eligibility requirements, pros, and cons of each strategy, from the structured payments of a 72(t) SEPP plan to the long-term flexibility of a Roth conversion ladder. Our goal is to provide clear, actionable insights so you can confidently select and implement the approach that best aligns with your financial goals and desired lifestyle, turning your early retirement vision into a reality. For personalized guidance on complex financial decisions, consider contacting the experts at Spivak Financial Group.

1. Rule of 72(t) – Substantially Equal Periodic Payments

For early retirees, the prospect of accessing retirement funds before age 59.5 often comes with a significant roadblock: the 10% early withdrawal penalty. However, IRS Section 72(t), often called the Substantially Equal Periodic Payments (SEPP) rule, provides a valuable exception. This rule is one of the most structured early retirement withdrawal strategies, allowing you to take penalty-free distributions from your IRA, 401(k), or other qualified retirement plans.

How Does Rule 72(t) Work?

The core principle of a SEPP is to establish a series of withdrawals based on your life expectancy. You must commit to taking these payments for a minimum of five full years or until you reach age 59.5, whichever period is longer. Once you begin a 72(t) distribution schedule, you cannot modify it without incurring substantial penalties, retroactively applied to all previous withdrawals.

The annual withdrawal amount is not arbitrary; it must be calculated using one of three IRS-approved methods:

- Required Minimum Distribution (RMD) Method: This is the simplest calculation, dividing your account balance by your life expectancy factor from IRS tables. The payment amount recalculates annually, making it variable.

- Fixed Amortization Method: This method calculates a fixed annual payment by amortizing your account balance over your life expectancy using a reasonable interest rate. The payment remains the same each year.

- Fixed Annuitization Method: This method uses an annuity factor to determine a fixed annual payment, which also remains consistent throughout the distribution period.

Practical Implementation and Examples

Let’s consider a practical scenario. A 45-year-old with a $500,000 401(k) needs to generate income. Using the fixed amortization method with an approved interest rate, they might calculate an annual distribution of approximately $25,000. They would need to withdraw this exact amount each year until they are at least 59.5.

A common strategy is to avoid applying the 72(t) rule to your entire nest egg. Instead, you can roll over a portion of your 401(k) into a separate IRA and apply the SEPP only to that specific account. This preserves the flexibility of your remaining funds while generating the necessary income.

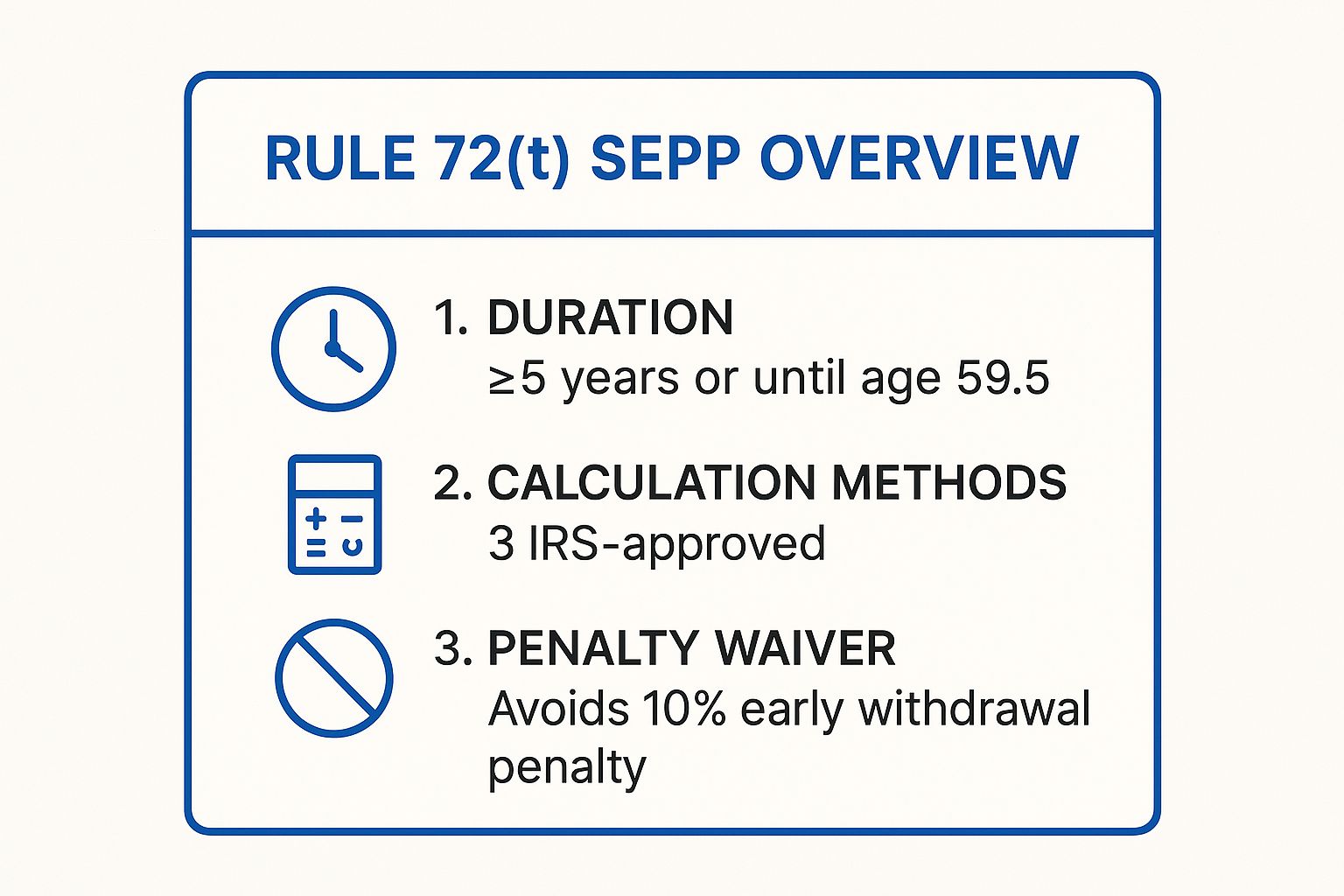

The following infographic provides a high-level overview of the SEPP plan's core components.

This quick reference highlights the essential commitments and benefits of using a SEPP strategy, emphasizing the strict duration and calculation rules required to waive the penalty.

Is This Strategy Right for You?

The Rule of 72(t) is ideal for those who need a predictable, fixed income stream and are confident they won't need to alter the payment amount. However, its rigidity is also its biggest drawback. An unexpected expense or change in financial needs could make the fixed payments problematic.

Key Insight: The inflexibility of the 72(t) rule is why many financial advisors, like those at Spivak Financial Group, recommend applying it to only a portion of your assets. This creates the income you need without locking up your entire retirement portfolio.

Before committing, it is crucial to calculate your potential payments using all three methods to see which best aligns with your financial needs. Professional guidance is highly recommended to ensure compliance and avoid costly errors. Resources like 72tProfessor.com can assist with these complex calculations, but consulting a qualified financial professional is the best first step.

2. Roth IRA Ladder

For those planning to retire years before 59.5, the Roth IRA conversion ladder has become one of the most powerful and flexible early retirement withdrawal strategies. Popularized by the Financial Independence, Retire Early (FIRE) movement and blogs like Mad Fientist, this strategy allows you to systematically access pre-tax retirement funds, like those in a traditional IRA or 401(k), without incurring the 10% early withdrawal penalty.

The strategy works by converting a portion of your traditional retirement funds into a Roth IRA each year. When you make a conversion, you pay ordinary income tax on the converted amount in that year. However, once the funds are in the Roth IRA, they grow tax-free. The crucial element is the IRS's five-year rule: each conversion amount must season for five years before it can be withdrawn tax and penalty-free. By creating a "ladder" of conversions, you establish a pipeline of accessible funds for your future self.

This visual shows how consistent annual conversions build a source of income that becomes available after the initial five-year waiting period, creating a steady, penalty-free cash flow.

How Does a Roth IRA Ladder Work?

The core principle is to strategically time your conversions and withdrawals. You are essentially pre-paying the income tax on your retirement funds during your early retirement years when your income (and thus your tax bracket) is likely to be lower. After the five-year clock on a specific conversion has passed, you can withdraw that principal amount.

The process involves a few key steps:

- Step 1 – Annual Conversion: Each year, you convert a specific amount from your traditional IRA or 401(k) to a Roth IRA. You will owe income taxes on this amount for the year of the conversion.

- Step 2 – The Five-Year Wait: A unique five-year clock starts for each individual conversion. For example, a conversion made in 2024 can be withdrawn starting in 2029.

- Step 3 – Penalty-Free Withdrawal: After the five-year period is complete, you can withdraw the converted principal without taxes or penalties, regardless of your age.

Practical Implementation and Examples

Imagine a 45-year-old who plans to retire at age 50. To fund their first year of retirement, they would need to start their first conversion at age 45. If they need $50,000 per year, they would convert $50,000 in year one (age 45), another $50,000 in year two (age 46), and so on.

When they turn 50, the first $50,000 conversion from age 45 will have met its five-year requirement, and they can withdraw it. At age 51, the second conversion becomes available. This creates a rolling source of income. It's crucial to have other funds (like savings or a brokerage account) to live on during the initial five-year waiting period.

Is This Strategy Right for You?

The Roth IRA ladder is ideal for early retirees who can plan at least five years in advance and have a way to cover living expenses while the ladder is being built. Its primary advantage is flexibility; unlike the 72(t) rule, you are not locked into a fixed withdrawal amount. You can convert different amounts each year based on your tax situation and withdraw funds as needed once they are seasoned.

Key Insight: The Roth IRA ladder's brilliance lies in tax planning. At Spivak Financial Group, we often advise clients to execute conversions strategically during low-income years to fill up lower tax brackets, minimizing the overall tax paid on their retirement savings.

The main drawback is the required foresight and the need for a five-year bridge fund. Any miscalculation in timing or an unexpected need for funds before a conversion matures can disrupt the plan. Careful tracking of each conversion's five-year timeline is essential, and consulting with a financial professional can help ensure you execute the strategy correctly to avoid costly tax mistakes.

3. Bridge Strategy

For many aspiring early retirees, the primary challenge is accessing funds to cover living expenses in the years leading up to age 59.5 without triggering penalties on their retirement accounts. The Bridge Strategy is a foundational approach designed to solve this exact problem. As one of the most flexible early retirement withdrawal strategies, it involves using non-retirement, taxable brokerage accounts to "bridge" the financial gap until your 401(k)s and IRAs are fully accessible.

How Does the Bridge Strategy Work?

The concept is straightforward: while you are working, you aggressively save in both tax-advantaged retirement accounts (like a 401(k) and Roth IRA) and a standard taxable brokerage account. The funds in the taxable account are specifically earmarked to cover your living expenses from your early retirement date until you turn 59.5. This allows your tax-advantaged accounts to continue growing untouched and penalty-free.

The key to a successful bridge account is managing taxes effectively. Withdrawals from a taxable account are not penalty-free, but they are often taxed more favorably than early retirement account distributions. Your withdrawals will primarily consist of:

- Principal (Contributions): The money you initially invested, which is withdrawn tax-free.

- Long-Term Capital Gains: Profits on investments held for more than one year, which are taxed at preferential rates (0%, 15%, or 20%), often much lower than ordinary income tax rates.

Practical Implementation and Examples

Let’s imagine an individual who plans to retire at age 50 and needs $50,000 per year to live on. They plan to tap their 401(k) at age 60. They need a 10-year bridge. To implement this strategy, they would aim to accumulate at least $500,000 in a taxable brokerage account by age 50. During their early retirement years, they would sell assets from this account to generate their required income.

To minimize the tax impact, they can employ several tactics:

- Tax-Loss Harvesting: Selling investments at a loss to offset capital gains, potentially reducing their tax liability to zero in some years.

- Asset Location: Holding tax-inefficient assets (like corporate bonds) in tax-advantaged accounts, while placing tax-efficient investments (like index funds or ETFs) in the taxable bridge account.

This strategy requires meticulous planning during your working years, a concept explored in guides on planning for early retirement.

Is This Strategy Right for You?

The Bridge Strategy is perfect for disciplined savers who want maximum flexibility in their early retirement. Unlike a 72(t) SEPP, there are no rigid withdrawal rules, amounts, or timelines. You can withdraw as much or as little as you need, whenever you need it. This adaptability is invaluable for handling unexpected expenses or fluctuating income needs.

The primary downside is the tax complexity and the potential "tax drag" on investment growth in the taxable account during your accumulation years. You also need the financial discipline to build a substantial taxable account alongside your regular retirement savings.

Key Insight: The Bridge Strategy offers unparalleled freedom but demands careful tax management. Professionals at Spivak Financial Group often emphasize that optimizing asset location and consistently harvesting tax losses are non-negotiable for making a bridge account last until 59.5.

This approach is a cornerstone of the Financial Independence, Retire Early (FIRE) movement and is often used in combination with other methods, like a Roth Conversion Ladder, for a multi-layered and robust early retirement income plan.

4. Cash Cushion Strategy

For early retirees, one of the greatest fears is a market crash occurring just as they begin drawing down their portfolio. Selling investments during a downturn can permanently damage a nest egg's long-term viability. The Cash Cushion Strategy is a conservative but effective approach among early retirement withdrawal strategies, designed specifically to mitigate this risk by providing a buffer against market volatility.

How Does the Cash Cushion Strategy Work?

The core principle is to set aside a significant amount of cash or cash equivalents to cover living expenses for a predetermined period, typically three to five years. This "cushion" allows you to pay your bills without being forced to sell stocks or other growth assets when their values are depressed. You live off the cash during bear markets and replenish it from your investment gains during bull markets.

This method, often advocated by conservative financial advisors like William Bernstein, provides crucial flexibility and peace of mind. It separates your short-term spending needs from your long-term investment growth, allowing your portfolio the time it needs to recover from downturns. The key elements include:

- Determining the Cushion Size: Calculate your essential annual living expenses and multiply that by the number of years you want the cushion to last (e.g., $40,000/year x 5 years = $200,000 cushion).

- Holding the Cushion: Keep these funds in highly liquid, safe accounts like high-yield savings accounts, money market funds, or short-term bond ETFs.

- Systematic Replenishment: During strong market years, sell appreciated assets to refill the cash cushion back to its target level. During down years, you simply draw from the cash and leave your investments untouched.

Practical Implementation and Examples

Let’s consider a retiree with a $1 million portfolio who needs $40,000 per year. They decide to create a five-year cash cushion of $200,000, leaving the remaining $800,000 invested. If the market drops 20% in their first year of retirement, they can confidently draw their $40,000 from the cash account, giving their portfolio a full year to start its recovery without any forced sales.

Once the market recovers and their portfolio grows, they can sell a portion of their gains to bring the cash cushion back up to the $200,000 mark. This disciplined approach of "sell high, live off cash low" is fundamental to the strategy's success. It’s a powerful way to manage sequence-of-return risk, which is the danger of poor market returns in the early years of retirement.

Is This Strategy Right for You?

The Cash Cushion Strategy is ideal for risk-averse early retirees who prioritize stability and are willing to potentially sacrifice some long-term returns for a greater sense of security. The main drawback is the "cash drag," as the large cash position may not keep pace with inflation and will likely underperform a fully invested portfolio over the long term.

Key Insight: Building a substantial cash reserve is a defensive maneuver that provides immense psychological comfort. At Spivak Financial Group, we often see clients use this strategy to sleep better at night, knowing they have a plan to weather any market storm without derailing their retirement.

This strategy demands discipline. You must resist the temptation to spend the cushion during good times or to invest it when you see markets roaring. It requires a clear plan for when and how to replenish the funds. For those exploring various ways to fund early retirement, understanding all your options, including how to access 401(k) funds without penalty on 72tprofessor.com, can provide a more complete picture of your financial toolkit.

5. Bond Ladder Strategy

For early retirees navigating the years before they can access traditional retirement accounts penalty-free, creating a predictable and stable income stream is paramount. The bond ladder is one of the most effective early retirement withdrawal strategies for achieving this goal. This approach involves purchasing multiple bonds with staggered maturity dates, ensuring a steady flow of cash as each bond matures, which can cover living expenses without touching your equity portfolio.

How Does a Bond Ladder Work?

The core principle of a bond ladder is to spread your investment across several bonds that mature in different years. For example, instead of investing $100,000 into a single 10-year bond, you would invest $10,000 each into bonds that mature in one, two, three, and so on, up to ten years. As each bond matures, you receive your principal back, plus interest, providing predictable cash flow.

This structure offers several key advantages:

- Predictable Income: You know exactly when and how much money you will receive as each "rung" of the ladder matures.

- Reduced Interest Rate Risk: By staggering maturities, you are not locked into a single interest rate. As bonds mature, you can reinvest the proceeds at current market rates if needed, or use the cash for expenses.

- Capital Preservation: High-quality bonds, such as U.S. Treasuries, are considered very safe investments, making them ideal for preserving capital needed in the short term.

Practical Implementation and Examples

Let's imagine an early retiree needs $40,000 per year for living expenses for the first decade of retirement. They could build a 10-year bond ladder by purchasing a series of high-quality bonds or Certificates of Deposit (CDs). They would buy a $40,000 bond that matures in one year, another that matures in two years, and so on, for ten years. Each year, a bond matures, providing the necessary $40,000.

A popular variation is to use Treasury I-Bonds for the initial rungs of the ladder. I-Bonds offer protection against inflation, which is a major concern in the early years of retirement. This ensures your planned income keeps pace with the rising cost of living.

Is This Strategy Right for You?

The bond ladder strategy is perfect for risk-averse early retirees who need a reliable income bridge to cover the period before age 59.5 or before Social Security begins. It provides a "sleep-at-night" factor by separating the funds you need for near-term expenses from your long-term growth assets, like stocks. This allows your equity portfolio to grow without the pressure of needing to sell shares during a market downturn.

Key Insight: A bond ladder acts as a financial shock absorber. The team at Spivak Financial Group often designs them to cover the first 5-10 years of retirement, giving the retiree's stock portfolio the valuable time it needs to compound without the need for premature withdrawals.

However, the trade-off is potentially lower returns compared to an all-equity portfolio. Therefore, this strategy is best used as a component of a broader retirement plan rather than as a total portfolio solution. It is crucial to select high-quality bonds to minimize default risk and ensure your income stream is secure.

6. Bucket Strategy

Navigating market volatility while drawing down your nest egg is one of the biggest challenges for early retirees. The bucket strategy is a powerful mental and practical framework designed to manage this risk. This approach is one of the most intuitive early retirement withdrawal strategies, as it segments your portfolio into different "buckets" based on when you'll need the money, providing a clear structure for your withdrawals.

The core idea, popularized by financial planners like Harold Evensky and Christine Benz, is to align your investments with your time horizon. Instead of viewing your portfolio as one large sum, you divide it into multiple accounts, each with a specific purpose and risk level. This mental separation helps you weather market downturns without panic-selling long-term assets to cover short-term expenses.

How Does the Bucket Strategy Work?

The strategy typically involves creating three distinct buckets, although the number can be adapted to your personal needs. Each bucket corresponds to a different time frame and holds assets appropriate for that period.

- Bucket 1 (Short-Term): This is your cash and near-cash bucket, designed to cover living expenses for the next 1-3 years. It holds highly liquid, low-risk assets like savings accounts, money market funds, and short-term bonds. This is the bucket you draw from for your regular income.

- Bucket 2 (Mid-Term): This bucket is intended to refill Bucket 1 and is invested for a 3-7 year time horizon. It contains a balanced mix of assets, such as high-quality bonds and conservative stocks, aiming for modest growth while managing risk.

- Bucket 3 (Long-Term): This is your growth engine, holding assets you won't need for 7+ years. It's invested primarily in stocks and other growth-oriented investments, designed to outpace inflation and ensure the longevity of your portfolio.

Practical Implementation and Examples

Imagine an early retiree needs $60,000 per year. Their bucket setup might look like this:

- Bucket 1: Contains $120,000 (2 years of expenses) in a high-yield savings account.

- Bucket 2: Holds $300,000 (the next 5 years of expenses) in a balanced 50/50 stock and bond portfolio.

- Bucket 3: The remainder of the portfolio is invested in a diversified stock index fund for long-term growth.

The retiree draws their annual $60,000 from Bucket 1. Annually, or when market conditions are favorable, they sell assets from Bucket 2 to replenish Bucket 1. During strong bull markets, they would sell appreciated assets from Bucket 3 to refill Bucket 2. This systematic process prevents the need to sell stocks during a market downturn to pay for immediate bills.

Is This Strategy Right for You?

The bucket strategy is excellent for retirees who feel anxious about market fluctuations and want a clear, logical system for managing withdrawals. It provides a psychological buffer, allowing your long-term investments to grow without being disturbed by short-term income needs.

However, it can be slightly more complex to manage than a simple total-return approach and requires disciplined rebalancing. You must establish clear rules for when and how to refill the buckets.

Key Insight: The true value of the bucket strategy is behavioral. As the team at Spivak Financial Group often advises, by creating a dedicated cash reserve, retirees are less likely to make emotional decisions during market downturns, protecting their long-term growth potential.

Before implementing this strategy, it's vital to define your bucket sizes, asset allocations, and refilling triggers. Working with a financial professional can help you tailor the bucket system to your specific risk tolerance and income requirements, ensuring it aligns with your overall retirement plan.

7. Geographic Arbitrage + Lower Withdrawal Rate

Instead of focusing solely on how to access funds early, some of the most effective early retirement withdrawal strategies concentrate on drastically reducing the amount of money you need in the first place. Geographic arbitrage is a powerful concept where you leverage the cost-of-living differences between locations to make your retirement savings go much further. By moving from a high-cost-of-living area to a more affordable one, you can maintain or even improve your quality of life on a significantly smaller budget.

How Does Geographic Arbitrage Work?

The principle is simple: earn your money in a high-income area and spend it in a low-cost one. For early retirees, this means relocating to a place where housing, healthcare, food, and transportation costs are a fraction of what they are in major metropolitan centers. This reduction in expenses directly lowers the required withdrawal rate from your portfolio, making early retirement sustainable with a smaller nest egg and preserving your capital for longer.

This strategy can be implemented in several ways:

- Domestic Relocation: Moving from an expensive state like California or New York to a lower-cost state such as Tennessee, Alabama, or a more rural part of the Midwest.

- International Relocation: Moving abroad to countries where the U.S. dollar has strong purchasing power, such as Portugal, Mexico, or parts of Southeast Asia.

Practical Implementation and Examples

Consider a couple living in San Francisco with annual expenses of $100,000. To retire early using a 4% withdrawal rate, they would need a $2.5 million portfolio. By relocating to a city in rural Tennessee, they might reduce their annual expenses to just $40,000. Suddenly, their required nest egg drops to only $1 million, making early retirement achievable years sooner.

Internationally, the effect can be even more dramatic. Many expatriates find they can live a comfortable, vibrant life in countries like Portugal or Mexico on $25,000-$35,000 per year. This strategy has been popularized by blogs like Go Curry Cracker, which documents a family's journey to early retirement largely through travel and location optimization.

Is This Strategy Right for You?

Geographic arbitrage is ideal for adventurous individuals or couples who are not tied to a specific location and are open to new cultures and experiences. The primary benefit is the immense financial leverage it provides, making early retirement accessible to those with more modest savings. However, it requires significant research and a willingness to adapt. You must be prepared for the challenges of moving, which can include leaving behind family and friends, navigating new healthcare systems, and understanding different tax laws.

Key Insight: Before making a permanent move, test your chosen location with an extended stay of three to six months. This allows you to experience daily life, understand the true costs, and decide if the culture is a good fit without making an irreversible commitment.

It is crucial to research your potential new home thoroughly. This includes a deep dive into healthcare quality and costs, visa requirements (if international), and local tax implications. To understand how your new, lower expenses translate into a sustainable income plan, you can explore what constitutes a good monthly retirement income. Consulting with a financial professional can help you model the long-term impact of such a move on your portfolio.

Early Retirement Withdrawal Strategies Comparison

| Strategy | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Rule of 72(t) – Substantially Equal Periodic Payments | High – strict IRS rules, no payment changes allowed | Moderate – requires calculation methods and consistent payments | Penalty-free early withdrawals; fixed predictable income | Early retirees needing early access to retirement funds | Avoids early penalty; IRS-sanctioned; predictable income |

| Roth IRA Ladder | Moderate – requires yearly conversions and tracking | Moderate – taxes paid upfront during conversions | Tax-free withdrawals after 5-year seasoning per conversion | Those who can plan 5+ years ahead, want tax-free withdrawals | Flexibility in timing; tax-free income; reduces RMDs |

| Bridge Strategy | Low – straightforward investing in taxable accounts | High – large taxable savings needed (10-15 years expenses) | Flexible withdrawals without penalties; bridges early retirement gap | Early retirees with substantial taxable assets | Full withdrawal flexibility; no penalty; tax loss harvesting possible |

| Cash Cushion Strategy | Low – maintain cash reserves | High – needs 3-5 years expenses held in cash | Market downturn protection; liquidity during bear markets | Risk-averse retirees wanting to avoid selling investments | Mitigates sequence risk; psychological comfort; flexibility |

| Bond Ladder Strategy | Moderate – building staggered bond maturities | Moderate – funds spread across bond maturities | Predictable income and principal return over early years | Retirees seeking steady income with capital preservation | Predictable cash flow; principal protection; reduces volatility |

| Bucket Strategy | Moderate to High – multiple buckets to manage | Moderate – diversified allocations by time horizon | Matches investment risk to funds' time horizons | Those wanting structured, phased withdrawal planning | Aligns risk with time; behavioral benefits; systematic refilling |

| Geographic Arbitrage + Lower Withdrawal Rate | Low to Moderate – lifestyle and location changes | Low to Moderate – smaller portfolio due to lower expenses | Extended portfolio longevity; smaller nest egg required | Retirees willing to relocate for cost savings | Dramatically lowers required savings; cultural experiences; improves longevity |

Crafting Your Personalized Early retirement Blueprint

The journey to financial independence is exhilarating, but crossing the finish line into early retirement requires a different kind of skill: transforming your accumulated assets into a reliable, penalty-free income stream. As we've explored, there is no single "best" method. The ideal approach is a deeply personal mosaic, assembled from the pieces that best fit your unique financial picture, risk tolerance, and life aspirations. Your optimal path might be a straightforward application of the Rule of 55, or it could be a sophisticated blend of a Roth conversion ladder for future tax-free growth and a cash cushion to navigate the first few years.

The key takeaway is that flexibility and foresight are your greatest allies. The financial landscape shifts, and your personal circumstances will undoubtedly evolve. The most resilient early retirement withdrawal strategies are not rigid, set-it-and-forget-it plans. They are dynamic blueprints designed to adapt, allowing you to pivot as needed without jeopardizing your long-term security.

Key Takeaways and Your Next Steps

Let's distill the core principles from the strategies we've covered into actionable steps you can take today:

- Quantify Your Needs: Before you can choose a withdrawal method, you must have a crystal-clear understanding of your annual income requirements. This is your foundation.

- Assess Your Asset Allocation: Where is your money located? Knowing the breakdown between your 401(k)s, IRAs, Roth accounts, and taxable brokerage accounts is critical for determining which strategies are even available to you.

- Evaluate Your Timeline: How many years do you need to bridge until age 59½? This single factor can heavily influence whether a short-term solution like a bond ladder is sufficient or if a long-term, complex strategy like a 72(t) SEPP is more appropriate.

- Model Different Scenarios: Don't commit to a single strategy on paper. Use retirement calculators or spreadsheets to model how different approaches would perform under various market conditions. How does your plan hold up during a downturn? What happens if your spending needs change?

A Note on Execution: The success of any withdrawal plan hinges on more than just the initial setup. Beyond simply withdrawing funds, the longevity of your early retirement greatly depends on diligent adherence to sound portfolio management best practices to ensure your underlying assets can sustain your withdrawals for decades to come.

The Power of a Personalized Blueprint

Choosing the right withdrawal strategy is not just a financial decision; it's a lifestyle enabler. A well-structured plan provides the confidence to leave the workforce, knowing you have a secure and compliant income stream to support your dreams, whether that involves traveling the world, starting a new venture, or simply enjoying more time with loved ones.

However, the complexity and unforgiving nature of IRS rules, particularly for strategies like the 72(t) SEPP or Roth ladders, cannot be overstated. A minor miscalculation or a missed deadline can trigger steep penalties and taxes, potentially unraveling years of disciplined saving and planning. This is where professional guidance becomes invaluable. An expert can help you navigate the regulatory maze, stress-test your plan against potential risks, and ensure every component is optimized for your specific situation.

The team at Spivak Financial Group specializes in designing and implementing these sophisticated early retirement withdrawal strategies, helping clients build the resilient and tax-efficient income plans they need to retire with confidence.

Contact Spivak Financial Group to ensure your blueprint is built on a solid foundation:

Spivak Financial Group

8753 E. Bell Road

Suite #101

Scottsdale, AZ 85260

(844) 776-3728

Navigating the complexities of the Rule of 72(t) requires precision and expertise. For those considering this powerful strategy, the specialized tools and calculators at 72tProfessor.com can help you model and implement a compliant Substantially Equal Periodic Payment plan. Visit 72tProfessor.com to explore how their software can simplify one of the most intricate early retirement withdrawal strategies.